(Kitco News) – Gold prices could rise to the edge of $4,000 per ounce by year-end – or they could finish with single-digit annual gains – depending on how geopolitical and macroeconomic risks ultimately impact the yellow metal’s key drivers, according to the World Gold Council (WGC).

“Gold has continued its record-setting pace, rising 26% in US dollar terms in the first half of 2025 – and reaching double-digit returns across currencies,” WGC analysts wrote in their Gold Mid-Year Outlook 2025. “A combination of a weaker US dollar, rangebound rates and a highly uncertain geoeconomic environment has resulted in strong investment demand.”

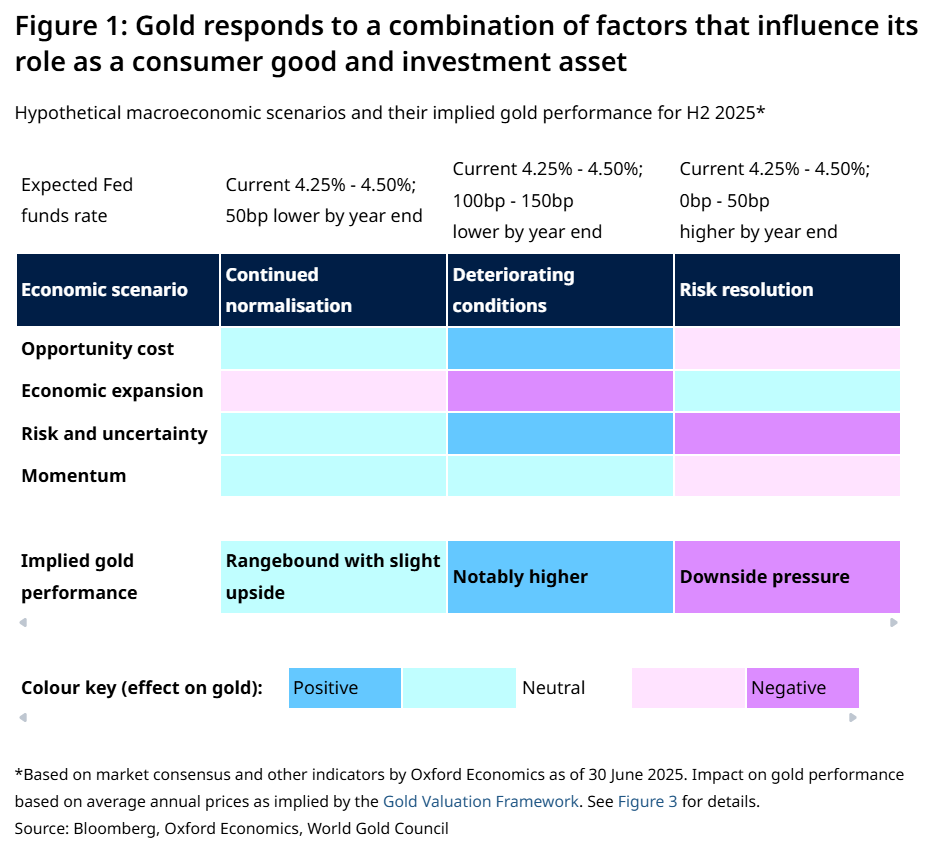

The analysts said that a recurring question from these investors is “whether gold has reached a peak or has enough fuel to push higher.” Using their Gold Valuation Framework, the WGC analyzed what current market expectations indicate for gold’s performance in H2 2025, along with the various drivers that could push gold higher or lower.

“If economists and market participants are correct in their macro predictions, our analysis suggests that gold may move sideways with some possible upside – increasing an additional 0%-5% in the second half,” they wrote. “However, the economy rarely performs according to consensus. Should economic and financial conditions deteriorate, exacerbating stagflationary pressures and geoeconomic tensions, safe haven demand could significantly increase pushing gold 10%-15% higher from here. On the flipside, widespread and sustained conflict resolution – something that appears unlikely in the current environment – would see gold give back 12%-17% of this year’s gains.”

The WGC noted that gold’s performance so far in 2025 year is one for the record books.

