(Kitco News) – Gold prices held up remarkably in December even as the U.S. dollar strengthened and traders booked profits, and debt concerns, central bank purchases, and geopolitical risks should support investor interest for the yellow metal in January, according to the World Gold Council (WGC).

In their latest Gold Market Commentary, WGC analysts wrote that gold’s value declined less than would otherwise be expected, with a positive outlook and higher risks limiting outflows.

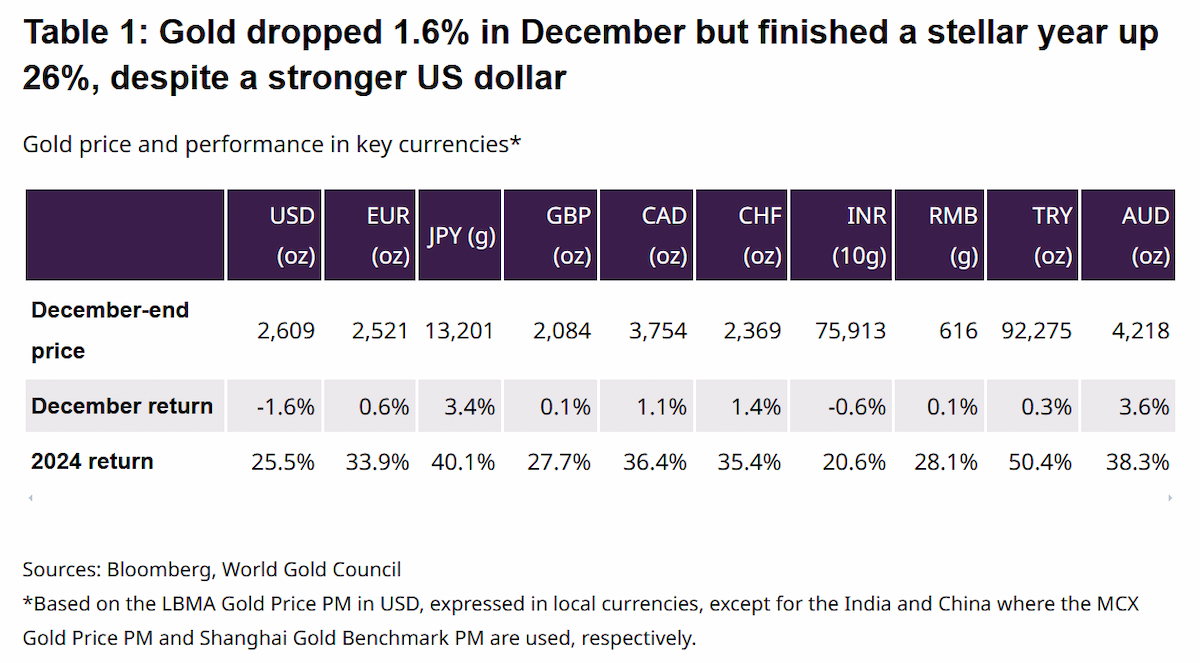

“Gold gave back a little more of its y-t-d gains in December, finishing down 1% on the month, but up 26% on the year,” they noted.

