(Kitco News) - Central banks continue to dominate the gold market, collectively buying more than 1,000 tonnes of gold in 2024 for the third year in a row and accounting for roughly 20% of total demand last year.

In its annual and fourth-quarter Gold Demand Trends report, published Wednesday, the World Gold Council said that total physical gold demand rose to 4,974 tonnes for the year, a record high.

The report noted that record demand helped drive gold prices to consecutive all-time highs. Quoting price data from the London Bullion Market Association, the average gold price in the fourth quarter rose to a record high of $2,663 an ounce. The average price for the year rose to $2,386 an ounce, up 23% compared to the average annual price in 2023.

“The combination of record gold prices and volumes produced a Q4 value of $111 billion. This took 2024 over the line to reach the highest-ever annual value of $382 billion,” the report said.

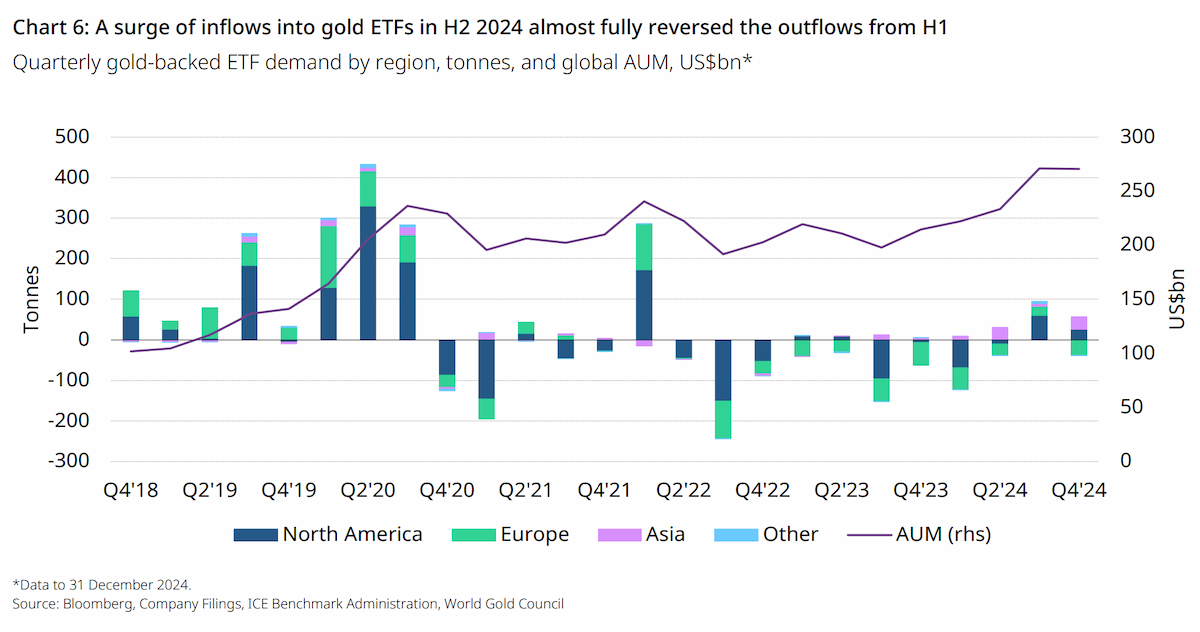

Along with central bank demand, the report said that investment demand for the yellow metal hit a four-year high as over-the-counter (OTC) demand outweighed relatively neutral demand for gold-backed exchange-traded funds.

“2024 marked the first year since 2020 in which holdings were essentially unchanged, in contrast to the heavy outflows of the prior three years,” the analysts said in the report.

Total investment demand increased to 1,179.5 tonnes, an increase of 25% from 945.5 tonnes in 2023.

In an interview with Kitco News, Joseph Cavatoni, market strategist at the WGC, said that consumption data continues to show that gold has reestablished itself as an important global financial asset.

