(Kitco News) - The start of the Federal Reserve’s new easing cycle is a tide that is lifting all boats in the precious metals market, as the sector is seeing broad gains in gold, silver, and platinum group metals.

While gold is attracting most of the attention in the marketplace, PGMs, particularly platinum, are starting to gain notice. Platinum prices have pushed back above $1,000 an ounce, trading at their highest level in 10 weeks. September platinum futures last traded at $1,013.20 an ounce, up 2% on the session.

Analysts note that lower interest rates, falling real yields, and a weaker U.S. dollar are making precious metals attractive investment opportunities. However, the World Platinum Investment Council (WPIC) notes that platinum has another strong tailwind: growing long-term deficits.

In a recent interview with Kitco News, Edward Sterck, Director of Research at the WPIC, said he expects it’s only a matter of time before the market’s growing deficit starts to impact prices. The comments were made as the WPIC published its demand trends for the second quarter.

The council sees platinum’s deficit growing by one million ounces this year; however, Sterck said that this is only one piece of a much bigger trend.

"We expect that underlying fundamentals should offer some support for prices," he said. "We are confident that there will be further deficits in the platinum market."

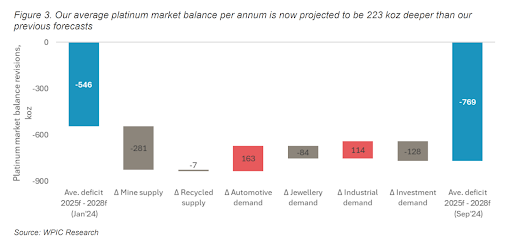

On Thursday, the WPIC published updated long-term forecasts. Platinum’s supply deficit is expected to average around 769,000 ounces between 2025 and 2028, a downward revision from January’s long-term projected average deficit of 546,000 ounces.

The analysts expect weak supply growth and solid demand to drive deficits in the next three years.

“Following company guidance, we have reduced average projected [South African] platinum production by 179 koz between 2025 and 2028. South African average platinum production forecasts have been reduced by 4% as margin pressure disincentivizes new growth,” the analysts said in the report. “In North America, we have reduced our average platinum production forecasts by 109 koz or 33% from 2025 to 2028.”

At the same time, demand, driven by the automotive sector, is expected to remain robust, even as the battery electric vehicle (BEV) market takes market share from internal combustion engines.

However, the WPIC expects that EV growth projections are a little too optimistic.

“BEV demand growth has slowed from +30% year-on-year in 2023 to mid-single-digit growth in 2024 year-to-date. Softening BEV demand growth is primarily attributable to consumer reluctance to adopt full battery electrification in the face of slow progress in reducing BEV prices, the lagging rollout of public charging infrastructure, and tapering government subsidies for BEVs,” the WPIC said.

At the same time, growing demand for hybrid electric vehicles, which still use catalytic converters to remove harmful emissions, will support platinum prices.

The WPIC also noted that increased loading in catalytic converters means that even if fewer cars are sold, more platinum will be needed to meet tightening environmental regulations.

Eighty percent of demand for platinum comes from the automotive sector.

The WPIC also sees growing demand from the investment sector.

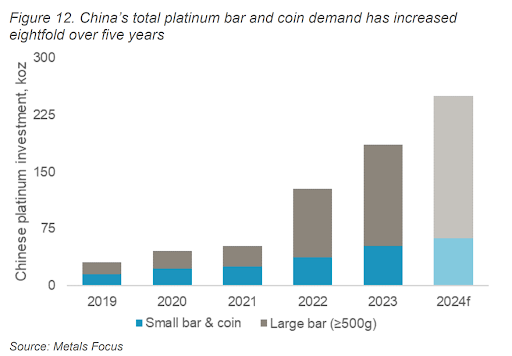

“Investment demand, always measured on a net basis, is forecast to be 128 koz higher per annum, based on the inclusion of Chinese bar and coin demand,” the report said.

As deficits grow, the analysts expect above-ground stocks will continue to be depleted.

“Platinum’s relatively inelastic demand will require the market to draw down above-ground stocks to fulfill multi-year market deficits from 2025 to 2028. It is not known what platinum price will be necessary to attract the portion of above-ground stocks required to meet the supply shortfall,” the analysts said. “All told, the compelling elements of resilient demand, supply-side risks, and a depleting stockpile combine to underpin platinum’s attractive investment case.”