(Kitco News) – Professional investors see gold as a hedge against inflation, financial market turbulence, economic stress, and geopolitical chaos, but its number one use in their portfolios is as a diversifier, according to a new survey from Wisdom Tree.

Gold is an excellent portfolio diversifier, wrote Nitesh Shah, Head of Commodities and Macroeconomic Research at WisdomTree Europe, because it enables investors to improve returns while effectively managing risk.

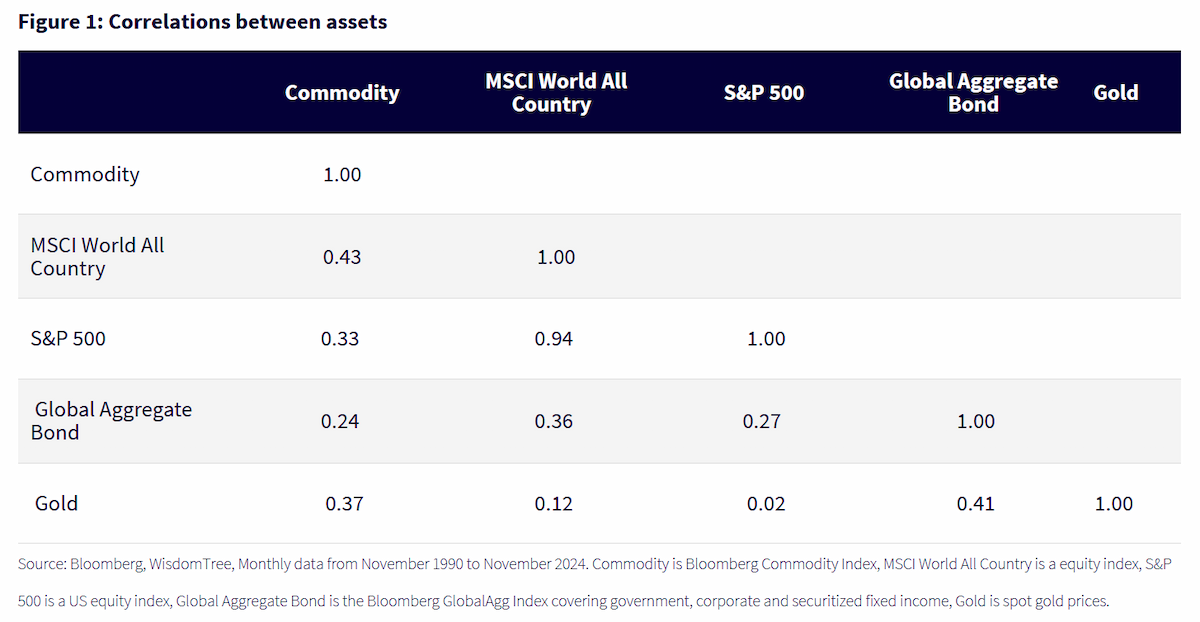

“36% of 800 professional investors surveyed by WisdomTree noted ‘diversification’ as their primary reason for holding gold,” he said. “Our analysis shows that gold has a low correlation with both equities and bonds and, thus, should contribute strongly to a diversification effort.”

Shah pointed out that gold behaves very differently from other assets. “On the one hand, it is a defensive asset, often competing with bonds as a safe harbour against broader market volatility,” he said. “On the other hand, it has cyclical traits because it rises in times of inflation, which is often generated in periods of strong economic growth. This duality of gold helps explain its low correlation with traditional assets.”

35% of respondents to the Wisdom Tree survey cited ‘inflation hedge’ as the second most popular reason to hold gold, followed by ‘financial market volatility hedge’ (31%) and ‘geopolitical volatility hedge’ (27%).

