(Kitco News) - The gold market was edging lower after the latest U.S. data showed growing momentum in the service sector but further weakening in manufacturing.

S&P Global reported on Monday that its flash Purchasing Managers Index (PMI) for the service sector rose to 58.5 in December, up from November’s reading of 56.1. Activity in the service sector exceeded expectations, as economists had forecasted a reading of 55.7.

The report highlighted that activity in the service sector reached its highest level in over three years.

Meanwhile, the U.S. manufacturing sector continued to contract. According to the report, the PMI for the manufacturing sector fell to 48.3, down from November’s reading of 49.7 and also below the consensus forecast of 49.4.

S&P Global noted that activity in the manufacturing sector hit a three-month low in December.

“[G]rowth remained heavily skewed toward the service sector, where an acceleration of growth contrasted with a steepening decline in manufacturing,” the report said.

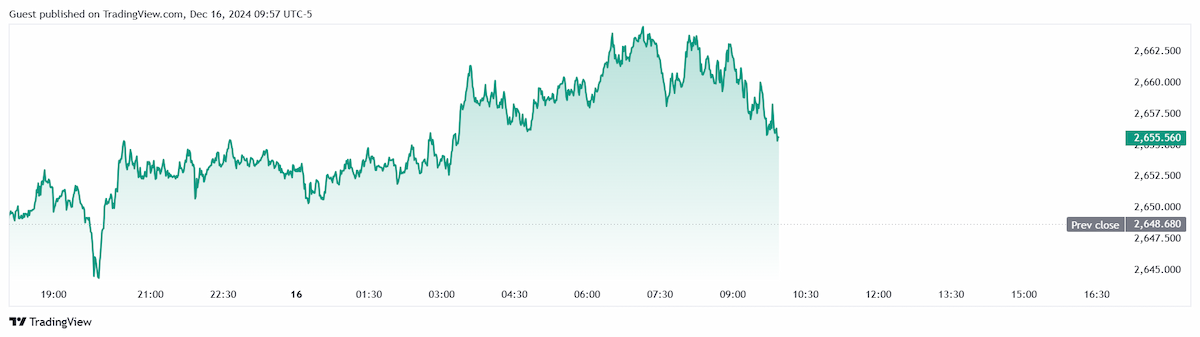

The gold market continued to come off its earlier highs following the PMI data release, but remained well off session lows. Spot gold last traded at $2,655.43 per ounce for a gain of 0.25% on the day.

“Business is booming in the US services economy, where output is growing at the sharpest rate since the reopening of the economy from COVID lockdowns in 2021,” said Chris Williamson, Chief Business Economist at S&P Global Market Intelligence. “The service sector expansion is helping drive overall growth in the economy to its fastest for nearly three years, consistent with GDP rising at an annualized rate of just over 3% in December.”

“It’s a different picture in manufacturing, however, where output is falling sharply and at an increased rate, in part due to weak export demand,” he added.