(Kitco News) – China’s gold market reflected the relative price stability seen in July, with ETFs seeing outflows and futures continuing to cool, while imports concluded their weakest H1 since 2021, according to Ray Jia, Research Head, China at the World Gold Council (WGC).

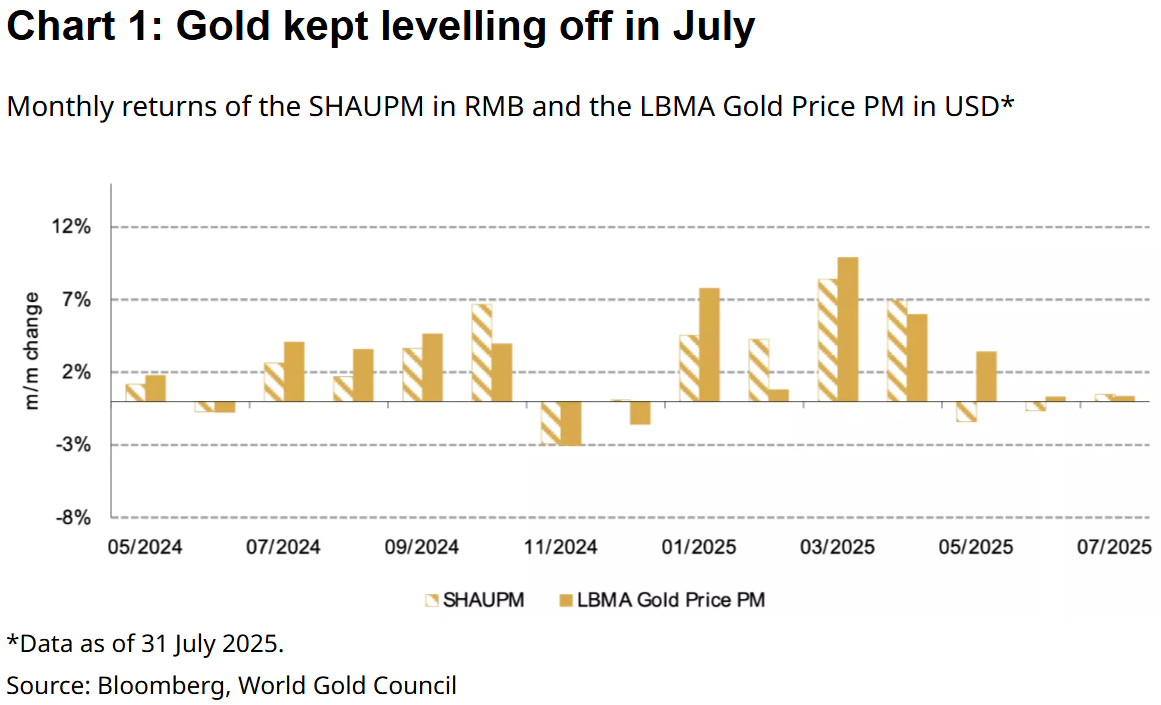

Jia noted that gold prices rose only modestly in July.

“Rising inflationary concerns and various other risks outweighed a stronger dollar, leading to a mild rise in gold prices: the LBMA Gold Price PM in USD was 0.3% higher m/m while the SHAUPM in RMB climbed 0.5%–due mainly to a weaker local currency against the dollar,” he said. “And y-t-d, the RMB gold price has surged by over 22%, outperforming most local assets.”

Wholesale demand also saw a minor increase on the back of seasonal factors.

“Gold withdrawals from the SGE totalled 93t in July, a modest m/m rise of 3t and a slight increase of 4t y/y,” Jia wrote. “As shown in the below chart, the m/m pick up is mainly seasonal: jewellery demand tends to improve into Q3. Meanwhile, we believe better sales of gold bullion – as physical gold investors took advantage of the current price stability – also contributed to wholesale gold demand’s rebound in July.”

He cautioned, however, that July’s data was well below the 10-year average, which highlights this year’s weak overall wholesale demand, particularly in the jewellery sector.