“Gold closed out the first half of the year as one of the top-performing major asset classes, rising nearly 26% over the period,” they noted. “It recorded 26 new all-time highs (ATHs) in H1 2025, having broken through 40 new ATHs in 2024.”

The analysts said this outperformance was the result of a combination of factors, including a weaker US dollar, rangebound yields in anticipation of future rate cuts, and “heightened geopolitical tensions – some of these directly or indirectly linked to US trade policy.”

“Stronger demand also came from increased trading activity across OTC markets, exchanges, and ETFs,” they said. “This lifted average gold trading volumes to US$329bn per day during H1 – the highest semi-annual figure on record. Central banks also contributed with continued buying at a robust pace – even if not at the record levels of previous quarters.”

The WGC noted that “one of the most significant macro themes so far this year has been the underperformance of the US dollar, which had its worst start to a year since 1973. This was also seen through the underperformance of US Treasuries, which, for more than a century, had been the epitome of safety. Yet, inflows into Treasuries faltered in April amid heightened uncertainty.”

“Conversely, gold ETF demand was particularly strong in the first half of the year, led by notable inflows from all regions,” they said. “By the end of H1 the combination of a surging gold price and investor flight to safety pushed global gold ETF’s total AUM 41% higher to US$383bn. Total holdings rose by an impressive 397t (equivalent to US$38bn) to 3,616t – the highest month-end level since August 2022.”

“Trade-related and other geopolitical risks played a large role, not just directly, but by fuelling moves in the dollar, interest rates, and broader market volatility - all of which fed into gold’s appeal as a safe haven,” they added. “Taken together, these factors have contributed around 16% to gold’s return over the past six months.”

Using their Gold Return Attribution Model (GRAM), the analysts broke down the impacts as follows:

Risk and uncertainty – as a trigger for flows from investors looking for effective hedges: 4% (half of which was explained by an increase in the Geopolitical Risk (GPR) Index)

Opportunity cost – making gold more attractive relative to the US dollar and bond yields: 7% (with the bulk or about 6% linked to dollar weakness)

Momentum – which can boost trends or, equally, mean-revert them: 5% (mostly connected to positive gold ETF flows).

The WGC analysts then outlined the different potential scenarios they see for H2 2025.

“The second half of the year sits on a seesaw, with geoeconomic uncertainty keeping investors on edge,” they said. “Inflation data have shown signs of improvement, but concerns remain that conditions could deteriorate quickly. Dollar-related pressures are likely to persist, and questions around the end of US exceptionalism may dominate investor discussions. Overall, these conditions position gold as a net beneficiary – but while the fundamentals remain strong, the gold price has already captured part of these dynamics. In turn, sustainable conflict resolution and continued rising stock prices could lure more risk on flows and limit gold’s appeal.”

The WGC analyzed the potential impacts of these various conditions through the lens of gold’s four key drivers – “economic expansion, risk and uncertainty, opportunity cost, and momentum – across three scenarios.”

The consensus expectation is one of continued normalization in the gold market.

“Market consensus suggests global GDP will move sideways and remain below trend in the second half,” they wrote. “World inflation is likely to rise above 5% in H2 as the global impact of tariffs becomes more pronounced – with the market expecting US CPI to reach 2.9%. In response to this mixed economic backdrop, central banks are expected to begin cautiously lowering interest rates towards the end of Q4, with the Fed expected to cut rates by 50bps by the end of the year.”

The analysts said that while some progress in trade negotiations is expected, the environment is likely to remain volatile for the remainder of the year. “Overall, geopolitical tensions – particularly between the US and China – are likely to remain elevated, contributing to a generally uncertain market environment.”

“Our analysis, based on our Gold Valuation Framework, suggests that, under current consensus expectations for key macro variables, gold could remain rangebound in H2, closing roughly 0%–5% higher than current levels, equivalent to a 25%–30% annual return,” they said. “Technical indicators suggest that gold’s consolidation phase over the past few months is a healthy pause in a broader uptrend, helping to ease previous overbought conditions and potentially setting the stage for renewed upside.”

