(Kitco News) – China’s gold market was tepid in June, but its first half performance was still very strong overall with the Shanghai Benchmark Gold Price and ETF inflows both setting semiannual records, according to Ray Jia, Research Head, China at the World Gold Council (WGC).

“Gold prices saw limited moves in June,” Jia noted. “The LBMA Gold Price PM in USD climbed 0.3% while the SHAUPM in RMB fell mildly by 0.7% – due mainly to a stronger local currency against the dollar. Nonetheless, the LBMA Gold Price in USD and the SHAUPM in RMB concluded H1 with their strongest performances since 2016, surging 23% and 21% respectively.”

“Based on our Gold Return Attribution Model, geopolitical risks and a weaker dollar were notable contributors to the gold price strength,” he said. “Meanwhile, we believe continued central bank purchases further aided gold.”

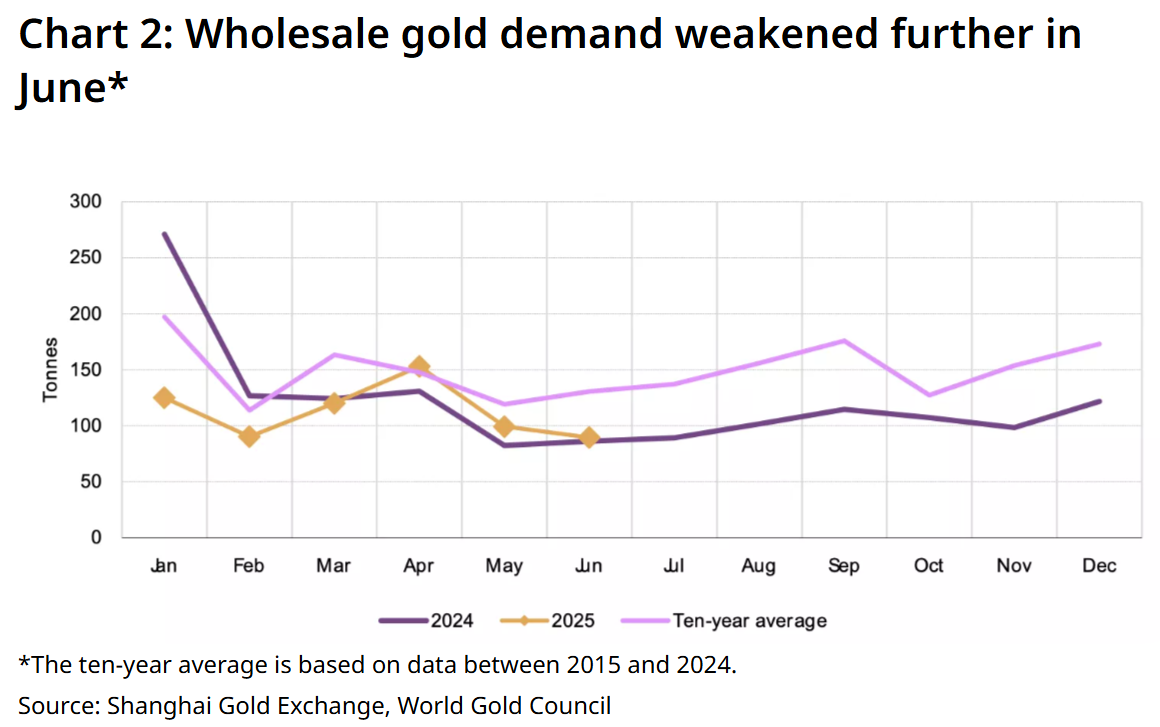

Wholesale demand, on the other hand, remained weak last month. “Jewellery manufacturers, commercial banks and other market participants withdrew 90t during the month, 10% lower m/m,” Jia said. “And while there was a mild 4% rise compared to a weak June in 2024, the month’s wholesale gold demand stayed well below its 10-year average. Seasonal weakness, still tepid consumer confidence and the elevated gold price continued to pressure gold jewellery consumption, leading to a cautious stance from retailers on restocking. Added to this was June’s cooling momentum in bar and coin investment as investors sat on the sidelines amid the range-bound gold price movement.”

