(Kitco News) – August was a rough month for the crypto market as Bitcoin’s (BTC) price experienced a 30% correction, falling from $70,000 to a low near $49,000. But according to one analyst, the sub-50k dip likely marked the bottom of the pullback, and things are expected to improve in the final quarter of 2024.

“August was characterized by a severe drawdown in cryptoassets and traditional financial assets due to increasing US recession woes,” said André Dragosch, Head of Research at ETC Group. “The main catalyst was the disappointing US jobs report for July that showed an increase in the US unemployment rate, which triggered many popular recession indicators such as the ‘Sahm Rule.’”

“Furthermore, the sharp appreciation of the Japanese Yen (JPY) sent shock waves through traditional financial markets as carry traders unwound their positions due to an increase in Japanese key interest rates by the Bank of Japan, which exacerbated flight-to-safety in early August,” he added.

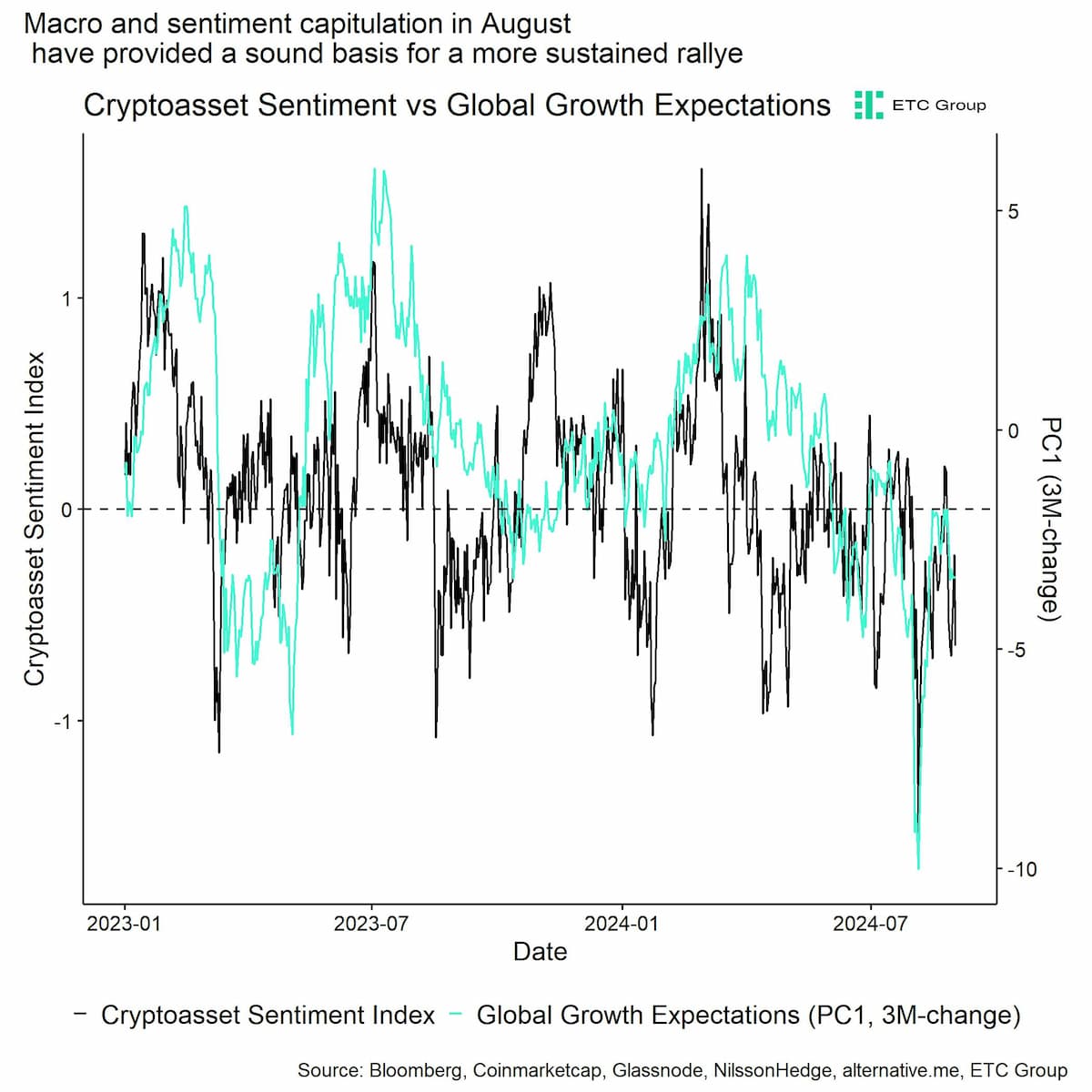

Dragosch noted that the result was a plunge in crypto asset sentiment to its lowest reading since November 2022, when FTX collapsed.