“The use cases for holding gold are clear and understood,” he said. “When we look at central bank demand, their rationalization for owning gold remains very strong. The growing government debt burdens and the dramatically changing geopolitical landscape suggest that central banks will continue to buy gold.”

Looking ahead, Cavatoni said that renewed geopolitical uncertainty caused by the unpredictability of the new Trump administration sets the ground for further central bank demand.

“Having positively surprised for three years in a row, there’s more evidence that supports the idea that central banks can again repeat their 1,000t-plus net buying in 2025. However, we reserve caution by reflecting it in potential downside risk rather than our central view,” WGC analysts said in the report. “We believe that armed conflict shifting to global trade and economic conflict may support central banks' net buying trend.”

At the same time, rising equity market uncertainty, increasing inflationary pressures, and stagnating economic growth are expected to push generalist investors back into the gold market through ETFs.

"We see tailwinds for gold ETFs, OTC, and futures-based investment stemming from generally lower interest rates, richly valued equities, a softer U.S. dollar, and geopolitical risk, mostly expressed through trade and economic uncertainty."

Cavatoni said that, overall, the broader trend is that given all the uncertainty in the marketplace, demand for gold will remain high through 2025, even at elevated gold prices.

While the ETF market is expected to attract new investor attention, the WGC is forecasting that bar and coin demand will remain healthy but lower compared to last year, as higher prices weigh on consumer purchasing power.

According to the report, global bar and coin demand totaled 1,186.3 tonnes, roughly unchanged from 1,189.8 tonnes in 2023. The WGC sees a similar outlook for 2025.

“In the West, economic malaise in Europe and high prices are likely to weigh on demand, as will declining inflation fears and conflict risk, but lower interest rates might attract European activity back in the second half of the year. In the U.S., Republican presidencies have historically been accompanied by below-average bar and coin demand; however, the geopolitical environment could soften the pullback,” the analysts said.

The Jewelry Sector Is a Weak Spot for the Gold Market

Although the gold market saw historic demand in 2024, record-high prices in global currencies took a toll on jewelry demand.

The report said that total jewelry demand dropped to 1,877.1 tonnes, a decline of 11% from 2,110.6 tonnes reported in 2023.

“With the exception of the COVID-stricken 2020, when demand crashed below 1,400 tonnes, we need to go back to 2009 to find the last comparable year for gold jewelry demand,” the WGC said.

One interesting facet of the market is that India once again became the world’s biggest gold-consuming nation, as weak demand was particularly sharp in China.

Chinese jewelry demand dropped to 479.3 tonnes, down 24% from the previous year’s total of 630.2 tonnes.

“The environment for Chinese jewelry demand was very challenging throughout 2024, hit by a combination of poor consumer confidence due to declining income growth and surging gold prices. The jewelry retail sector faced challenges, and stores closed throughout the year,” the analysts said.

Meanwhile, India saw its jewelry sector decline by 2% last year, consuming 563.4 tonnes of gold.

“The fact that annual demand only shrank by 2% during a year in which the gold price reached multiple record highs is a testament to the resilience of gold jewelry demand in India, highlighting both the strength of the response to the July duty cut and the country’s relatively healthy economic growth,” the analysts said.

A.I. Evolution Is Also Driving Gold Demand

While the tech sector and AI drove equity markets to record highs last year, it is a sector largely ignored in the gold market. However, it saw solid growth last year, rising to its highest level in four years.

Last year, the technology sector consumed 326.1 tonnes of gold, an increase of 7% from 2023.

“During 2024, electronics demand (the dominant category of demand in this sector) was bolstered by ongoing strength in AI-related applications and some recovery in the consumer electronics markets after a particularly weak 2023,” the WGC said.

While robust demand drove gold prices higher last year, it also spurred an increase in supply. The WGC said that global gold supply increased by 1% last year to a new record high of 4,974.5 tonnes.