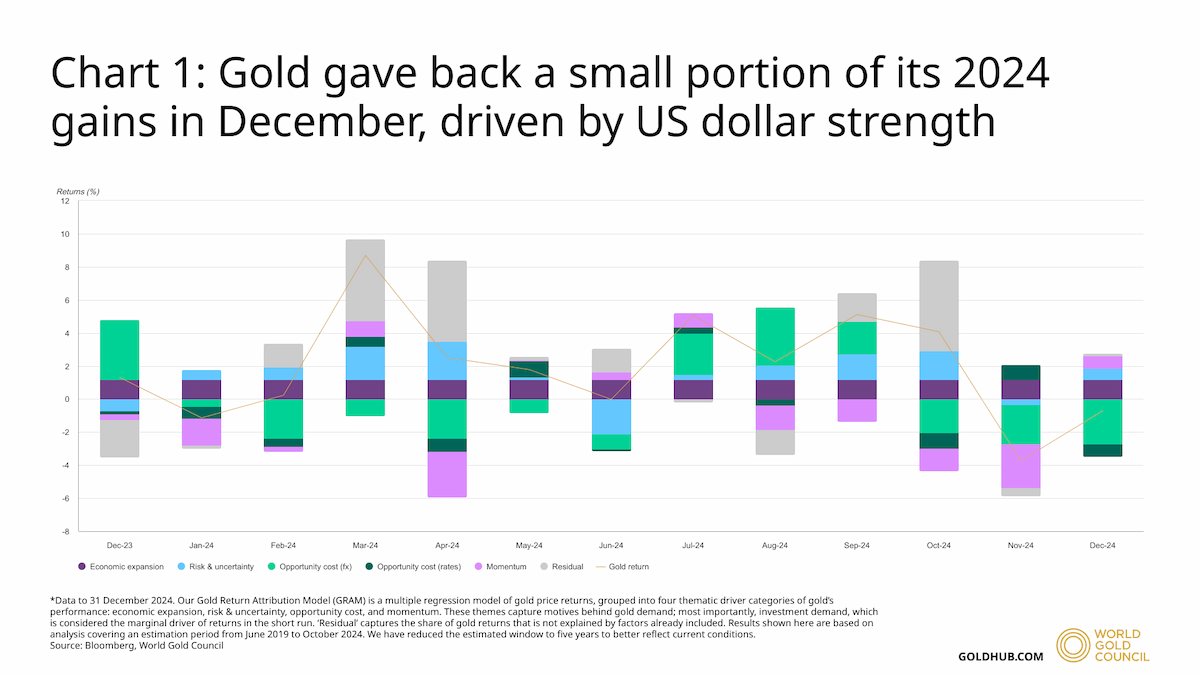

“According to our Gold Return Attribution Model (GRAM), the primary driver for gold’s decline was a strong rally in the US dollar index (opportunity cost FX) which finished the year at its high,” the analysts said. “Softening gold’s drop were a rise in breakeven inflation expectations and the Geopolitical Risk index (risk & uncertainty), likely on the back of martial law declared in South Korea, as well as small global gold ETF inflows (momentum).”

While December saw significant outflows from North American gold ETFs, global flows were positive thanks to strong Asian ETF buying. “Those outflows were quite benign given the weakness in November and the prospect of profit-taking following such a strong year,” they noted. “A positive sell-side outlook for gold probably helped constrain a bigger end-of-year shift out of gold. Profit-taking also likely occurred in futures, where somewhat extended managed money net longs shed US$4bn (-49t) over the month, taking total net positions down to US$65bn (764t).”

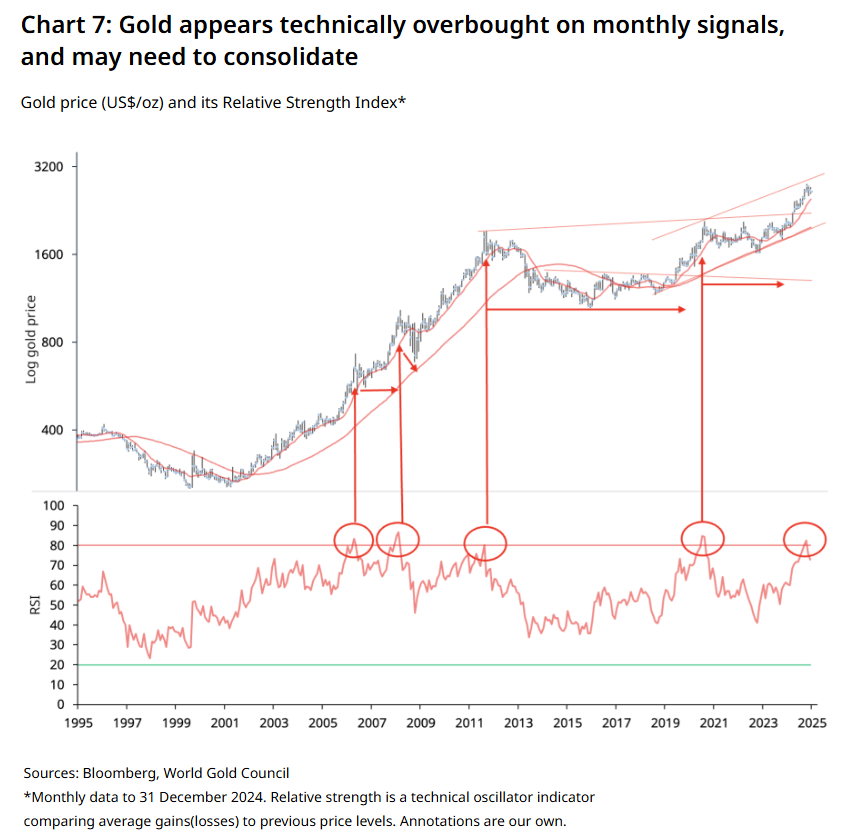

Looking forward, the WGC believes that the ongoing uncertainty in the bond market will likely fuel interest in gold in January, but they cautioned that technical signals still suggest overbought conditions for the precious metal.

