(Kitco News) – The U.S. federal deficit currently stands at $35.362 trillion, its highest level in history. Despite politicians' lip service that reducing the debt is a priority, one analyst says meaningfully reducing the debt is unlikely as the world faces a potential global recession.

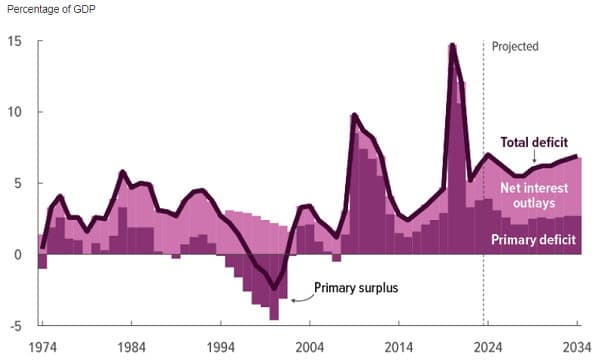

“The Congressional Budget Office projects structurally high deficits forever unless meaningfully addressed, despite the fact that they assume no recessions will ever occur, and deficits tend to be even larger when recessions do occur,” noted Lyn Alden, an independent investment and macroeconomic analyst.

“So that’s the conservative baseline, which calls for over $20 trillion in net new public debt additions over the next 10 years,” she said.

According to Alden, what the data really shows is that the U.S. “is in the process of entering fiscal dominance. This means that fiscal deficits are larger and more impactful for the economy and for financial markets than they used to be, and at inflection points they can even impair the effectiveness of the central bank’s monetary policy or outright constrain the central bank’s ability to make certain monetary policy decisions independently.”

After listing several recent developments that highlight this trend – including the 2019 bond market bubble and the surge in inflation that began in 2021 – Alden noted that recently, she has “been focused on the topic of the U.S. economy slowing down again, but in ways that are somewhat counterintuitive and rather sector-specific.”

“Some aspects of the economy look like they’re at risk of going into recession, whereas other aspects of the economy look as if they’ve already been through a recession and are emerging back into growth,” she noted.

“One of the investment implications from all of this in this cycle is that, despite being quite concerned with the outcomes of a lot of these actions at times, I’ve been heavy on equities and other scarce assets, and light on bonds,” Alden said. “Since we’re in fiscal dominance, we can’t bet too much on the value of the denominator (the dollar) other than as a temporary trade. The defensive side of my portfolio has mostly consisted of T-bills and gold, which both held up better than T-bonds since 2019.”

Alden said that while politicians like to play the blame game when it comes to who is responsible for the current state of the U.S. economy, “fiscal deficits are harder to fix than most people realize,” and rather than one specific person to blame, “it’s a blend of many factors going back decades.”

One issue is how Social Security was designed. “As the nation grows older and more top-heavy, there are fewer workers supporting each retiree. The social security fund that was built up for decades is now shrinking, and is expected to be depleted by 2035, from which point it’ll have an inability to make the full payouts if left unfixed,” she said.

A second major concern is inefficient healthcare spending.

“The United States government subsidizes the raw ingredients that go into inexpensive carbohydrate-based ultra-processed foods,” Alden noted. “For example, the high-fructose corn syrup industry gets more federal funds (via subsidies for types of corn that are bred for that purpose and inedible for corn-on-the-cob consumption) than grass-fed beef, fruits and vegetables, or seafood.”

“For a variety of reasons, obesity and metabolic disorders are on a structural growth trajectory, resulting in ballooning healthcare costs,” she said. “And with our complex public/private hybrid health system with high administrative overhead, we pay more for healthcare than every other country, despite having higher infant mortality and lower life expectancy outcomes than many of them, in addition to a lower number of physicians and hospital beds per capita than many of them. For wealthy people the American healthcare system is great, but in terms of its impact on deficits and in terms of its quality for the median person, it is a major drag.”

Also adding significantly to the deficit is “Foreign Adventurism,” Alden said. “The post-9/11 War on Terror is estimated to have cost around $8 trillion with all things considered. And going forward from here, our baseline military spending is $800+ billion per year, plus various contingency spending that brings the full figure in a typical year higher than that.”

“These activities have accumulated a lot of debt onto our public ledger, contributing to our rapidly growing interest expense,” she noted.

The fourth item on the list is accumulated debt interest.

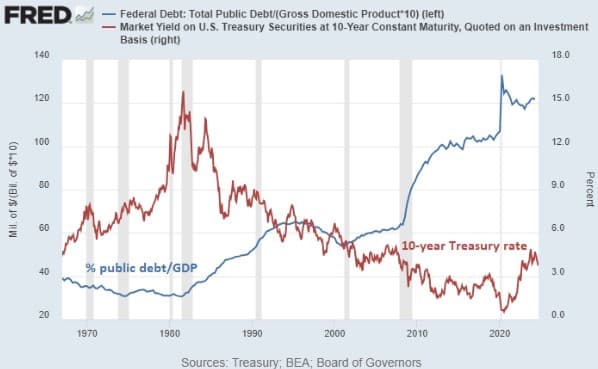

“For the past four decades, the United States had a rising debt/GDP ratio, but falling interest rates,” she highlighted. “This kept interest expense manageable in absolute terms and especially as a percentage of GDP. But now that interest rates hit zero and are bounding in a more sideways pattern, it means that the rising debt/GDP ratio no longer has an offset of structurally falling interest rates. That’s a big change.”