“As we noted in our Q2 Gold Demand Trends, the divergence in China’s gold demand has continued amid the unprecedented level of the local gold price: while investment demand for gold kept surging, jewellery consumption – in tonnage terms – fell off a cliff, weighing on gold jewellers’ restocking activities – a major part of SGE withdrawals,” he said.

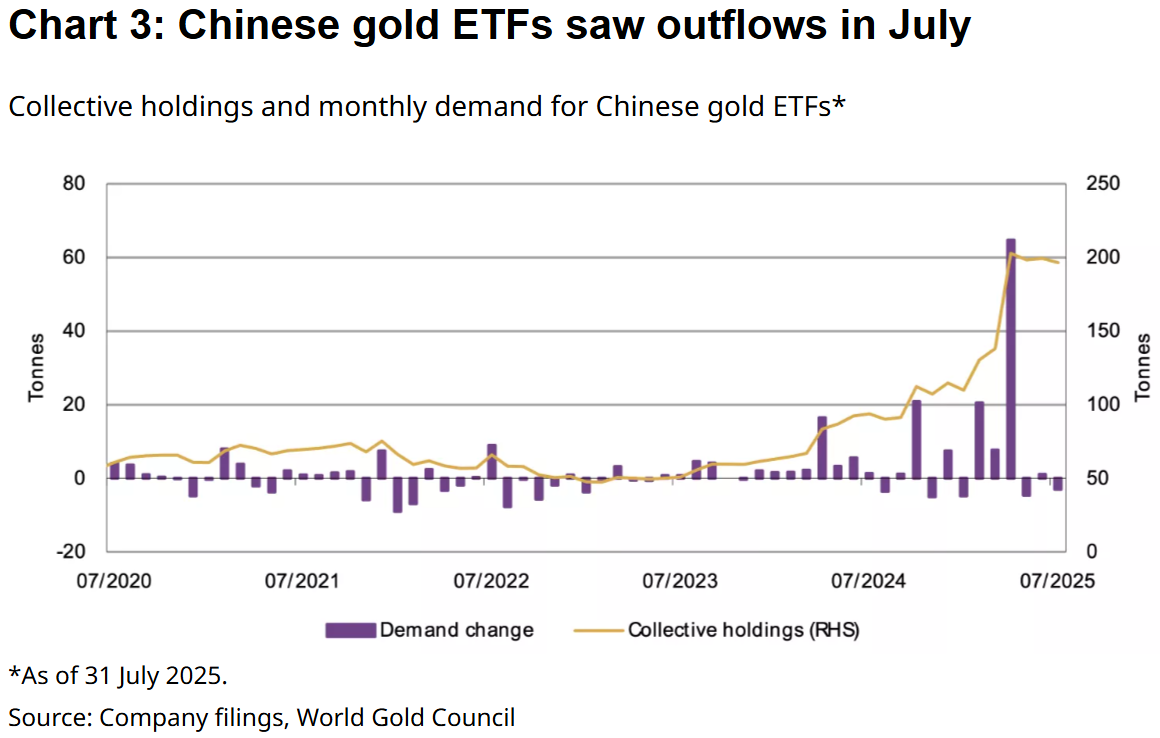

Meanwhile, Chinese ETF flows turned negative once again.

“Chinese gold ETFs saw outflows of RMB2.4bn (US$325mn) in July,” Jia said. “Due to these outflows and a flat gold price, their total AUM declined slightly by 1% to RMB151bn (US$21bn). And collective holdings reduced by 3t to 197t.”

“Despite the July loss, Chinese gold ETFs’ y-t-d inflows remained at a record high of RMB61bn (US$8.5bn, 82t),” he wrote.

Jia pointed out that China’s Q2 GDP exceeded expectations and helped boost risk appetite, “which is reflected in the strongest monthly performance of the CSI300 stock index” since September 2024.

“Meanwhile, local government bond yields kept rebounding amid the economic resilience and investors’ cooling expectations of further rate cuts from the People’s Bank of China (PBoC),” he said. “These factors, combined with the lack of a clear trend in the local gold price, dimmed Chinese investors’ interest in gold ETFs during the month.”

