(Kitco News) – Gold has shined bright in 2024 as rising demand from central banks and retail investors has pushed the yellow metal to multiple new record highs, and it could potentially continue to see its fortunes rise for years to come as one analyst warns that the gold supply is at risk due to scarce and smaller gold discoveries.

According to a report from S&P Global analyst Paul Manalo, there have only been five major gold discoveries since 2020, totaling 17 Moz of gold.

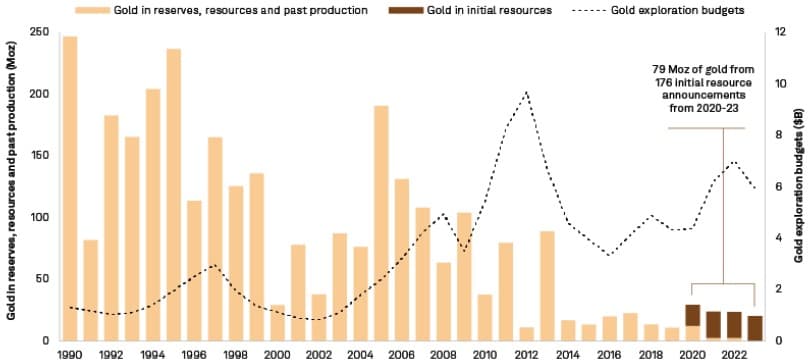

S&P’s annual analysis of major gold discoveries found that there were 350 deposits discovered between 1990 and 2023, containing 2.9 billion ounces of gold in reserves, resources and past production. A major gold discovery is one defined as one containing at least 2 million ounces in reserves, resources, and past production.

“While the number of major discoveries and the total amount of gold continue to grow each year, it is important to note that most of the assets added to the list were discovered decades ago and only recently met the criteria of having at least 2 million ounces of gold in reserves, resources and past production,” wrote Manalo. “Since 2020, there have been only five major discoveries with a total of 17 Moz of gold, accounting for just 22% of the additional 79 Moz of gold added in the 2024 update.”

Manalo said the recent discoveries “are scarce and smaller in size, with an average of 3.5 Moz compared to the 5.5 Moz average from 2010 to 2019. None of the discoveries made in the last 10 years have entered the list of the largest 30 gold discoveries, supporting our long-held view that the decade-long focus on older and known deposits limits the chance of finding huge discoveries in early-stage prospects.”

“It is important to note that while recent significant discoveries are sparse, reserves and resources grow over time, and there is still potential for growth in these recent discoveries,” he added.

That said, Manalo warned that “The lack of quality discoveries in the recent decade does not bode well for the gold supply.”

“Based on the latest monthly Gold Commodity Briefing Service, we expect gold supply to peak in 2026 at 110 Moz., driven by increased production in Australia, Canada, and the U.S. – countries that also account for most discovered gold,” he said. “Gold supply is expected to fall to 103 Moz in 2028, resulting from a decline in supply from these countries.”

There is some hope that supply will increase, he noted, as S&P has “Identified 176 initial resource announcements with a total of 79 Moz of contained gold” after examining various prospectus announcements.

“Only 78, or 44%, of these announcements are from greenfield assets, while the rest are from newly discovered deposits within existing projects, demonstrating the industry’s preference for exploring known assets,” he said. “While not all of these assets will become major discoveries, the increasing number of announcements in recent years brings much-needed optimism to an industry that has experienced fewer and smaller discoveries.”

Manalo suggested that the rising price of gold could help change this outlook, as it allows annual gold exploration budgets to continue to increase.

“Since 2017, annual gold exploration budgets have more than doubled, reaching a peak of $7 billion in 2022 after a low of $3.3 billion in 2016,” he noted. “Although budges fell in 2023 due to tighter financing conditions, they remain elevated compared to previous years. This trend is likely to continue as long as gold prices remain high.”

Manalo added that between 2017 and 2023, the higher budgets resulted in “an average of 42 announcements with an average of 24 Moz of gold each year, compared to an average of 30 announcements and 13 Moz of gold from 2013 to 2016, when gold budgets were declining.”

“The future of gold supply is a mixed bag. The focus on old and existing assets has taken a toll on the number and size of discoveries in recent years, as proven by the lack of substantial discoveries in the last decade,” he concluded. “However, the increasing gold budgets since 2017 bring a tad of optimism for the future of gold supply, as the number of initial resource announcements continue to grow in size and number.”

Commenting on Manalo’s analysis, Ahead of the Heard editor Rick Mills warned: “Peak gold it’s already here.”

“In a world of resource depletion, it falls to gold exploration companies to fill the gap with new deposits that can deliver the kind of production required to meet gold demand, which is currently out-running supply,” he added. “The gold market continues to experience tightness due to difficulties expanding existing deposits and a pronounced lack of large discoveries in recent years.”

“In 2023, 4,448 tonnes of gold demand minus 3,644t of gold mine production left a deficit of 804t,” Mills noted. “Only by recycling 1,237t of gold jewelry could the demand be met. (The World Gold Council: ‘Gold Demand Trends Full Year 2023’).”

“This is our definition of peak gold,” he said. “Will the gold mining industry be able to produce, or discover, enough gold so that it’s able to meet demand without having to recycle jewelry? If the numbers reflect that, peak gold would be debunked. We’ve been tracking it since 2019, and it hasn’t happened yet.”

After listing off several factors contributing to his negative outlook, including the escalating economic battle between the U.S. and China via tariffs, Mills said, “The situation is dire, and it starts with mining.”

“The S&P report is misleading in that it shows that major mining companies are exploring for more gold, but they are doing it on their own properties, sometimes mining around the edges of deposits discovered decades ago,” he noted. “They are doing nothing to go out and find new mines, but that has never been a major’s job. It’s the job of juniors to discover new mineral deposits, but they are not being financed; they literally have no money and are conducting financings at 5-10 cents, thus blowing out their share structures.”

“Right now, the industry’s solution is to go poking around their own brownfield projects to find more metal to mine,” he added. “It’s a far cry from what we are going to need. It is elemental to the mining industry that the juniors are well financed, [and for] deposits [to] have a shortened path to production, say five years like in Scandinavia, versus up to 28 in the US. Juniors need to be out in the bush making discoveries.”

Mills said that “only with the help of juniors can mining solve its existential problem of getting the resources that are currently owned by its adversaries. Junior resource companies find the resources miners then buy and turn into their mineable reserves.”

“In fact, I don’t think it’s much of a stretch to say that without financed juniors, without a safe and secure supply of metals, without security of supply, without refineries and smelters, and without the technological knowledge to manufacture magnets and anodes, the developed economies of the western world are very much at risk if supplies of these critical metals, and associated technologies, come from our competitors,” he concluded.