“A country with well over 100% debt-to-GDP has two main choices in this scenario,” Alden said. “The first choice is that they can keep interest rates very low despite periods of price inflation that occurs, and debase all of the currency holders and bondholders. Japan is far enough into fiscal dominance that they’ve chosen that route. The second choice is that they can try to meaningfully raise interest rates when needed, and contribute to a fiscal spiral of ever-higher interest expense.”

She suggested that politicians are holding out hope that productivity growth will offset price inflation, as “Aggregate price inflation is normally lower than the rate of money supply growth because there is a gradual increase in productivity.”

“In other words, the price inflation that we do get, is measured from a negative baseline, rather than from zero,” Alden said. “From a politicians’ standpoint, the best realistic scenario for them is that money supply growth will be high to support the deficits as needed, but that there will be enough productivity growth from AI and other areas to offset it and prevent aggregate prices from increasing too rapidly.”

“The problem, however, is that even if that were to happen for the official CPI metric, it wouldn’t occur evenly,” she noted. “Things that are truly scarce will increase more in line with money supply growth, widening the gap between the haves and the have-nots, likely contributing to ongoing wealth concentration and populism.”

The fifth reason for high deficits, according to Alden, is “political polarization, except for deficits.”

“Republicans and Democrats are now very polarized politically; far more than in the 1990s when they could still come to large compromises on fiscal topics,” she said. “The probability of getting through meaningful tax hikes and/or meaningful spending cuts is minimal now.”

“And yet, the one thing they do agree on is to not dramatically cut any of the major spending areas,” she added. “They have plenty of differences, but the biggest areas of spending are not really among those differences anymore.”

As an example of their shifting stances, Alden highlighted that Republicans have gone from calling for cuts to Social Security, Medicaid, and Medicare to adopting a platform that looks to protect these benefits, while Democrats are now less in favor of cuts to defense spending than they have been historically amid the rising strength of China and uptick in global conflicts.

“So now in practice, the spending differences between the parties are around the margins, and instead the main differences are 1) tax policy and 2) social and geopolitical stances,” Alden said. “The handful of things that the majority of Republicans and Democrats agree on now is that it’s a third rail to touch any of the major spending areas, ranging from Social Security, to Medicare, to Defense, to Veterans’ Benefits. And then there’s Interest Expense, which is also untouchable.”

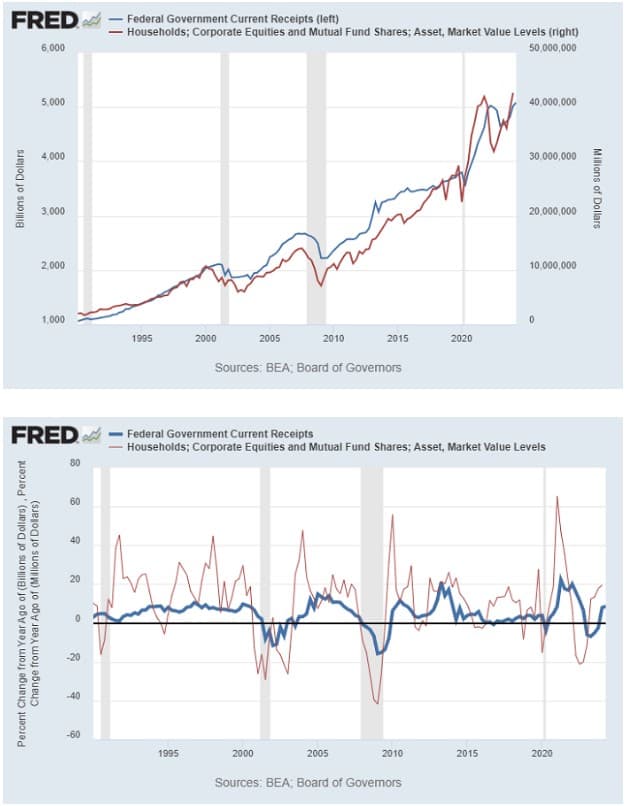

The final item she identified as leading to “sticky deficits” is the financialization of tax receipts.

“The United States’ tax receipts are more correlated to asset prices than most other countries, with tax receipts lagging the performance of the stock market,” Alden said. “This can be seen in both absolute terms and year-over-year terms.”

“We might wonder if this is an example of correlation but not causation,” she noted. “We could propose, for example, that a declining stock market predicts a rising unemployment rate, and that the rising unemployment rate is what really causes weaker tax receipts.”

“However, the recent period invalidates that idea,” Alden said. “The stock market peaked in 2021, troughed in 2022, and then soared again in 2023, all while the unemployment rate remained low. Tax receipts, with a lag, did the same thing. The strong market performance in 2021 led to strong tax receipts in 2022. The weak market performance in 2022 led to weak tax receipts in 2023. The rebounding market in 2023 led to rebounding tax receipts in 2024.”

