(Kitco News) – The yield spread at the front end of the U.S. Treasury curve has risen to its highest level in over five years, and this is contributing to the attractiveness of gold and silver as investments, according to Ole Hansen, Head of Commodity Strategy at Saxo Bank.

“The US 2–10-year Treasury spread trades around 60 basis points, approaching the steepest level on a daily close since January 2022,” he wrote on Thursday. “The move reflects a so-called ‘bull steepener,’ where short-dated yields fall on rising expectations for rate cuts, while longer-dated yields struggle follow suit amid mounting concerns about Federal Reserve independence, inflation risks, and a rising US debt pile.”

Hansen said that while the impact of this on investment metals is nuanced, it’s supportive on balance.

“For gold, lower front-end yields ease the opportunity cost of holding non-yielding assets,” he said. “This shift is particularly relevant for real asset managers, many of whom have struggled—or in some cases been restricted—from allocating to gold while US funding costs were elevated. It helps to explain why total holdings in bullion-backed ETFs—despite a central-bank-led gold rally—saw an 800-ton decline between 2022 and 2024, a period when US funding rates and real yields surged as the Federal Reserve stepped up its battle against inflation.”

“Together with a general supportive backdrop for bullion and traders now bringing forward additional rate cut expectations, the prospect of lower funding costs is once again underpinning demand for gold, especially via ETFs,” he added.

On the other side of the equation, Hansen noted that “10-year yields have not reflected the prospect of incoming rate cuts, instead holding above support near 4.2% and complicating an otherwise bullion-supportive backdrop.”

“Much of the nominal yield is explained by inflation breakevens, currently around 2.45%, while the balance—the real yield—signals that investors are demanding greater compensation for fiscal risks and potential political interference with monetary policy,” he said. “This environment typically supports gold as both an inflation hedge and a safeguard against policy credibility concerns.”

Hansen pointed out that silver, with its dual role as both a monetary and industrial metal, also tends to benefit in these situations, especially if inflation concerns drive increased demand for hard assets.

“Historically, the correlation between real yields and gold prices has been strongly negative, as real yields—adjusted for inflation to reflect the true return—have tended to move opposite to gold,” he noted. “Since 2022, however, this relationship has been challenged, with periods where both rose in tandem.”

“Four key factors explain this divergence,” he wrote. “[E]levated geopolitical risks, global economic uncertainty, fiscal concerns, and record central-bank demand aimed at hedging the first three while reducing dollar dependency.”

Because of this, Hansen said that rising long-end yields – and even higher real yields – can still be supportive for gold prices if fears about Fed independence and soaring debt levels are what’s driving them.

“These factors reduce the ability of long-dated Treasuries to act as a safe haven, thereby increasing gold’s attractiveness as an alternative hedge,” he said. “The net effect of the current curve dynamics is broadly positive for investment metals. Rate-cut expectations at the short end create a tailwind, while long-end term premium linked to inflation worries and financial stability concerns strengthens the hedge argument.”

“However, while the negative correlation between gold and real yields has faded, investors should still monitor real 10-year yields closely and assess the drivers behind their prevailing levels and direction,” Hansen cautioned.

Gold continues to build on its early gains on Thursday, with spot gold last trading at $3,416.59 per ounce for a gain of 0.56% on the session.

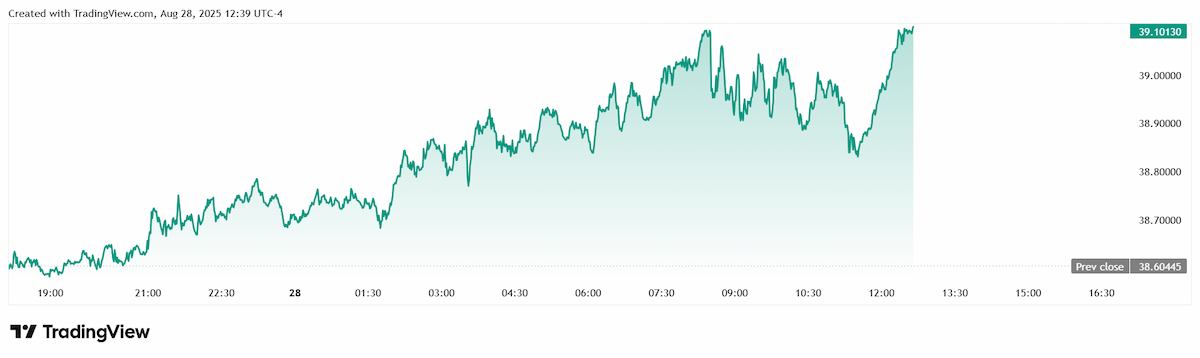

Meanwhile, silver has performed better still, with spot silver holding above $39 per ounce and last trading at $39.100 for a 1.28% gain on the daily chart.