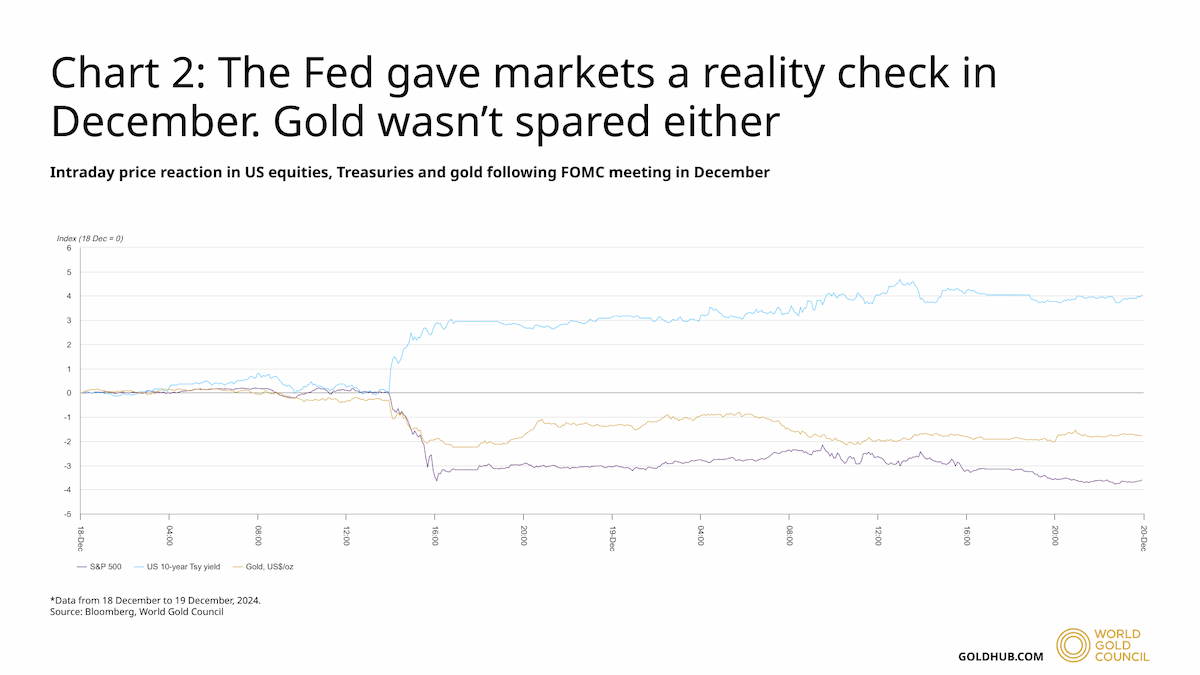

“A 25bps Fed policy rate cut in December, doused with further hawkish guidance, resulted in sizeable intraday wobbles in equities, US Treasuries and gold,” the analysts wrote. “The S&P 500 fell by 3%, and the 10-year Treasury yield marked the largest FOMC-meeting move since 2013. Gold dropped by over 2%. Undoubtedly, the Fed’s sober messaging prompted some investors to take profit following a stellar year for equities and gold, with tax-loss selling an additional incentive to cut equity exposure.”

