(Kitco News) – Gold is an excellent source of diversification and optionality, but its volatility, lack of yield, and inconsistency even as an inflation hedge mean investors shouldn’t put all their eggs in the yellow metal’s basket, according to Aaron Hussein, global market strategist at JP Morgan Asset Management.

Hussein said it’s no surprise that gold is getting a lot of attention these days, as the price has nearly doubled since 2022, which has driven many new investors to the precious metal.

“Several factors have contributed to this renewed demand,” he said. “Heightened geopolitical risks, including tensions in the Middle East and Russia’s invasion of Ukraine, have revived interest in gold as a safe-haven asset. At the same time, growing fiscal concerns in the US and speculation around the long-term future of the US dollar have added fuel to the fire. Central banks in emerging markets have responded by steadily increasing their gold reserves, adding to the momentum.”

Hussein said that under these circumstances, investors are revisiting the role of gold in their portfolios. “But before rushing to chase the rally, it’s worth stepping back and asking a more fundamental question: what are gold’s actual characteristics and do they justify a more strategic allocation?”

He then offers several key characteristics for investors to consider before jumping into the gold market.

“First, gold’s long-term performance depends heavily on timing,” he said. “Over the past three and a half decades, gold was the worst-performing major asset class both in absolute terms and on a risk-adjusted basis. It lagged stocks, real estate and timberland, and delivered similar returns to bonds, but with three times the volatility.”

But when the start date is moved forward by 10 years, gold becomes the best investment. “Over the past two and a half decades, it was the best-performing asset class in absolute terms outperforming stocks, bonds, and other real assets such as real estate and timberland,” Hussein noted.

The second factor to consider is that gold is highly volatile while also enduring long periods of stagnation. “The reason for this variability lies in the nature of gold itself,” he said. “It doesn’t produce income or earnings, so its value is driven almost entirely by sentiment around inflation, macro stress, and the credibility of fiat currencies.”

Hussein said that while these narratives can be powerful, they are also “cyclical, unpredictable, and prone to reversals,” as the period after 1980 shows.

“After hitting an inflation-fuelled high, gold fell in real terms for two decades and didn’t reclaim its 1980 peak (adjusted for inflation) until February 2025,” he noted. “That’s a 45-year drawdown in real terms.”

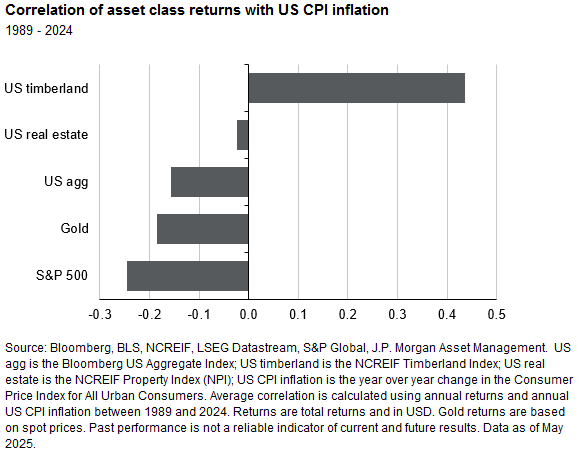

The third consideration is that gold-as-inflation-hedge isn’t always true. “Gold is often seen as a hedge against inflation and it performed well in the 1970s,” Hussein said. “But over the past four decades, the relationship has been far weaker. On average, gold’s correlation with US inflation has been negative, not positive.”

“Even during the inflation spike of 2020–2022, gold prices declined — making it one of the worst-performing major asset class over that two-year stretch,” he added. “While gold may act as a hedge against inflation in specific regimes, it is far from reliable in doing so.”

The fourth key factor to consider is that the yellow metal generates no income. “This may seem obvious, but in an environment where investors can now earn 4-5% from bonds and core real assets, the opportunity cost of holding gold is real,” Hussein said. “It produces no income, and unlike productive assets, there is no underlying cashflow to grow over time. Any return depends entirely on changes in price, which rely heavily on sentiment rather than fundamentals.”

“In contrast, core real assets have delivered remarkably stable returns over the past three decades, with income often accounting for more than two-thirds of total return,” he added. “That stability not only helps to lower overall portfolio volatility but also provides investors with a regular income stream.”

Hussein acknowledges that in the current macroeconomic and geopolitical environment, gold clearly has a role to play. “As a hedge against geopolitical shocks, deglobalisation, and weakening trust in fiat currencies, a modest allocation can offer diversification and optionality,” he said. “And given the recent rally, many investors may regret not having owned more.”

“But gold is not a panacea,” he warned. “It’s volatile, generates no income, has a patchy track record as an inflation hedge, and has endured long periods of stagnation. Other core real assets, such as infrastructure, real estate, and timberland, share many of gold’s defensive attributes while also offering greater stability and a steady stream of income.”

For these reasons, Hussein believes that gold should not be treated as “a silver bullet but as a source of diversification and optionality within a wider real assets strategy.”

“On its own, it may be unreliable, but when paired with income-generating, lower-volatility assets like infrastructure or real estate, it can strengthen portfolios for a range of market regimes,” he concluded. “In a world of heightened uncertainty, owning some gold makes sense. Relying on gold as your only diversifier does not.”