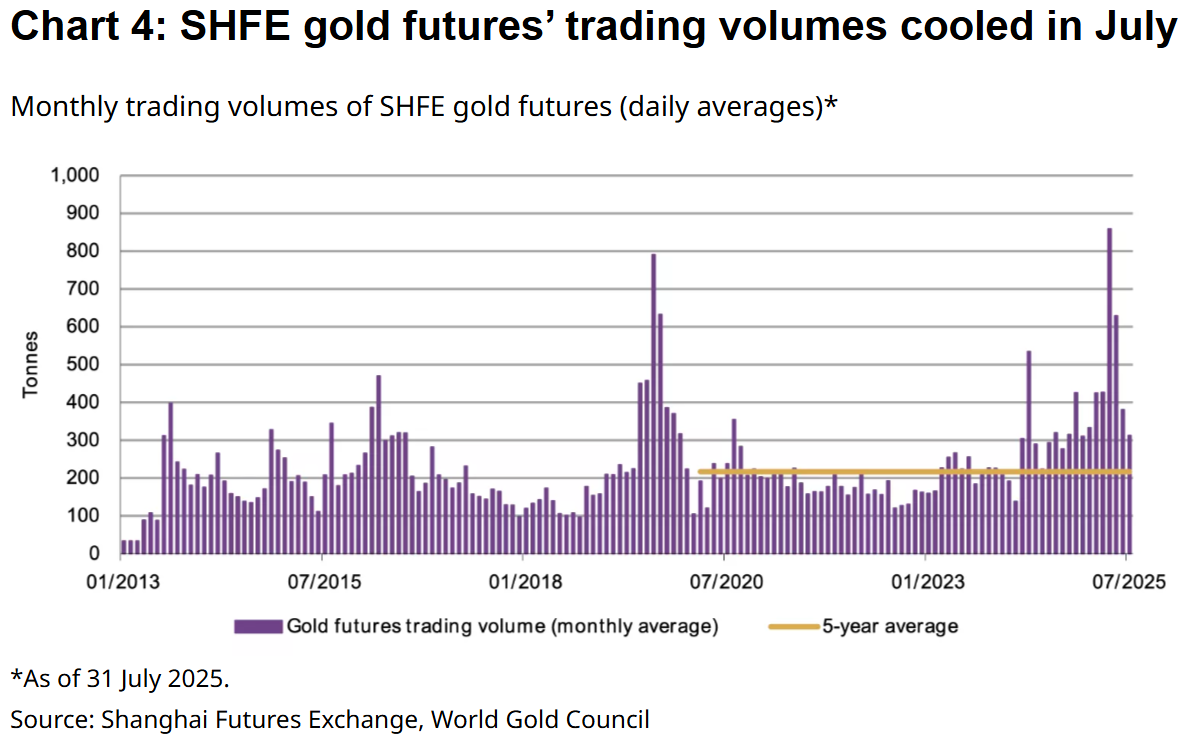

Turning to futures markets, Jia noted that trading volumes at the SHFE averaged 242 tonnes per day, a decline of 18% month over month but still above the five-year average of 216 tonnes per day.

“We believe this drop is mainly related to the range-bound gold price performance and a declining price volatility during the month, which lowered traders’ interest,” he wrote.

And the central bank’s recent buying streak continued last month.

“The PBoC announced another gold purchase in July, amounting to 2t, the ninth consecutive monthly addition,” Jia said. “Following non-stop purchases during the past nine months, China’s official gold holdings now reached 2,300t, 6.8% of the total reserve.”

The country has increased its gold holdings by 21 tonnes so far in 2025.

Import data for June - the most recent month for which numbers are available - confirmed that imports were historically weak during the first half of the year.

“China’s gold imports almost halved in June, totalling 50t, 45% lower m/m,” he said. “We believe this is related to tepid wholesale gold demand in the month. And this takes the Q2 total to 250t, 18% below the 2024 level.”

During the first half, China imported a total of 323 tonnes of gold in H1 2025 - a massive year-over-year drop of 62%.

Looking ahead, Jia said WGC analysts expect “continued seasonal improvement in China’s wholesale gold demand going forward, particularly in the gold jewellery sector,” though high prices could keep volumes lower.

“Meanwhile, the momentum in bar and coin demand will depend on factors such as the gold price trend and the overall risk appetite – the recent strong equity performance may divert some attention away,” he said.