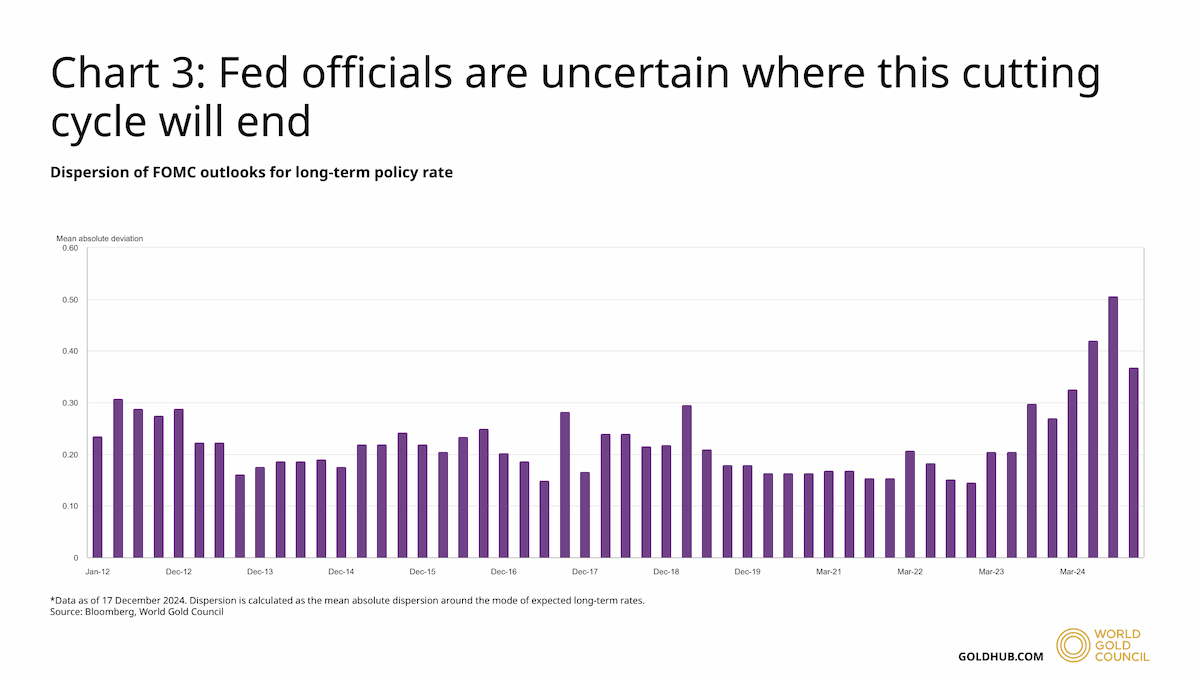

“The reaction probably also reflected some pent-up uncertainty that markets, as well as the Fed, soon face a change in personnel at the helm of the US economy come January 20,” they noted. “While the FOMC members are somewhat confident in where interest rates will be at the end of 2025 – they are unusually divided on where rates will be at the end of this cutting cycle.”