“This pronounced bearishness in crypto markets also coincided with a significant decline in cross-asset risk appetite in traditional financial markets,” he observed. “That being said, we think the combination of the macro and crypto sentiment capitulation in early August most likely marked a significant tactical bottom in Bitcoin and consequently also marked the beginning of a renewed bull run.”

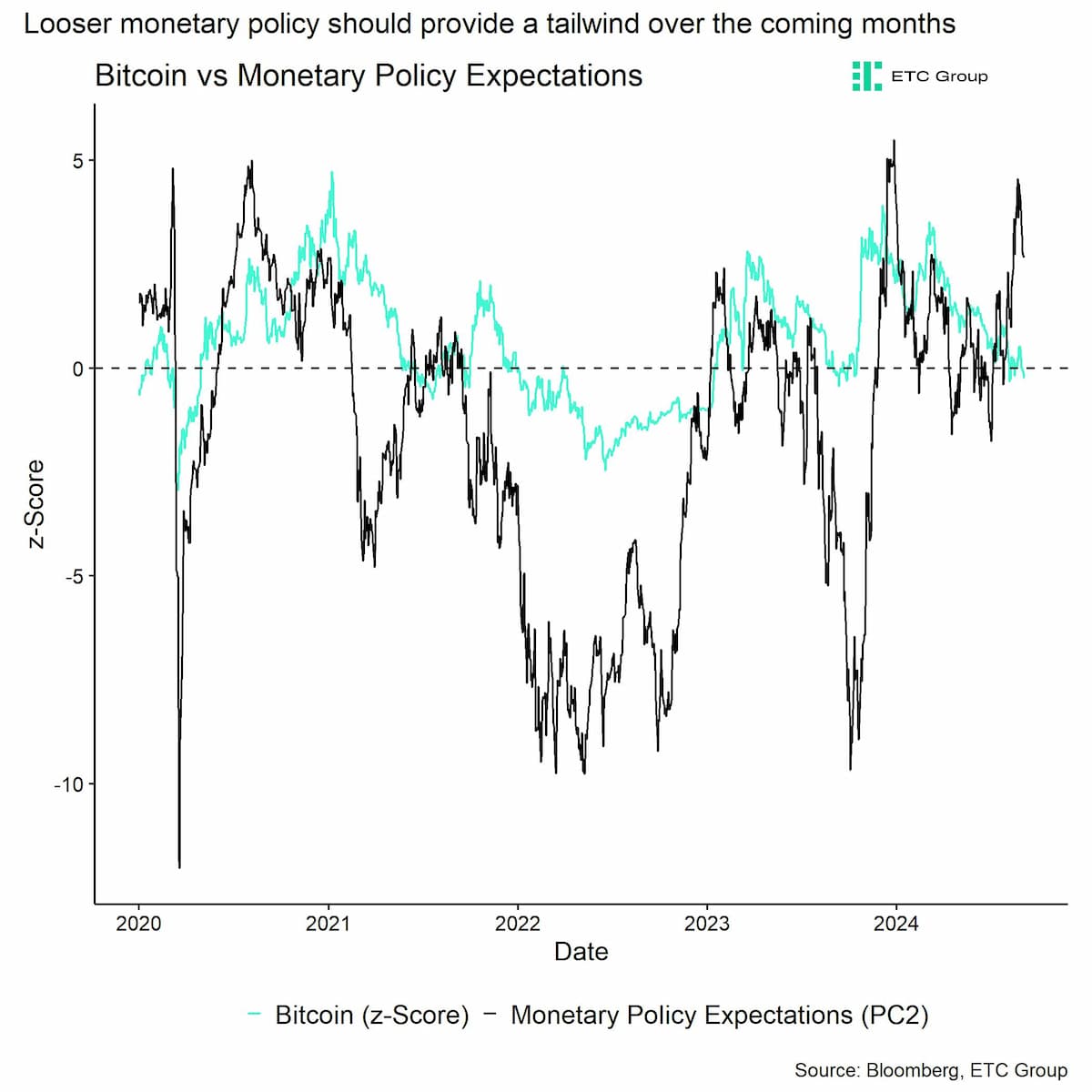

Dragosch said one of the main reasons for the bullish outlook “is the fact that financial markets were quick to price in a reversal in Fed monetary policy following these market ructions at the beginning of August, which were also recently confirmed by the latest deliberations by Fed chairman Powell at the central bank symposium in Jackson Hole, Wyoming.”

With Powell clearly communicating “that a reversal in Fed monetary policy is imminent amid the weakening labor market and is very likely to commence this month,” Dragosch said, “Expectations of looser monetary policy are bound to provide a positive tailwind for Bitcoin and cryptoassets over the coming months.”

