(Kitco News) – The rising price of gold has led to a resurgence of interest in the yellow metal, especially as global economic conditions worsen and geopolitical tensions escalate. To help investors better gauge how gold could benefit their portfolios, the World Gold Council has released a new tool to help determine gold’s real return.

“While gold’s contribution to managing portfolio risk is well established, supported by a large body of work devoted to its hedging characteristics, its contribution to portfolio return is not,” the WGC wrote. “Frameworks for estimating gold’s long-term return exist but fall short of a robust approach that aligns with the capital market assumptions for other asset classes.”

“Gold’s dual nature, as both a real good and a financial asset, means that its value is not easily explained by traditional asset pricing models,” they added. “This is further complicated by gold’s continued use as a monetary asset within central bank reserves, despite the ending of the Gold Standard and the mandatory requirement to hold gold as reserves more than five decades ago.”

Since gold doesn’t generate cash flows, the WGC highlighted that “traditional discounted cash flow models are not applicable,” adding that “Generally, commodity pricing models also fall short given gold’s unique and ever-growing above-ground stock that, among other things, diminishes primary production as marginal supply.”

“Unlike most other commodities such as oil and wheat, gold cannot be consumed in the sense that its consumption makes it disappear,” they noted.

For these reasons, the WGC has created a new framework to better determine gold’s contribution to portfolio returns, dubbed the “Gold Long-Term Expected Return (GLTER),” which “uses the distribution of above-ground gold stocks analyzed via different demand categories as a foundation and starting point.”

“Publications tackling gold’s expected return have generally concluded that gold’s primary function is as a store of value, implying a long-run co-movement of gold with the general price level (CPI),” the WGC said. “Alternative approaches using risk premia estimations or bond-like structures with embedded options produce similar results.”

They said that while these efforts provide valuable insights, there are two features that “mischaracterize gold and have led to biased conclusions: Using data from periods during the Gold Standard to analyze gold’s performance paints a misleading relationship between gold and general prices; and Viewing long-term price dynamics exclusively through the lens of demand from financial markets and ignoring other sources of demand, is a likely contributor to a systematic underweighting of gold in private portfolio allocations.”

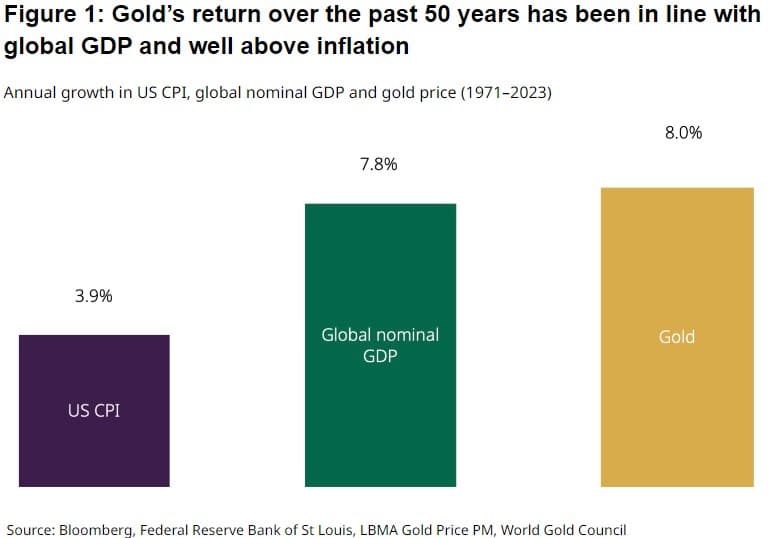

“In most cases, these theories land on an expected long-run real return ranging between 0% and 1%,” the report said. “We instead show that gold’s long-run return has been well above inflation for over 50 years, more closely mirroring global gross domestic product (GDP), a proxy for the economic expansion driver used in our other gold pricing models.”

Using GLTER, investors can better understand the various sources of gold demand – including jewelry and technology fabrication, central banks, financial investment, retail bars, and coins – and see that “the gold price over long horizons is mainly driven by an economic component, proxied by global nominal GDP, coupled with a financial component, proxied by the capitalisation of global stock and bond markets, that balances the overall relationship,” WGC said. “Third-party inputs are then used to estimate long-term expected returns for gold.”

They argued that while the “bulk of existing research places financial investment at the forefront of price determination for gold, [and] the short-term impact of financial markets is undeniable, the long-term importance of other sources of buying is even more so.”