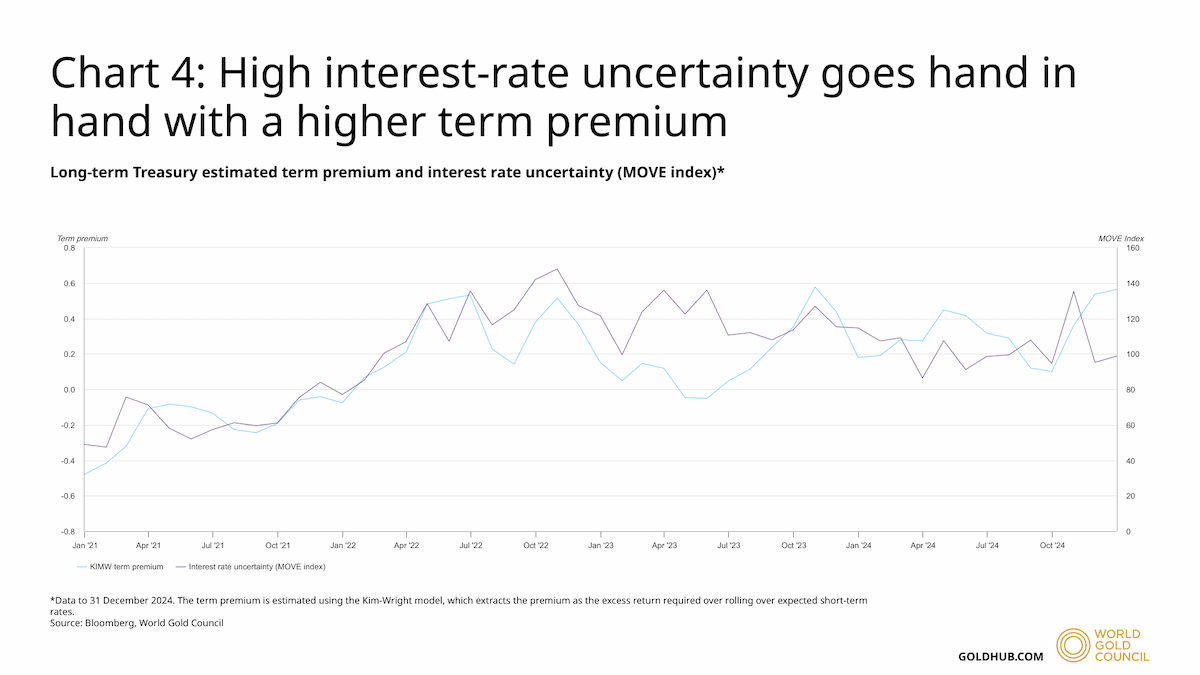

This uncertainty surrounding interest rates was also reflected in the elevated level of the MOVE index, which is an options-based measure of implied volatility in bonds. “This is partly the result of two months of positive inflation surprises in the US,” the analysts said. “But elevated debt and deficits are arguably also factors. Interest rate uncertainty should favour gold relative to bonds as it raises their associated premia, at least through January with debt ceiling wrangling and the US presidential inauguration on the cards.”

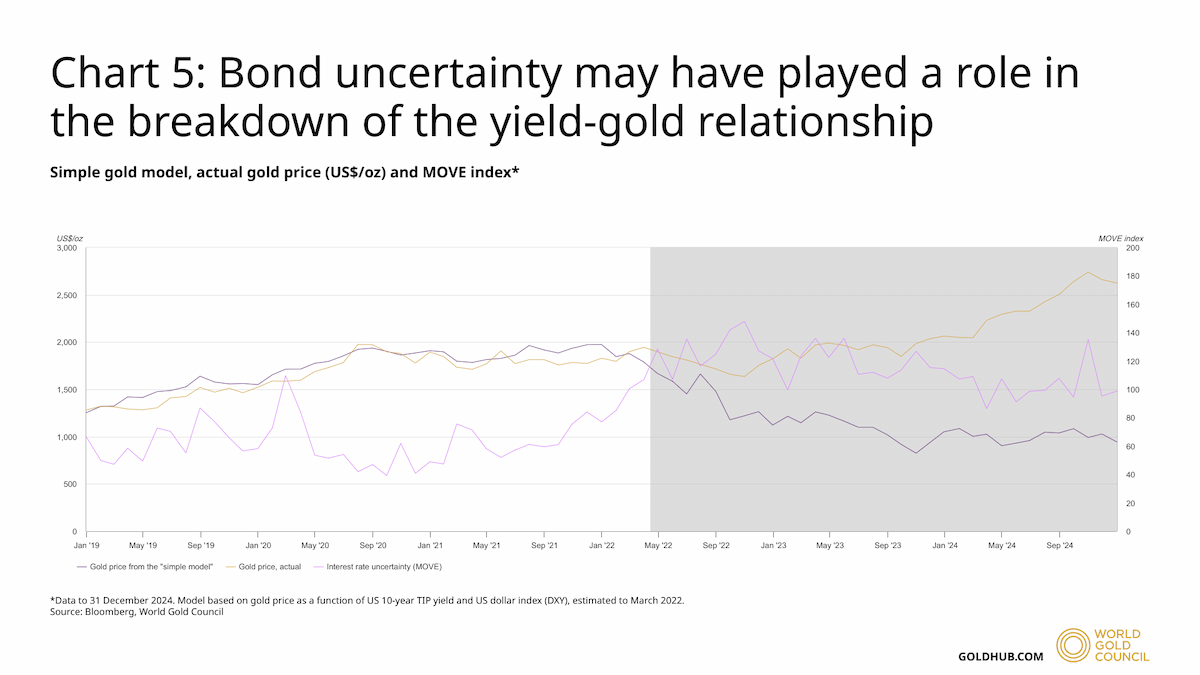

The WGC also pointed out the well-documented, a breakdown in the relationship between gold and real interest rates that has unfolded over the past two years. “We have in the past attributed the phenomenon largely to emerging market central bank buying and geopolitical risk premia. But perhaps bond uncertainty has also played a role,” they said.