Pointing to the fallout that ensued after the yen carry trade unwound, which led to the JPY increasing in value as carry traders unwound their positions and sold foreign currency assets to buy back their short yen positions, he said that the “JPY appreciation of the Yen is consistent with a much broader weakness in global growth expectations emanating from increasing US recession risks.”

“This observation is also consistent with the persistent rally in the price of gold amid flight-to-safety and increasing expectations of a Fed monetary policy pivot,” Dragosch added.

With Fed Chair Jerome Powell providing a clear signal that a monetary policy shift is imminent and rate cuts are on the table for September, Dragosch said ETC Group’s “market-based measure of monetary policy expectations is now clearly signaling positive expectations for monetary policy.”

“This is bound to provide a positive tailwind for Bitcoin and other cryptoassets over the coming months,” he said. “At the time of writing, Fed Funds Futures already price in slightly more than 9 cuts at 25 bps each and a terminal rate of 3%, which will be reached by the end of 2025. So, markets are already anticipating significant cuts to the Fed Funds target rate.”

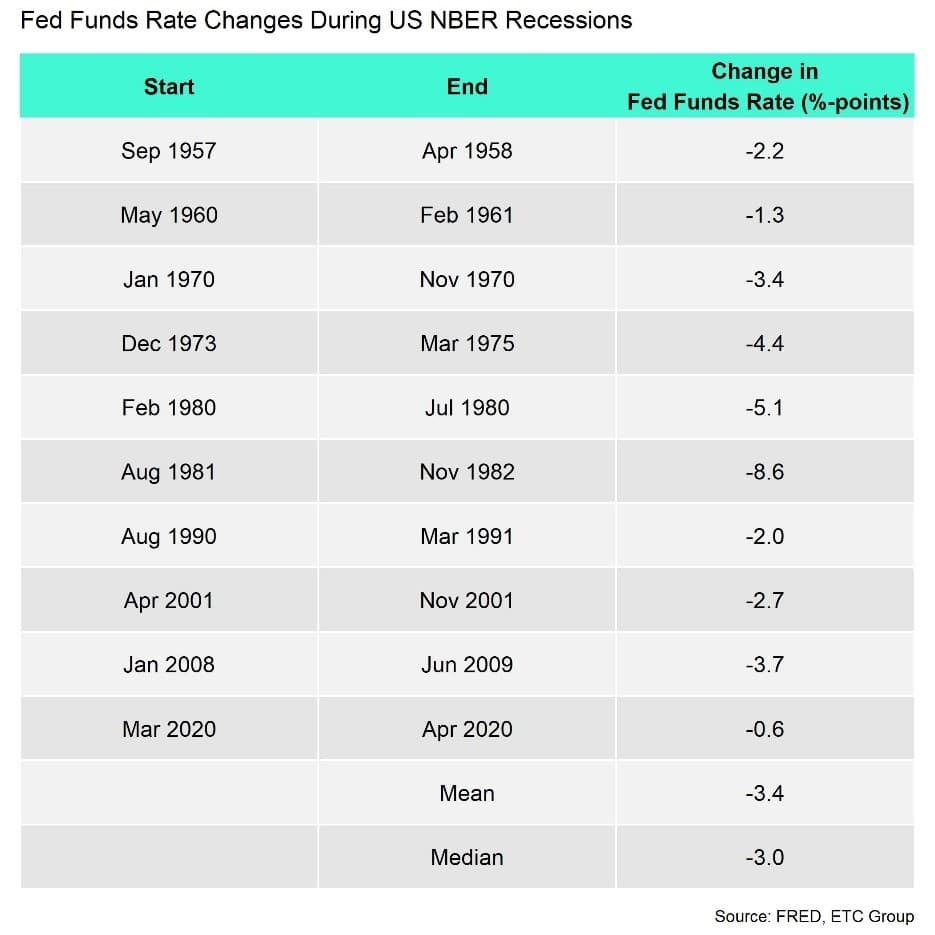

Despite these efforts, Dragosch said their “base case remains for a US recession to materialize.”