She said that while the unemployment rate and other variables do matter, the main point is that “the stock market going sideways or down tends to be a key problematic variable for the following year’s tax receipts even on its own.”

“This is partially because the United States has more wealth concentration than most other developed countries, and with a higher ratio of that wealth tied to the stock market,” Alden said. “And it’s also partially because a very large portion of U.S. executive compensation is tied to equity value.”

“What this means is that many attempts at fiscal austerity are likely to reduce the deficit less than we might imagine, because if those austerity measures negatively impact the stock market and other types of asset prices, it’s likely to weaken the tax receipt side even as certain other spending and revenue items are adjusted,” she explained.

“So in order to meaningfully fix the deficit, not only would a highly polarized Congress have to agree on some sort of grand bargain which has been entirely impossible in the post-GFC environment and is unpopular with the voter base, it would also have to include a rather deep and skillful overhaul of the tax system itself to successfully untangle the Gordian knot that ties asset price performance and tax receipts together,” she surmised. “I’d assign an extremely low probability to that combined outcome for the next five years or ten years, which is roughly what a long-term investment timeframe is.”

Using a quote from the character Walter White on the popular show Breaking Bad, Alden said that when it comes to the momentum of these fiscal deficits, “Nothing stops this train. Nothing.”

“The decoupling of deficits from unemployment levels across two presidential administrations of differing political parties, outside of the pandemic spike, helps to illustrate Walter White’s ‘unstoppability’ of this deficit train,” she said. “The deficits are tied to a combination of entitlement demographics, healthcare inefficiencies, decades of foreign adventurism, accumulated debts and their associated interest expense, political polarization, and the financialization of tax receipts.”

Investing Implications

As for what all this means for investors, Alden said, “There are two primary investment implications or data sets from this observation of encroaching fiscal dominance that we can turn to for analysis.”

During the fiscal dominance that occurred in the 1940s, she noted that “Developed countries reached their peak of centralization back then.”

“The U.S. Treasury, as part of the Executive Branch, outright captured the Federal Reserve and had them perform yield curve control on their government debt until it was no longer needed,” she said. “The Fed held short term rates barely above zero, and long-term rates at 2.5%, as price inflation hit 19%.”

“The current political environment is more polarized compared to back then,” she noted. “The stock market, coming out of the Great Depression and entering World War II, was very cheaply priced, which differs from our currently more expensive market environment.”

And looking at how emerging markets dealt with large monetized fiscal deficits in more recent decades, Alden said, “what we see in general is that they tend to be more inflationary on average, and their recessions tend to be somewhat stagflationary rather than deflationary.”

“During crises their asset prices often do well in local currency terms, even as they do poorly when denominated in dollars or gold, because the denominator of the local currency weakens so quickly,” she said. “When money supply grows persistently at a double-digit annual rate, it’s hard for most assets to go down in nominal terms on a sustained basis, even as they can easily go down in global purchasing power terms. And much like how the U.S. behaved in the 1940s with all sorts of controls on movements of capital, emerging markets with currency crises frequently turn to various levels of capital controls.”

Taking all this into account, Alden said she has a “neutral-to-negative view on the major U.S. stock indices in inflation-adjusted terms” over the next five years.

“They’re starting from an expensive baseline, and with a high ratio of household investable assets already stuffed into them,” she noted. “However, I do think that among the universe of more cyclical and/or mid-sized stocks that make up smaller portions of the U.S. indices, there are plenty of reasonably-priced ones with better forward prospects.”

For international stocks, she said, “the upcoming 2024 Fed interest rate cutting cycle is one of the first true windows for them to have a period of outperformance relative to U.S. stocks for a change.”

“It doesn’t mean that they certainly will follow through with that, but my base case is for a meaningful asset rotation cycle to occur, with some of the underperforming international equity markets having a period of outperformance,” she added. “At the very least, I would want some exposure to them in an overall portfolio, to account for that possibility.”

Regarding developed market government bonds, Alden said she doesn’t “have a positive long-term outlook in terms of maintaining purchasing power.”

“A ten-year U.S. Treasury note currently yields about 3.7%, while money supply historically grows by an average of 7% per year, and $20 trillion in net Treasury debt is expected to hit the market over the next decade,” she noted. “So I think the long end of the curve is a useful trading sardine, but not something I want to have passive long exposure to.”

“A five-year inflation-protected Treasury note, however, pays about 1.7% above CPI, and I view that as a reasonable position for the defensive portion of a portfolio,” she added. “T-bills are also useful for the defensive portion of a portfolio. They’re not my favorite assets, but there are worse assets out there than these.”

As for gold, Alden said the yellow metal “remains interesting for this five-year period, although it might be tactically overbought in the near term. It has had a nice breakout in 2024 but is still relatively under-owned by most metrics and should benefit from the U.S. rate-cutting cycle. So I’m bullish as a base case.”

And for Bitcoin (BTC), she noted that King Crypto “has been highly correlated with global liquidity, and I expect that to continue. My five-year outlook on the asset is very bullish, but the volatility must be accounted for in position sizes for a given portfolio and its requirements.”