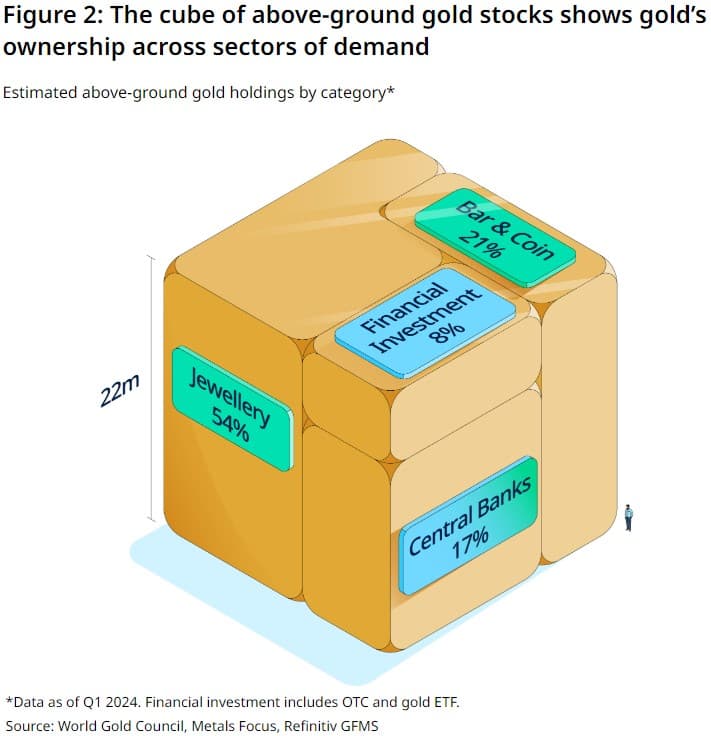

For that reason, they created the “cube,” which depicts the above-ground stock of gold, estimated to be 212,582 tonnes, as a “balance sheet snapshot of gold ownership.”

“It is remarkable for a number of reasons,” WGC said. “The cube illustrates how the total stock of this ubiquitous metal could occupy a physical space barely larger than three Olympic-sized swimming pools. In addition, it reveals how little financial investment – (referring here to physically backed gold ETFs and over-the-counter (OTC) physical holdings) has been amassed by market participants over the years in relation to other sources of demand – a misleading statistic given the vast volumes of gold that flow through financial centers every day.”

Since this depiction shows that much of the available supply of gold is not owned via financial instruments, WGC said this “implies that any explanation of its total distribution must consider factors beyond those solely linked to the day-to-day decisions of financial market participants.”

“The distribution of the cube also suggests that the price of gold has been driven by two distinct components: an economic component combined with a financial component,” they said.

Focusing on gold’s key drivers, WGC said, “Gold’s performance responds to the interaction of its roles as a consumer good and as an investment asset. It draws not only from investment flows but also from fabrication and central bank demand.”

To better understand gold's behavior across time, they identified four key drivers to monitor: “Economic expansion: periods of growth are supportive of jewellery, technology and long-term savings; Risk and uncertainty: market downturns, inflation and geopolitical risk often boost investment demand for gold as a safe haven; Opportunity cost: the price of competing assets, including bonds and currencies, influences investor attitudes towards gold; and Momentum: capital flows, positioning and price trends can boost or dampen gold’s performance.”

They highlighted these drivers to help overcome the “common pitfall in establishing an expected return for gold when using historical data to test a theory empirically.”

“Generally, more history is preferable to less, as more observations increase one’s confidence in the analysis,” the report said. “Capital market assumptions for long-term stock and bond returns commonly use data from 1900 or earlier. Replicating this for gold creates one glaring issue: for the best part of the 20th century, gold prices were determined by the conversion rate established by central banks and governments.”

“This means that gold was money, linked to the US dollar at a fixed price that was only adjusted sporadically,” they underscored. “As such, investors were not always able to use it in practice as an inflation hedge or an equity market hedge. And in the US, citizens were barred from acquiring gold as an investment from 1933 to 1974.”

“For gold, while its historical performance during Gold Standard periods is an interesting reference, it is truly its market structure and behaviour post-1971 that matters most,” they highlighted. “By way of an example, to value a company and assess its expected return, one needs to apply the analysis to the business it will be rather than to the business it has been. If the two are materially different, then past is not prologue.”

The WGC gave the example of Nokia, which was originally “established as a manufacturer of rubber cable and boots until the early 1990s when it morphed into one of the global leaders in the telecoms industry. Applying valuation metrics to Nokia as a boot maker in the early 1990s would have been as fallible as valuing gold in 2024 based on its performance as money during the first half of the 20th century,” they said.

