(Kitco News) – The gold bugs are back, but the yellow metal’s gains aren’t coming from its usual drivers, according to Victor Balfour, investment strategist at Rothschild & Co Wealth Management.

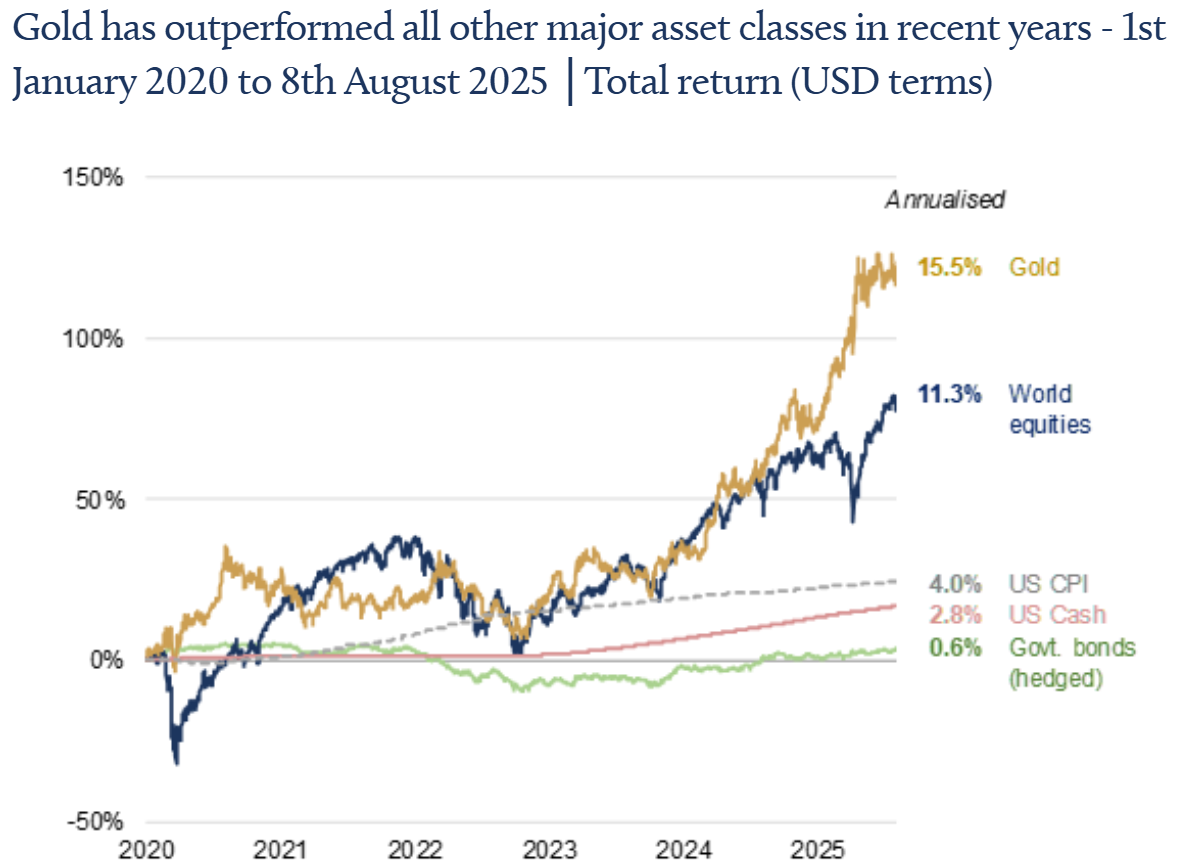

Balfour noted in an analysis published on Tuesday that gold is in the midst of another standout year. “The shiny metal is up by more than a quarter in 2025, and on track for a third consecutive year of double-digit returns – a winning streak not seen since the mid-noughties,” he said.

But Balfour said the recent climb has been neither stable nor predictable. “Gold has lost touch with its traditional drivers like real yields and the dollar, with demand shaped by the geopolitical maelstrom – including protectionism and wider conflict,” he wrote. “Yet despite ongoing attempts to reshape global trade – and even talk of a renewed gold arbitrage - prices have been flatlining for several months now.”

He said this makes it more difficult to assess gold’s role in investor portfolios.

“Clearly, gold (more so than other precious metals) has played an important investment role. Historically, it has been a long-term store of value over several millennia, lending monetary institutions their credibility (rather than vice versa) and acting as a key medium of real wealth protection,” Balfour noted. “It can also act as a financial panic button, a sort of last-resort asset at times of crisis. Amidst fears of US default (as in 2011), banking collapse (2008) or runaway inflation (1979) it has strongly outperformed securities markets.”

But despite this track record, he said gold remains impossible to value objectively. “Arguably, this is true of all assets, but the absence of a yield makes it particularly difficult for gold and other commodities: discounted cashflow analysis is correspondingly impossible,” he pointed out. “This might not matter if the real price were stable, but it isn't. Current mining costs are not a useful guide to value – supply is inelastic and most gold traded is already above ground.”

Balfour noted that high interest rates generally hurt gold demand due to its lack of a yield. “Intuitively, this reflects the opportunity cost of owning gold relative to other "risk-free" assets such as treasuries,” he wrote. “But this hasn’t often been the case in the last few years, with gold unusually rising alongside higher yields. Nor is gold’s relationship to the dollar always helpful: dollar weakness this year may explain some of gold’s ascent, but the same cannot be said of late 2024 – when all around dollar strength should have been a headwind, but gold continued to surge (relative to all major currencies).”

Balfour lists geopolitical risk and central bank buying as other more qualitative factors that have boosted the gold price. “A number of mostly emerging economies, particularly China, have been big buyers of gold in recent years as they look to ‘de-dollarise’,” he noted. “On this count, a disruptive President Trump suggests gold will remain a crucial currency diversifier ahead.”

He cautions, however, that there are two potential headwinds that should concern investors.

“First, the economic story still remains constructive: we don’t think stagflation, or a big economic downturn is likely or imminent – two scenarios that would benefit gold meaningfully,” he said. “US growth is (still) respectable and although inflation has started to edge higher, tariffs aside, it will likely remain manageable. This suggests to us that the Fed’s easing cycle is likely to be relatively short-lived from here. The current ongoing idea of rates being ‘higher for longer’ points to elevated real yields and at some stage (possibly) a rebounding dollar – which might temporarily constrain gold’s advance.”

The second risk facing the gold rally is the rise of Bitcoin and other cryptocurrencies as debasement hedges in their own right, though Balfour finds these “unconvincing.”

“Recently passed US legislation is set to further legitimatise stablecoins, which may encourage more enthusiasm for unbacked coins,” he noted. “But in the Bitcoin vs gold debate, we strongly prefer the latter: we see our role as investment advisers being not to help our clients ‘get rich quickly’ but rather to stay so.”

Balfour concluded that the strategic investment case for owning gold remains strong. “And despite its visible rise in recent years, we remain slightly overweight in a portfolio context given its role as a liquid portfolio diversifier and potential source of resilience in periods of market stress,” he said.