“It could very well be that the US economy is already sliding into a recession as we speak,” he said. “In case of a recession, it is quite likely that markets will price in even more Fed cuts since the average reduction in the Fed Funds Rate during past US recessions has been around -340 basis points (median: -300 basis points).”

Dragosch highlighted several reasons to expect a recession in the U.S., including a triggering of the Sahm and Mel Rules, “which are clear signals of an imminent recession,” while the “spread between expectations and present situation in the Conference Board consumer survey has increased to a new cycle high in July suggesting that we are entering a recession already.”

“The spread between the prominent ‘jobs hard to get’ and ‘jobs plentiful’ sub-indicator also suggests that US consumers see labor market conditions clearly deteriorating,” he added. “Another reason to assume broad-based weakness in the US labor market is the fact that payroll growth has recently been significantly revised to the downside,” noting the 818,000 reduction in non-farm growth through March 2024.

“It is quite likely that downward revisions to US payrolls will continue into the future as the establishment survey indicates a significant decline in establishment counts in the US, contrary to what the household survey and the payroll data are still implying,” he said. “So, BLS payroll statistics will most likely continue to overstate the ‘true’ state of the US labor market until further revisions occur.”

Dragosch noted that while “leading indicators of the unemployment rate are not yet signaling an imminent spike in layoffs… this could change in Q4 as layoffs tend to be announced around the turn of the year.”

“The recent increase in the unemployment rate is rather stemming from a significant decline in job openings and hirings across the economy,” he said. “This is also evident in the continued decline in job openings signaled in both the LinkUp 10,000 data as well as job openings data published by Indeed, which is consistent with official job openings statistics in the JOLTS data.”

Dragosh said that while a recession would be a negative development for most assets, several factors suggest it could be positive for cryptos.

“The macro capitulation in early August coincided with a capitulation in crypto sentiment, which significantly limits further downside,” he said. “Market-based global growth expectations hit a multi-year low on the 5th of August while our in-house Cryptoasset Sentiment Index hit the lowest level since November 2022, i.e. when FTX collapsed. A significant growth scare appears to be priced in already so that [an] actual recession could have less of an impact on crypto performances going forward.”