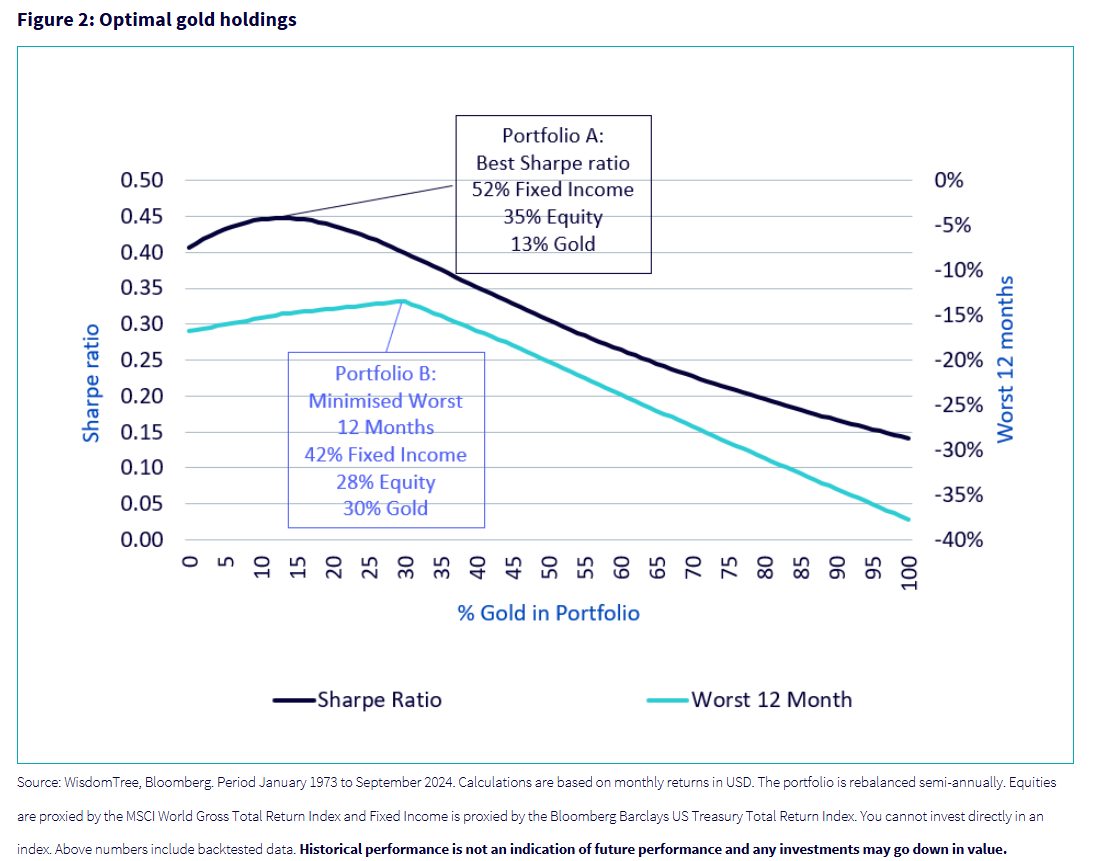

“Putting gold into a portfolio of other assets can increase a portfolio’s Sharpe ratio and reduce worst 12-month performances,” Shah noted. To illustrate how gold functions as a defensive asset, Shah used an example based on the 52 years of data from 1973 to 2024.

“We start with a portfolio of bonds (60%) and equities (40%) and no gold: that is the 0 point on the horizontal axis,” he said. “The Sharpe ratio of this portfolio is 0.41 and the worst 12-month performance is -17%. As we move along the horizontal axis we introduce some gold to the portfolio. The remainder of the portfolio maintains a 60/40 ratio of bonds to equities.”

“As we increase gold holdings, Sharpe ratios rise and worst 12-month performances decline, up to a point (before they deteriorate again),” Shah wrote. “The maximum Sharpe ratio (portfolio A) is achieved with 13% gold (where the remainder of the portfolio is 52% bonds and 35% equities). The Sharpe ratio is 0.45 in this portfolio. The minimum worst 12-month performance (portfolio B) is achieved with 30% gold (where the remainder of the portfolio is 42% bonds and 28% equities). The worst 12-month performance is -13% in this portfolio.”

However, the results of the survey show that the mean average holding of gold in the portfolios of professional investors is only 5.42%, which is well below the optimal amount to maximize the Sharpe ratio. “In fact, less than 14% of investors surveyed hold enough gold to maximise their Sharpe ratio (assuming equities and bonds are the mainstay of their portfolio),” he noted.

After diversification, the next three reasons respondents held gold related to the hedging of various risks. “[B]ut what is the market’s perception of those risks today and how could they evolve?” he asked.

The first risk area related to the stability of the financial system. “Several metrics gauge market anxiety, including the VIX and MOVE alongside direct investor surveys,” Shah said. “At present, none of these measures indicate immediate concern. However, risks can escalate rapidly, as seen in August 2024, when a yen carry trade unwind sparked fears across global financial markets. With various equity indices reaching all-time highs—and concerns that these gains are heavily concentrated—many investors are seeking ways to hedge against a potential market reversal. Gold serves as a key tool in this context.”

Economic risks are the second area of concern. “The global economy has shown resilience through the past cycle, with the likelihood of a recession in the next year considered low,” Shah said. “However, policy uncertainty remains a significant concern for many investors.”

“In the United States, a new administration has risen to power with a strong focus on trade policies. Should President-Elect Trump impose new tariffs, rather than using them as negotiation tools, it could pose challenges to global economic growth,” he added. “In this scenario, gold may become a preferred asset for hedging these risks.”

The final set of risks cited by professional investors were geopolitical.

“Throughout 2024, gold prices were supported by heightened geopolitical tensions,” Shah wrote. “The Russia-Ukraine war and the Israel-Hamas/Hezbollah conflicts dominated investor concerns. More recently, the fall of the Assad regime in Syria has created uncertainty, particularly for Russia, a key ally of Assad. Russia’s military bases in Syria now face an uncertain future, raising concerns about potential escalations. In November 2024, Ukraine’s use of US and UK-supplied long-range missiles prompted retaliatory strikes from Russia Coupled with amendments to Russia’s nuclear doctrine, fears of further escalation remain.”

“President-Elect Trump has promised a swift resolution to the Russia-Ukraine conflict,” he added. “However, achieving this without significant concessions from Ukraine and NATO seems unlikely, suggesting that geopolitical risks may persist.”

Shah also noted that Iran now faces a similarly precarious situation. “The weakening of Hamas, Hezbollah, and the Assad alliance undermines Iran’s regional influence,” he said. “Additionally, the US may enforce sanctions against Iran more rigorously, which could prompt unpredictable responses from Tehran.”

“Despite speculative positioning in gold futures slipping slightly—from over 300,000 contracts net long in early October 2024 to just below that level today—the ongoing geopolitical tensions may drive positioning higher once again.”

“Professional investors rightly view gold as a hedge against inflation, financial market turbulence, economic stress, and geopolitical chaos,” Shah concluded. “While some of these risks may not be at the forefront of investors' concerns today, hedging against the potential escalation of tail risks remains highly valuable.”

Wisdom Tree’s own analysis also supported respondents’ most widely held belief that gold is an effective portfolio diversifier. “Our analysis confirms that incorporating gold into a portfolio enhances overall outcomes, improving returns while effectively managing risk,” he added.