(Kitco News) - Gold continues to attract significant investor attention, and one research firm not only expects prices to move higher, but also believes investors need to hold significantly more of the precious metal than they currently do.

In a recent report, analysts at FTSE Russell said that gold has once again reestablished itself as an important neutral monetary asset as the global economy fragments. Co-authors Sayad Reteos Baronyan, Director of Multi-Asset Research, and Alex Nae, Quantitative Research Analyst, stated that gold has become an essential diversification tool as bond and equity markets struggle in a world marked by rising uncertainty and higher inflation.

“[Gold] is no longer merely a defensive store of value, but a dynamic, strategic tool for navigating complexity in the multi-asset space,” the analysts said.

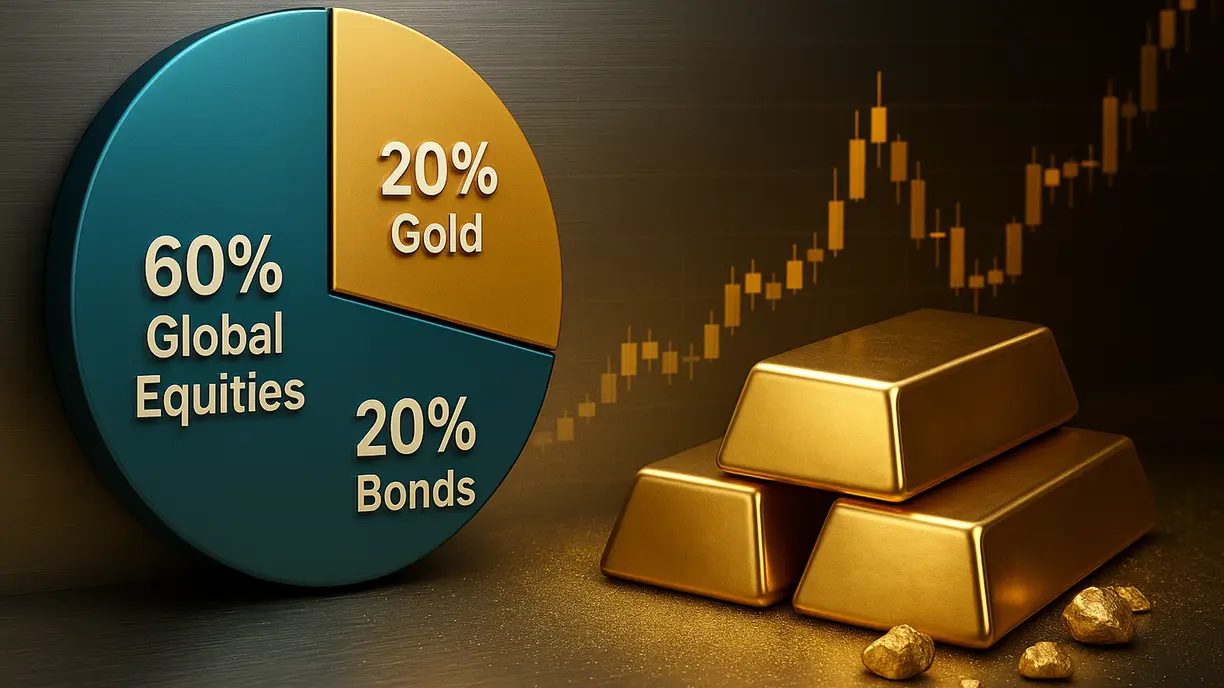

They argued that in this environment, investors should consider transforming their traditional 60/40 portfolio to incorporate a 20% gold allocation. The analysts noted that over the past 15 years, a portfolio with 60% in global equities, 20% in bonds, and 20% in gold has outperformed the traditional allocation while also reducing volatility.

They observed that from 2010 to the present, a 60/20/20 portfolio has achieved an annualized return of 7.5% with volatility of 8.55%, resulting in a Sharpe ratio of 0.38. In contrast, the traditional portfolio returned 6.3% annually with volatility of 8.01%, yielding a Sharpe ratio of 0.28.

“Though gold marginally increased overall volatility, it enhanced return efficiency, making it a valuable addition to multi-asset strategies in uncertain macro environments,” the analysts wrote.

“Exposure to gold in a multi-asset portfolio can enhance risk-adjusted returns, particularly in macro environments where the classic bond-equity hedge is less reliable,” they added. “In the multi-asset space—where macroeconomic uncertainty, deglobalization, and liquidity shifts increasingly challenge asset allocators—gold offers an alternative hedge, making it a proactive tool for navigating risk and capturing value across diverse regimes.”

While some investors may be hesitant to jump into gold as prices climb back above $3,300 an ounce, the report notes that, compared to other periods of major financial distress, gold still has considerable upside potential.

Baronyan and Nae highlighted three other significant periods of economic turmoil. They noted that during the inflation crisis between 1972 and 1976, gold prices surged over 300%; from 1977 to 1982, when gold reached its all-time inflation-adjusted highs, prices peaked at 261%; and during the Great Financial Crisis from 2007 to 2015, gold prices peaked at 154%. Although prices corrected from their highs, the analysts said they remained significantly above pre-crisis levels.

Looking at recent price action, Baronyan and Nae noted that since 2020, gold prices at last month’s peak were up 90%, without experiencing a major correction.

The analysts said that while economic uncertainty and inflation continue to support investment demand for gold, central bank interest remains a key factor in the current rally.

“While motivations differ across regions, the underlying strategy is consistent: central banks may be preparing for a world of greater geopolitical and monetary fragmentation, where gold functions as a neutral, tariff-resistant reserve asset,” they stated. “Whether to hedge against external shocks or maintain domestic monetary stability, gold’s role in reserve portfolios has increased.”

Central banks have increased their gold reserves by more than 1,000 tonnes in each of the last three years. Data from the World Gold Council shows that central banks continue to buy, albeit at a slightly slower pace, purchasing 243.7 tonnes of gold between January and March.

Data from FTSE Russell shows that although central bank gold holdings as a percentage of total foreign reserves have risen in the past five years—from 9% to 13.5%—they are still significantly below long-term averages.

“Since 2022, central bank accumulation has emerged as a dominant theme, driven by shifting reserve strategies, geopolitical fragmentation, and a desire to reduce reliance on dollar-denominated assets. These actions signal a growing preference for neutral, non-sovereign collateral within global reserve portfolios,” the analysts said.

“As an investment asset, gold behaves distinctly. Its low correlation to equities, bonds, and commodities makes it a compelling portfolio hedge—particularly when traditional assets falter simultaneously. However, its value is not static. Gold tends to attract capital during periods of financial stress—whether inflationary or deflationary—and experiences partial reversals as market confidence returns. This tactical behavior distinguishes gold from buy-and-hold growth assets: its utility lies in flexible allocation during shocks, rather than permanent exposure,” they concluded.