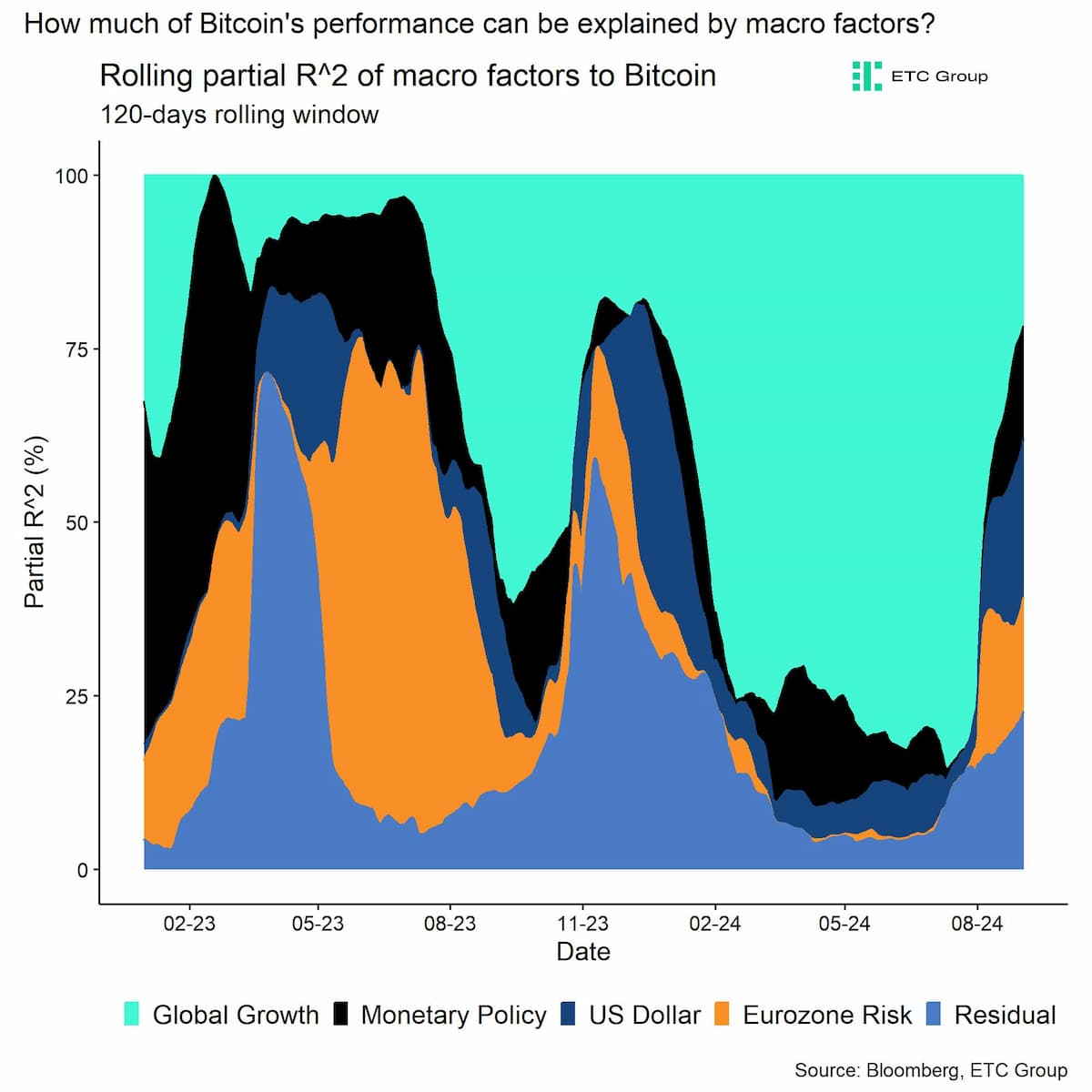

A second positive factor is that “Bitcoin's sensitivity to global growth expectations is decreasing, making a potential US recession less of a risk for cryptoassets,” he added. “To the contrary, we are shifting from headwinds (growth) to tailwinds (monetary policy, US Dollar).”

“Our macro factor model implies that Bitcoin's performance over the past 120 days has been explained less by changes in global growth expectations (which have been a headwind) and more by other macro factors such as monetary policy expectations or the US Dollar (which have provided tailwinds),” Dragosch said. “In particular, we are also seeing an increasing share in explanatory power by residual/non-macro/coin-specific factors for Bitcoin, which imply an increasing probability of Bitcoin to even decouple from increasing US recession risks.”

Third, he said the “monetary policy tide is turning, and initial Fed rate cuts are imminent.”

“At the time of writing, Fed Funds Futures price a total of 9 cuts at 25 bps and a terminal rate of approximately 3% by the end of 2025,” he noted. “G5 central banks are shifting towards easing mode and global money supply has recently reached a new all-time high. Expansions in global money supply tend to be bullish environments for Bitcoin and cryptoassets.”

And the fourth reason to be bullish on Bitcoin is the fact that “The US Dollar has been weakening, which tends to be a bullish environment for Bitcoin and cryptoassets,” he said.

“Weak Dollar environments tend to be best environments for Bitcoin and vice versa,” he added. “A reversal in Fed monetary policy associated with interest rate cuts and Quantitative Easing (QE) tends to be Dollar bearish, which should provide a significant tailwind for Bitcoin and cryptoassets going forward.”

“Bottom Line: The simultaneous macro and crypto sentiment capitulation in early August has provided a good basis for a more sustainable bottom in Bitcoin,” Dragosch concluded. “In addition, we think that the fact that Bitcoin has become less sensitive to changes in global growth expectations, the turnaround in global monetary policy combined with a broad Dollar weakness could provide a very positive macro tailwind for Bitcoin and cryptoassets going forward.”