“Falling interest rates and continued uncertainty would maintain investor appetite, particularly via gold ETFs and OTC transactions,” they added. “At the same time, central bank demand is likely to remain robust in 2025, moderating from its previous records while staying well above the pre-2022 average of 500-600t.”

High gold prices will likely continue to curb consumer demand and potentially encourage recycling, however, which “would act as a damper to stronger gold performance.”

The WGC’s bull case for gold would rely on deteriorating economic and market conditions.

“This could be either a more severe stagflationary environment – marked by slower growth, falling consumer confidence and persistent inflationary pressure from tariffs – or an outright recession, characterised by widespread flight-to-quality flows,” they said. “Gold would benefit from lower interest rates and dollar weakness given growing concerns around US economic leadership and policy uncertainty. In this context, central banks could further accelerate their diversification of foreign reserves away from the dollar.”

The projected impact of this bull case “shows that gold would perform strongly in such an environment, potentially rising an additional 10%–15% in H2 and closing the year almost 40% higher,” they said. “As we have seen historically during periods of heightened risk, investment demand would significantly outweigh any deceleration in consumer demand and rise in recycling. And while flows into gold ETFs in the first half of the year have already been substantial, total holdings at 3,616t remain well below the 2020 peak of 3,925t. Further, gold ETFs have accumulated less than 400t in the past six months and just over 500t in the past twelve. In contrast, gold ETFs have amassed between 700t and 1,100t in previous bull runs.”

The analysts also pointed out that COMEX futures net long positions are currently around 600t, whereas they rose above 1,200t in previous crises. “This all suggests meaningful room for further accumulation should conditions deteriorate,” they said.

The bear case for gold which the WGC envisages relies upon resolution of the major current geopolitical and economic risks.

“Sustainable geopolitical and geoeconomic conflict resolution would reduce the need to keep hedges, such as gold, part of investment strategies – encouraging investors, in turn, to take on more risk,” they noted. “A full resolution of risk does not seem as likely given what we’ve seen over the past six months. But more encouraging economic growth prospects, even if inflationary pressures were to persist, would push US Treasury yields higher, leading to a steepening of the yield curve. And if inflation stabilised further, the effect on rates would be more substantial.”

The bear case impact could see gold give back 50% or more of its annual gains, the WGC said.

“In this scenario, our analysis suggests that gold could retreat by 12%–17% in H2, finishing the year with positive but low double-digit (or even single-digit) returns,” they wrote. “This pullback is equivalent to the trade risk premium that partly explains gold’s H1 performance. The reduction in risk, combined with an increase in opportunity cost – through rising yields and a stronger dollar – would trigger gold ETF outflows and reduce overall investment demand. We could also see a deceleration in central bank demand if US Treasuries are again favoured.”

“Gold market technical analysis and speculative positioning suggest that US$3,000/oz would be a natural ‘support level’, prompting opportunistic investment buying,” they added. “If gold were to break through these levels, disinvestment may accelerate. That said, lower gold prices would attract more price-sensitive consumers and discourage recycling, limiting gold’s downside compared to what may otherwise be implied by simply looking at real rates and the US dollar.”

The World Gold Council concluded by noting that the yellow metal’s “exceptionally strong” first half came on the back of “a weaker US dollar, persistent geopolitical risk, robust investor demand and continued central bank purchases.” And while some of these drivers are likely to continue through H2, “the path forward remains highly dependent on multiple factors including trade tensions, inflation dynamics, and monetary policy.”

“Consensus expectations suggest a relatively steady finish for gold with moderate upside potential if macro conditions hold. Gold could also be partly supported by contributions from new institutional investors such as Chinese insurance companies,” the analysts said. “A more volatile geopolitical and geoeconomic scenario could push gold significantly higher, particularly if more substantial stagflation or recession risks materialise and investor appetite for safe haven assets grows. On the flip side, while seemingly unlikely given the current environment – widespread and sustained global trade normalisation would bring higher yields and resurgent risk appetite, challenging gold’s momentum. Gold could also be tested by a visible deceleration in central bank demand beyond current expectations.”

Taken together, the WGC said that they “believe that gold – through its fundamentals – remains well-positioned to support tactical and strategic investment decisions in the current macro landscape.