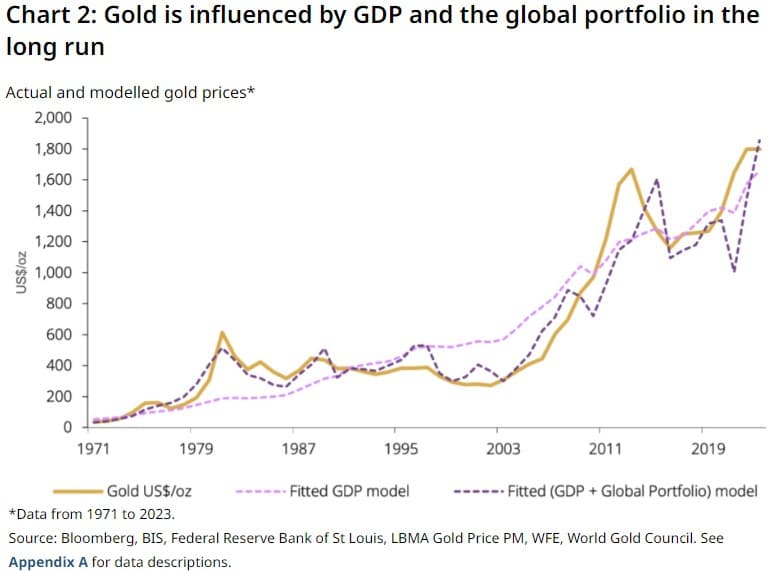

To more accurately determine gold’s performance, WGC proxied “the economic and financial components using real-world economic and financial variables.”

“Our economic component proxy is global nominal GDP in US dollars. Nominal GDP comprises real GDP, an inflation component (the GDP deflator), and a currency component – used to convert local GDP to US dollars,” they explained. “This captures the flow of capital from income to gold.”

“Our financial component is proxied using the capitalisation of global equity and bond markets – the global portfolio – in US dollars,” they added. “It captures the investments available for investors to reallocate income and wealth. It is important to note that we are looking at market capitalisation, accounting for both quantity of float and issuance, not just prices. We assess the influence of each of these variables using regression analysis. The analysis reveals that GDP is the primary driver of the gold price in the long run.”

After conducting regression analysis comparing “a simple regression to examine the co-movement of gold prices with only GDP” with the GLTER model, which adds global portfolio capitalization, WGC said that “Once growth as the primary driver of gold prices has been accounted for, we are left with this substitution effect between gold and the global portfolio.”

“Importantly, the negative coefficient on the global portfolio does not mean that it lowers the price of gold, but that it makes it appreciate at a lower rate,” they noted. “In this case, both the Phillips-Perron test and a Johansen cointegration test clearly indicate that there is a long-run relationship and equilibrium between gold prices and the two components.”

“Additional regressions show that individually, stocks and bonds each have a negative coefficient when included with GDP in a two-variable system, adding credence to the above finding,” they added. “The use of two variables rather than one yields a better fit with the price of gold. While it is not surprising that two variables provide a better fit than one, it is notable that the financial variable significantly reduces the deviations from the long-term relationship.”

“Crucially, using only an economic component to explain gold prices produces a model with rather prolonged periods of disequilibrium,” WGC highlighted. “Accounting for gold’s dual nature makes for a much more nuanced explanation of gold’s long-run price path.”

Combining all the data together, WGC’s “analysis suggests that gold’s long-term expected returns are explained by three parts global nominal GDP growth less one-part global portfolio growth,” they said.

Based on the GLTER model, gold was found to have “an 8.6% annual average return for the period 1971–2024, versus an actual return of 8% over that period. Using external forward estimates for GDP growth and the global portfolio, the model predicts an annual average return of 5.2% for the next 15 years.”

“The estimated average gold return over the 2025-2040 period in excess of 5% per year is well above that produced by most other models,” WGC said. “Specifically, the estimate exceeds common long-term return assumptions such as a zero real return (2.5% nominal in line with expected CPI inflation) over the next 15 years or a gold return equivalent to the risk-free rate (2.9% for short-term US Treasury bills).”

WGC cited “a lower expected growth in global GDP” as the reason the projected return over the next 15 years is lower than the observed historical return.

“However, all asset returns are likely to be impacted,” they said. “For example, estimates for intermediate US Treasury bonds and World government bonds over the same period are 3.9% and 4.8%, respectively. And US large cap stocks are expected to grow at a 7% annual rate – below their 20-year return.”

“In our view, any model that fails to account for economic growth alongside financial factors will prove insufficient in establishing gold’s long-term expected return,” WGC said. “Our novel contribution highlights the theoretical and empirical importance of economic growth and gold’s role in global portfolios in driving gold prices in the long run.”

“GLTER complements our other gold pricing models, GRAM and Qaurum, where economic expansion is present but not a central driver given their short- and medium-term focus,” the report concluded. “And it explains why gold’s long-term return has been and will likely remain, well above inflation.”