(Kitco News) – The current cryptocurrency bull market cycle has differed from its predecessors in a number of ways – including the launch of spot Bitcoin (BTC) exchange-traded funds (EFTs) that allowed institutional investors to get in on the game, pushing BTC to a new all-time high before its halving for the first time in history – but not all the differences are welcome. According to one analyst, the crypto industry is now in crisis as it has devolved into a haven for gambling.

“In the past, the crypto industry itself was like a game,” tweeted Ki Young Ju, founder and CEO of on-chain analytics firm CryptoQuant. “A game abstracts the human pleasure pathways, providing an experience similar to real-life happiness by triggering dopamine release. This includes the joy of overcoming adversity, the thrill of winning in competition, and the satisfaction from mental connection with others.

Ju noted that two of the most impactful “dopamine triggers” in the crypto industry include “Making money from unpredictable gambling” and “Creating new technologies in uncharted territories.”

“Those who have noticed will know that the first is the experience of traders, and the second is that of builders,” he explained. “As time has passed, the nature of traders and builders has also changed. In the early days, many investors were attracted to the philosophy, like Bitcoiners, while six years ago, futures traders dominated. Today, more conservative investors are leading the industry.”

Ju said that while the “initial builders were the cypherpunk cryptographers, six years ago, the growth of the trading industry brought forth a wave of exchange founders and coin issuers.”

“Currently, talents from various industries, including finance, gaming, and content, are participating in building,” he noted. “However, they do not blend well with those who enjoy the game-oriented trading mindset. This is because they are playing an entirely different game. What they create no longer provides dopamine to the traders.”

Ju suggested that this has led to a fundamental shift in the landscape of the cryptocurrency ecosystem.

“The synergy between traders and builders was the essence of this industry we called ‘crypto.’ The intriguing creations of builders fueled traders' enthusiasm,” he explained. “However, over time, most builders who made things that traders loved have disappeared. They have been suppressed by financial regulations, imprisoned, or have lost their hunger after making too much money and become absorbed in partying.”

In their absence, “the crypto industry is gradually turning into a gambling den,” he said. “The remaining builders are now creating either gambling products like meme coins or dull, time-consuming products seen in traditional financial institutions. Their works no longer offer fresh stimuli to traders.”

“Some are even building ecosystems so different that they are categorized as belonging to industries other than crypto,” he added. “Where have all those builders gone who inspired us and explored new technologies? Why did they leave? I don't know. I want to ask @VitalikButerin.”

Commenting on the basics of human behavior, Ju reiterated that “Humans repeat activities that stimulate dopamine. Life goals, jobs, and hobbies are all filled with things that give dopamine. An industry that does not promote dopamine is destined to decline.”

“The crypto industry we once knew is now failing to provide any dopamine to both builders and traders. That is why it is in crisis,” he said. “A new game for traders must emerge. Only then can money flow into the market, and the industry can grow. “

“The 2024 altcoin performance is dismal. Money is not flowing into the industry,” Ju concluded. “If we do not create a new game to stimulate traders' dopamine, the crypto industry we know will face a prolonged period of stagnation. I am genuinely concerned.”

In a follow-up post, Ju clarified that his comments were directed at Web3 and crypto, not Bitcoin.

The concerns expressed by Ju about the trajectory of the crypto ecosystem are shared by a large number of analysts and crypto fans who have warned about the explosive growth of the memecoin sector in 2024.

According to a report from BDC Consulting, decentralized exchange aggregator data shows that between 40,000 and 50,000 new crypto tokens are created daily, with up to 100,000 new tokens appearing “during periods of intense viral hype.”

“The majority of memecoin projects (89%) have a market cap between zero and $1,000,” the report noted. “Only 5% of memecoins had a market cap above $10 million in March 2024.”