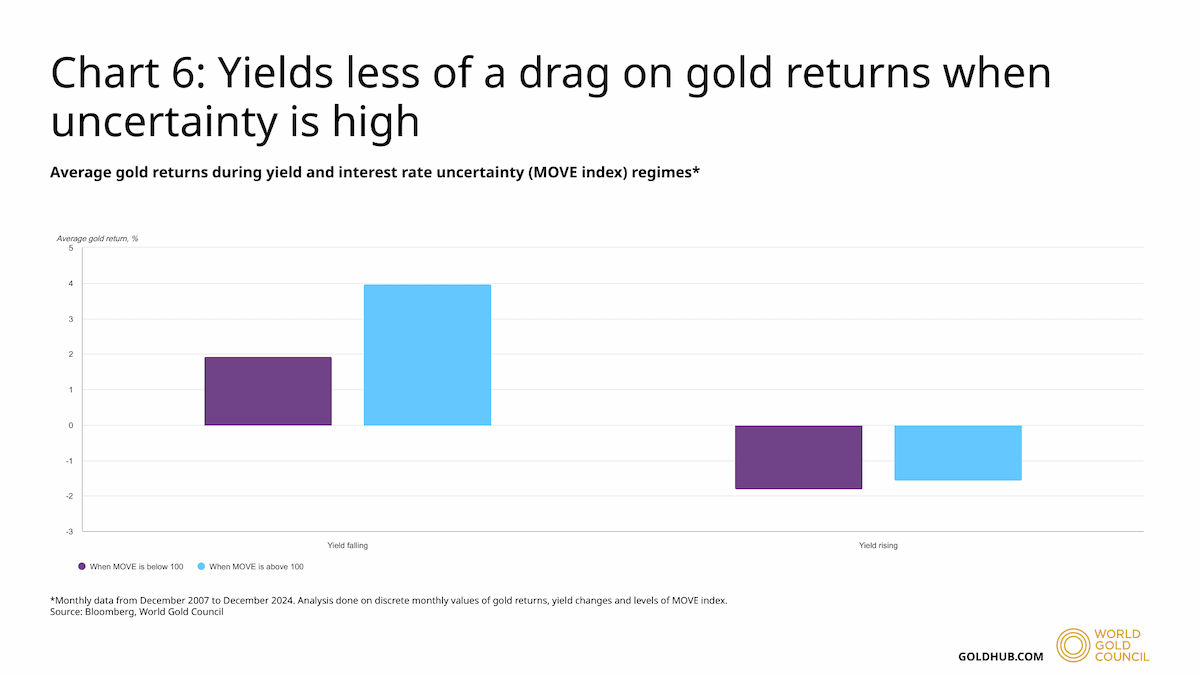

“Data suggests that when interest rate uncertainty – as measured by the MOVE index - is high, yield trajectory appears to exert less of a drag on gold returns than when it is low,” the analysts noted.

“It also looks like this is a statistically significant difference, if we regress gold returns on a real yield component with an interaction dummy for when the MOVE index is above 100 (it has recently risen to 99),” they said. “The normal sensitivity is more than halved when bond uncertainty is high, even accounting for moves in the US dollar index. Thus, alongside central bank demand and geopolitical risk, it may further explain why the traditional simple real rate model hasn’t been quite as accurate over the past two or so years as it was post the global financial crisis up to 2022.”

The WGC believes gold “is unlikely to take much of a negative cue from bond yields” until debt concerns, central bank purchases, and geopolitical risks diminish.

“To add fuel to the fire, bond market uncertainty might get amped up in January again as the Biden administration carves out its last twenty days in office,” they added. “And debt ceiling jitters are set to resurface in the middle of the month when the Treasury could be forced into extraordinary measures to avoid a debt default, as warned by the incumbent Treasury Secretary, Janet Yellen.”

But while all the uncertainties are providing support for gold prices, the yellow metal may also be a victim of last year’s success as the technical picture suggests it may still be somewhat overvalued.

“Technically, gold will have to battle what looks like overbought territory for some time,” the analysts said. “The long-term structural uptrend may get challenged in early 2025 as monthly momentum indicators suggest a ‘sell’ signal after five months in extreme overbought territory, with similar signals seen at the peaks in 2006, 2008, 2011 and 2020. Longer term, the core uptrend looks well cemented and any near-term weakness could be viewed as an opportunity for investors to re-engage in gold at more attractive levels.”