Gold withdrawals from the SGE totaled 678 tonnes during the first half of 2025, an 18% year-over-year decline and 22% below the ten-year average. “Jewellery demand has weakened amid the surging gold price, cautious consumer spending, and the industry’s continued consolidation,” he said. “But [the jewelry] sector’s weakness was partially offset by investment strength: the gold price rally, rising safe-haven demand – amid spiking US-China trade tensions particularly in April – and tepid performances of other domestic assets supported bar and coin sales.”

ETF demand, on the other hand, recovered last month to conclude the strongest first half on record. “Chinese gold ETF flows turned positive in June, attracting RMB1bn (US$137mn),” Jia wrote. “With the US-China trade tensions easing and the RMB strengthening, safe-haven demand for gold cooled, resulting in limited changes in ETF flows.”

Chinese gold ETFs added $8.8 billion during H1 2025. “Inflows were driven by similar factors, supported bar and coin sales noted above,” he said. “Chinese gold ETFs’ total AUM surged 116% during the first half, reaching RMB153bn (US$21bn) by the end of June. Meanwhile, collective holdings jumped 74% to 200t.”

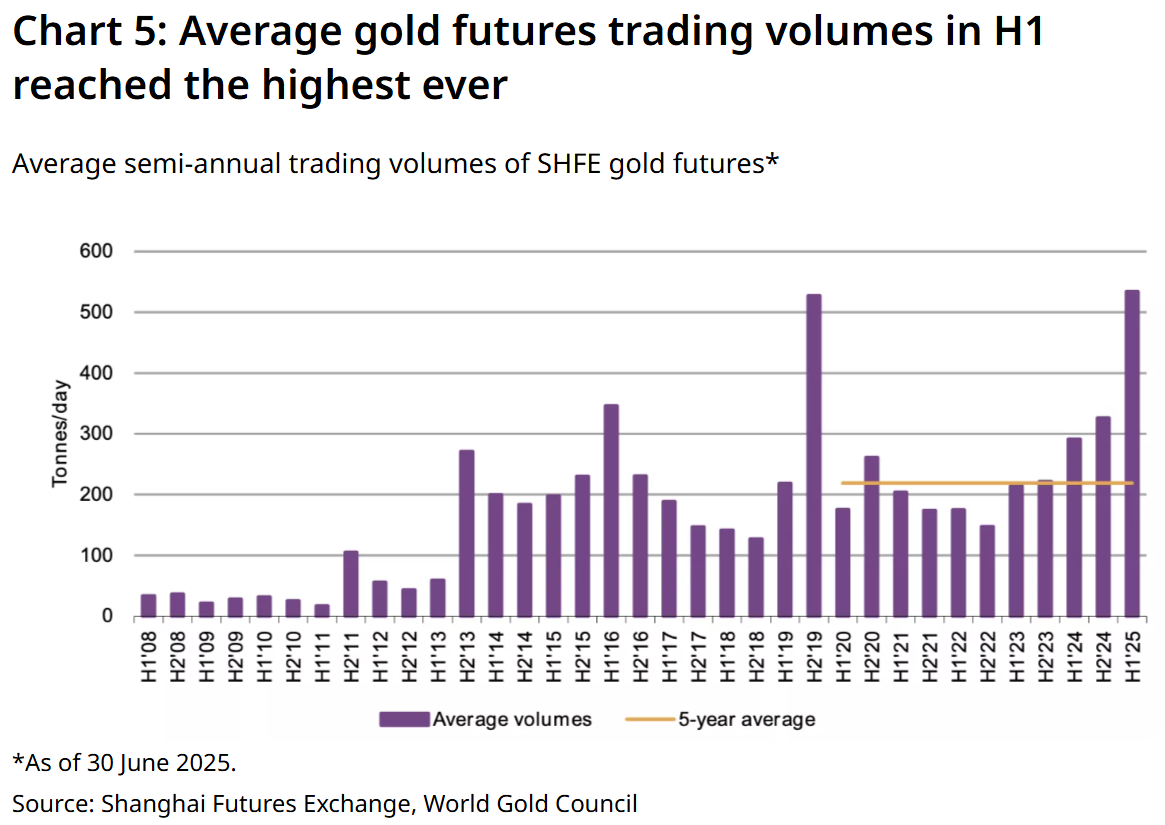

And while SHFE futures trading activity fell 39% month-over-month to 380 tonnes per day in June amid consolidating prices and low volatility, futures trading volumes averaged 534 tonnes per day during the first half, the highest semi-annual performance on record.

