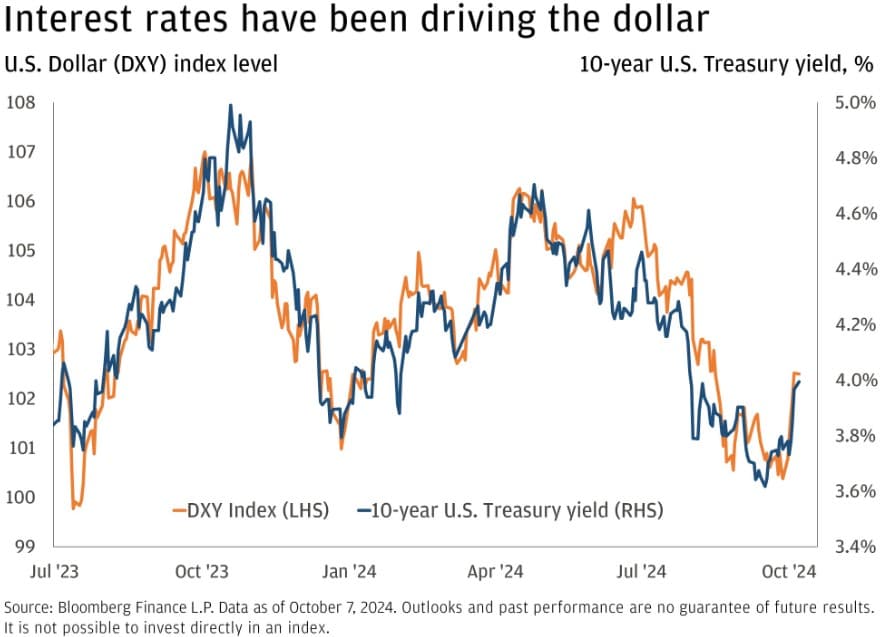

(Kitco News) – The U.S. dollar has seen a rebound in recent weeks, with the dollar index (DXY) climbing from 100.185 on September 30 to a high of 104.58 on Monday. But with the strength of BRICS rising and other headwinds mounting, analysts at JPMorgan asked the question top of mind for many global investors: can King Dollar continue its reign?

“Currency volatility has reached its highest level since May 2023 as investors contend with geopolitics uncertainty and recalibrate bets for the rate-cutting cycle ahead,” JPMorgan investment strategists Matthew Landon and Samuel Zief wrote.

They highlighted the conflict in the Middle East and interest rate cuts as the primary drivers of volatility in the currency market.

“Although it is the human impact that is our primary concern at this time, it is important to address the impact of developments in the Middle East on markets, too,” they said. “To that end, the impact on oil prices feels most intuitive. However, such events often spark a ‘flight to safety’ for investors – where assets like the dollar and gold tend to benefit from inflows.”

Regarding the global cutting cycle, they noted that “All in the space of a week, Fed Chair Powell talked down the prospect of another 50 basis point (bps) cut in November, a red-hot September U.S. payrolls report showed a resilient labor market, central bank heads in Europe (ECB and BoE) hinted at a faster pace of cuts, and Japan’s new Prime Minister suggested further rate increases weren’t needed for now.”

“That improves the attractiveness of U.S. interest rates for global investors relative to other regions – driving the dollar higher,” they said. “But that is just one week. Looking at the bigger picture shows a broader USD downtrend starting to emerge since the summer.”

Prior to the week ending October 4, they noted that “it had been nine weekly losses in the previous ten weeks for the dollar.”

Landon and Zief said the moves in the DXY have “closely tracked swings in interest rates,” leading them to ask if the dollar is “on the edge of a new dollar regime?”

“Despite the recent softness in the dollar, current levels still embed a 5-10% premium relative to what its historical relationship with interest rates would suggest,” they said. “That will likely continue to unwind at some point over the coming years, but before we see that, we would argue that there are three necessary conditions for USD to weaken materially: Certainty over Federal Reserve rate cuts; Global (ex-US) growth improvement; and Positive risk sentiment.”

“The first condition looks to have been met by this point,” the analysts said. “The pace of cuts might not be so clear, but the Fed has clearly indicated its intention to lower interest rates to support the labor market as inflation risks fade.”

They noted that while progress has been made on the other two conditions, “the story is less clear-cut.”

“Stimulus announcements from China boost the prospect for growth outside the U.S., but activity data generally remains weak (especially in Europe),” Landon and Zief said. “And while risk assets have kept rallying this year to support higher-beta currencies against the dollar, the recent uptick in volatility poses risks to that trend.”

“Until we see more certainty over those conditions, it is difficult to envisage another leg lower for USD,” they noted. “At this point, that feels like it will be more of a 2025 story – particularly given the risks surrounding the upcoming U.S. Presidential election. Considering how to diversify foreign exchange holdings ahead of that time could be prudent.”

