(Kitco News) – The resumption of the Fed’s cutting cycle means all systems are a go for risk assets, but gold and silver should outperform even a hot equity market in a lower-rates environment, according to Sameer Samana, head of Global Equities and Real Assets at Wells Fargo Investment Institute.

In a Thursday interview with Kitco News, Samana was emphatic that – with one key exception – most assets should deliver a very strong performance over the next 12 months.

“I think what's really interesting is just how good the environment is for all risk assets, across the board,” Samana said. “Rarely have you had a Fed start to actively consider cutting rates when inflation has been this far above their target of 2% – running at 3% and bottoming out – and they're talking about cutting rates.”

“Clearly their focus is shifting from inflation to the labor market,” he added. “For high-quality risk assets, I think it means game on.”

Samana said this renewed investor appetite is being reflected in the equity markets – and also in gold prices. “It's becoming harder and harder to make a bear case for really anything other than bonds, given this pivot by the Fed.”

And even with Wells Fargo projecting that the labor market will continue to weaken and economic growth is expected to slow through early 2026, he believes the market has already discounted the poor performance, and equities will see a smaller secondary pullback at the worst.

“The market tends to run ahead of the economy, and the fact that we had a pretty big drawdown in Q1, almost a bear market, already accounts for some of the negative impacts of trade and tariffs, which is why we'll see the soft patch in Q4 and into the first part of ’26,” he said. “I would argue five to seven percent, maybe 10%, but nothing like we saw in the first half.”

“[Equities] will probably find their footing somewhere in that seasonally strong fourth quarter period, whereas the economy might not find its footing until the first quarter, maybe the second quarter of 2026.”

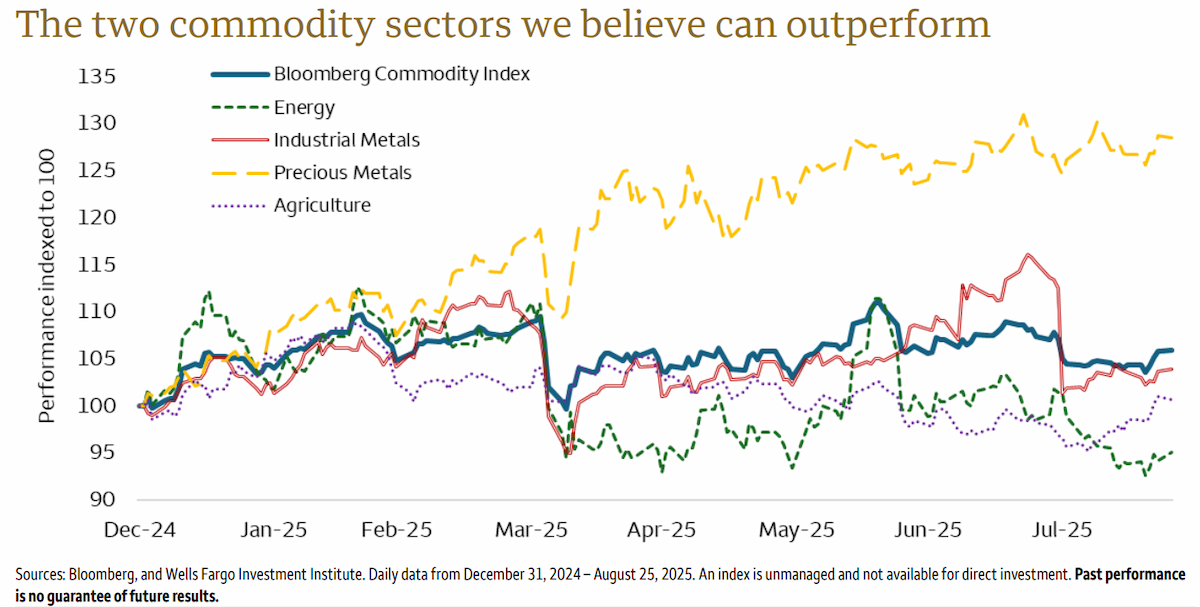

And while Wells Fargo forecasts equities to do very well through 2025 and next year, the investment bank’s chart of the week showcases the two commodity sectors expected to outperform stocks over the same timeframe: precious and industrial metals.

Samana said the case for gold is structural.

“If the Fed's going to start cutting interest rates and focus on the labor market with inflation at 3%, they're basically throwing bondholders under the bus,” he said. “Bonds are going to be under pressure, and they're not going to be the typical diversifiers, because they struggle to be good diversifiers in a high-inflation environment. Then people need to look elsewhere for diversification, and gold seems to be the easiest alternative, because it does well in uncertain times. For individuals, I think it's a diversification aspect that historically tended to be more tied to bonds.”

“Then on the central bank side, on the institutional side, there's the ‘diversification away from the dollar’ aspect, where obviously the new administration is doing things very differently than the previous administration – although you could argue that gold purchases started in earnest somewhere around 2022 with the Russia sanctions around Ukraine,” Samana said. “So it's just a continuation of that, where central bankers around the world are rethinking how much money they want tied up in U.S. dollar assets.”

“And two, if all these countries are going to be thinking about their economies first and fiscal discipline second, it's probably going to be very inflationary.”

Silver is set to be another major beneficiary of the low-rate, risk-on environment. The gray metal has been trading comfortably above $40 an ounce, and may have played a significant part in driving gold to fresh all-time highs. But it's also very much an industrial metal, and with the economic recovery expected only in the second half of 2026, investors banking on silver’s historical tendency to overshoot gold coming out of a slowdown need to be aware of the timing.

Samana said it’s likely silver could weaken in the near term as economic activity falters, but he sees no reason to doubt its potential as industrial activity ramps up afterwards.

“If I look at the gold:silver ratio, they're both pretty close to the three-year average right now,” he said. “I'll give you a three-month outlook and then a 12-month outlook.”

“I think on a three-month basis, it wouldn’t surprise me if silver underperformed again, given this soft patch that we see that markets will have to contend with,” Samana said. “But over the next 12 months, I could see silver outperforming by a little bit. If gold, let's say, is up mid-single-digits, it wouldn’t surprise me if silver's coming in close to high-single-digits.”