The People’s Bank of China also continued its streak of official bullion purchases last month. “The PBoC reported a 2t gold purchase in June, the eighth consecutive monthly increase,” Jia noted. “China’s official gold holdings now stand at 2,299t. China has announced non-stop gold purchases – of varying amounts – during the first half of 2025, totalling 19t. During this period, gold’s share of China’s total foreign exchange reserves rose from 5.5% in December 2024 to 6.7% at the end of June.”

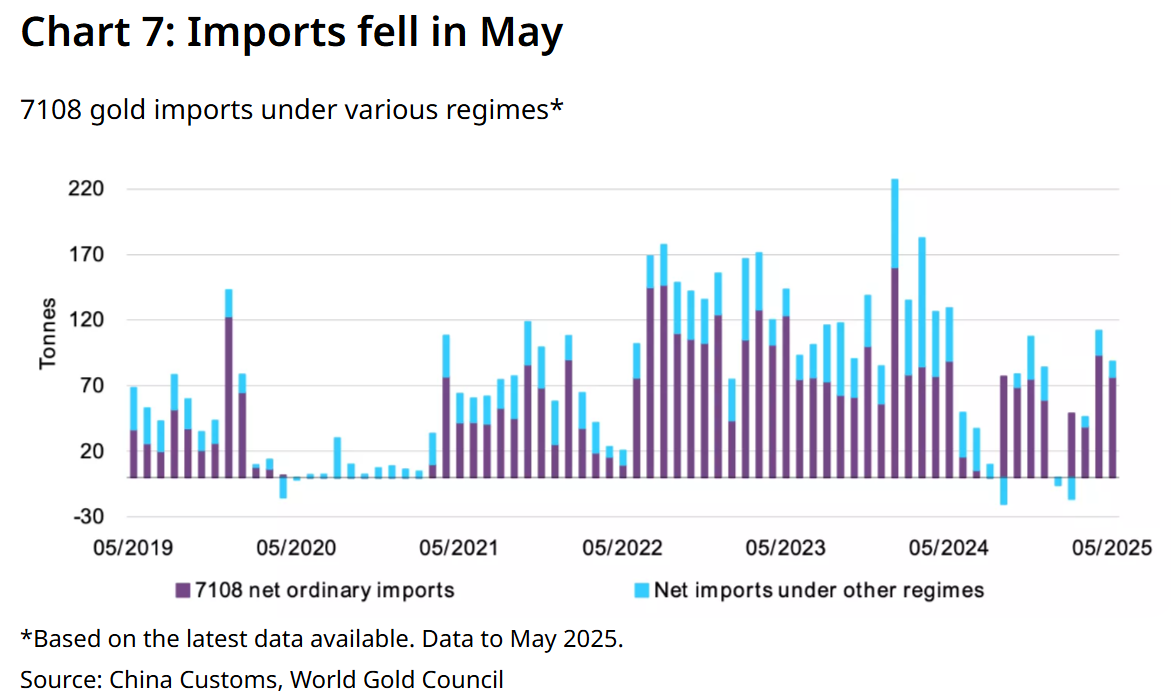

Meanwhile, imports fell once again in May, the most recent period for which data is available. “China imported 89t of gold in May on a net basis, according to the latest data from China Customs, down 21% m/m and 31% y/y,” he said. “Basically, this reflects wholesale demand trends in the month: gold withdrawals from the SGE in May saw a sizable m/m fall. In general, weakening gold jewellery demand so far this year has weighed heavily on imports.”

Looking ahead, Jia warned that “[t]epid consumer confidence and industry consolidation may continue to weigh on gold jewellery demand,” but investment demand for bullion has the potential to remain strong in the second half of 2025.