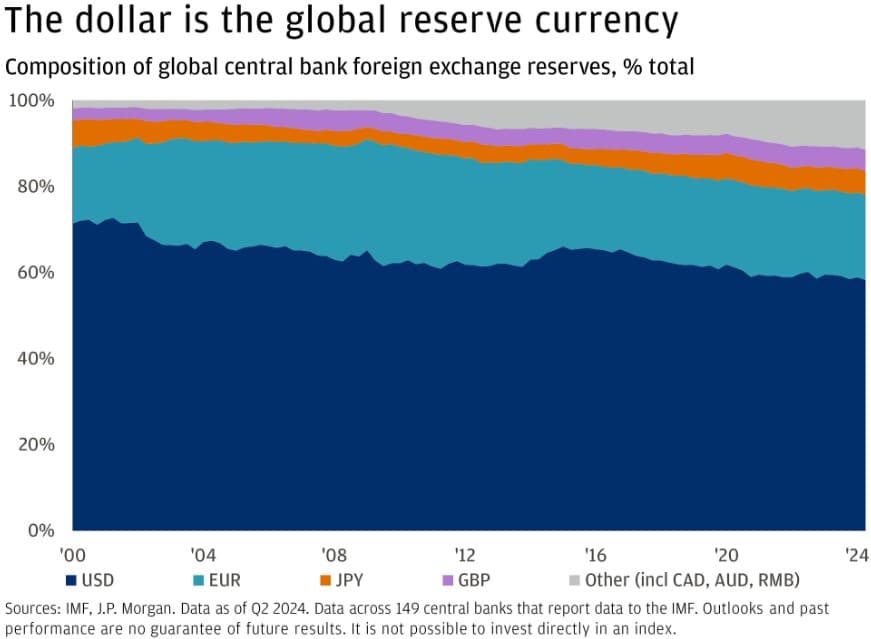

As for how to go about currency diversification, they highlighted that “The dollar is often considered the ballast for currency allocations, and rightfully so. It accounts for 60% of global foreign exchange reserves, 55% of banks’ foreign currency liabilities and claims, and makes up one side of 90% of all FX transactions. It is well and truly the global reserve currency.”

“However, the basics of investing tell us that you should not be putting all of your eggs in one basket,” they stressed. “Each situation is different depending on an individual’s day-to-day spending needs. Naturally, those that live and pay taxes in the UK will need more pounds than a Danish farmer that hasn’t left their home country.”

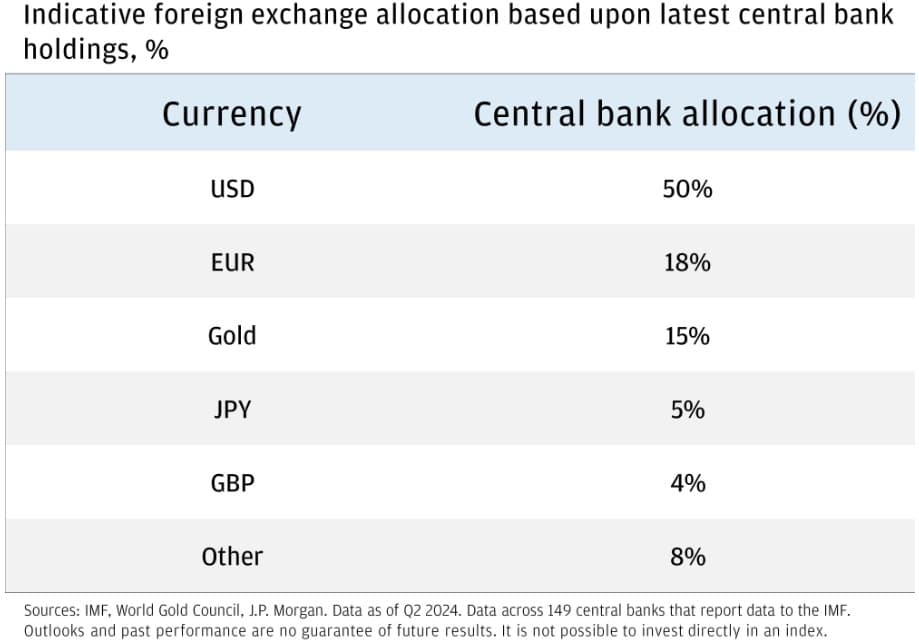

“But from a pure diversification standpoint, we look to central banks as a starting point,” they said. “Like many investors, central banks have very long time horizons, a primary objective to preserve purchasing power, and a priority for liquidity and safety while also seeking out some return. With nearly $13 trillion in assets under management, their bias is to overweight currencies with deep, liquid financial markets that have a large universe of investable assets.”

Landon and Zief noted that central banks' “largest non-USD allocations are to securities denominated in euros, Japanese yen, and British pounds, along with a few others for diversification purposes like the Chinese renminbi, Swiss franc, Australian dollar or Canadian dollar.”

“In recent years, gold has become an increasingly important diversifier for central banks too,” they added. “Given its nature as a physical store of value, gold has grown in popularity as geopolitical tensions have flared. Gold allocations now account for roughly 15% of global reserves.”

“As we evaluate portfolios in the final months of the year, level setting and rebalancing currency allocations is important,” they said. “For example, with the view that the dollar could weaken over the medium-term, an investor fully invested in dollars today could start by converting a certain amount to another currency. Considering that in the context of a wider portfolio is also important.”

“An investment portfolio heavily weighted towards stocks might not require as much exposure to currencies like the pound or Canadian dollar given their pro-cyclical nature,” they concluded. “The likes of the dollar, Japanese yen and gold might be preferred in such a situation to smooth out volatile periods due to their more defensive nature.”