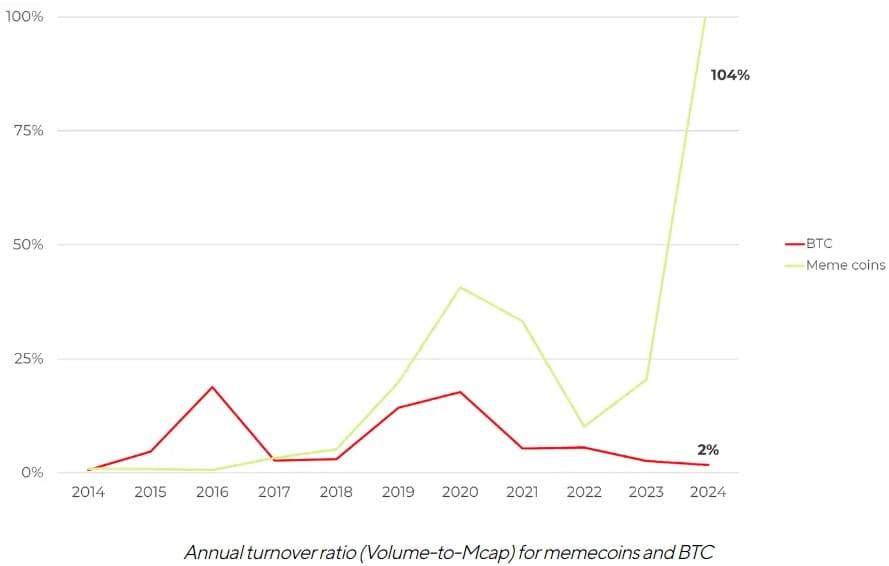

The sector is extremely volatile, and for the most part, most memecoins see a rapid rise and fall and usually leave traders who were chasing life-changing money holding a bag of worthless tokens. “As of March 2024, the turnover ratio for memecoins is 77% - and only 1.8% for Bitcoin,” the report noted.

“Memecoins’ extra-high volatility – even in a market that is considered generally very volatile – is a consequence of the current high virality in this niche,” the report said. “Memecoin buyers are mostly short-term investors or traders. Many projects can’t manage to stay liquid even for a week (this applies to 90% of newly issued coins). For this reason, only 1,000 out of the 40,000-50,000 new memecoins ever get listed on a well-known exchange.”

And with such a high token turnover, memecoins have become a hot spot for scams and honeypots, highlighting another reason that most traders should avoid this sub-sector of tokens.

“A rug pull is one of the most common scams: the way it works is that the creators of a token pull out investors’ liquidity from a trading pool,” BDC Consulting noted. “As the memecoin market exploded, over 85% of all such projects had low liquidity and could hide vulnerability at the level of contract code. Honeypot is one of the most common contract-level threats: it makes it difficult to re-sell tokens and thus artificially inflates their prices.”

According to the State of Memecoin 2024 report from Chainplay, the average lifespan of a memecoin is one year, just a third of the life span of an average crypto project, and 97% of all memecoins that have been created have already ceased to exist.

Chainplay noted that each month, an average of 2,020 memecoin disappear, and overall, 55.24% of all memecoins are deemed malicious, and one-third of investors have reported losses due to scam tokens.

“Despite the high risks and volatility, memecoins have firmly established themselves in many crypto investors' portfolios,” Chainplay noted. “Two-thirds of crypto investors have invested in memecoins. This widespread adoption indicates a substantial belief in the potential for high returns, despite the known risks. Meanwhile, the media’s stance on memecoins is predominantly cautious. Only 13.77% of news reports about memecoins are bullish, reflecting widespread skepticism.”

“The state of memecoins in 2024 paints a vivid picture of high risk and rapid turnover,” the report concluded. “While the majority of memecoins have a short lifespan and high failure rate, they continue to attract investors due to their potential for quick gains. The prevalence of scams and the cautious media sentiment further complicate the investment environment.”

While the crypto community at large remains at odds over memecoins and whether they help or hurt the industry, Vitalik Buterin, co-founder of Ethereum, suggested that they won’t go away anytime soon, so its best to try and find a middle ground.

“One of my personal moral rules is ‘if there is a class of people or groups you dislike, be willing to praise at least a few of them that do the best job of satisfying your values,” Buterin wrote. “If you dislike social media platforms for being extractive and encouraging toxic behavior, but you think Reddit is 2x less bad, say nice things about Reddit. The opposite approach - to shout ‘yes, all X are part of the problem’ - feels good in the moment, but it alienates people and pushes them further toward their own bubble where they will insulate themselves entirely from any moral appeals you might have in the future.”

“I think of the ‘degen’ parts of the crypto space in the same way,” he added. “I have zero enthusiasm for coins named after totalitarian political movements, scams, rugpulls or anything that feels exciting in month N but leaves everyone upset in month N+1. At the same time, I value people's desire to have fun, and I would rather the crypto space somehow swim with this current rather than against it.”

“And so I want to see higher quality fun projects that contribute positively to the ecosystem and the world around them (and not just by ‘bringing in users’) get more mindshare,” he concluded. “At the least, more good memecoins than bad ones, ideally those that support public goods instead of just enriching insiders and creators. But also ideally, making games rather than coins, and making projects that people enjoy participating in.”