(Kitco News) - Gold’s rally has entered a cooling phase after two consecutive weekly losses, but while near-term momentum has stalled, the fundamental case for holding gold remains intact, according to Ole Hansen, head of commodity strategy at Saxo Bank.

Hansen said that over the past two weeks, the tone “has shifted from exuberance to reflection, with traders reassessing how much of the 2025 narrative—rate cuts, fiscal stress, geopolitical hedging, and central bank demand—has already been priced in.”

He noted that India’s festival season typically boosts jewelry demand. “The market has now entered its customary post-festival soft patch, likely to stabilise as year-end buying returns, potentially aided by the recent correction,” he said. “A more structural development came from China, where authorities ended a long-standing VAT exemption for certain jewellery retailers purchasing through the Shanghai Gold Exchange and Shanghai Futures Exchange.”

Hansen said the change will raise retail costs somewhat and could dampen jewelry sales, but its macro significance is limited. “Investment gold—bars, coins, and ETFs—remains fully exempt, ensuring the key channels that have driven China’s record physical demand stay intact,” he wrote.

Hansen said Powell’s recent comments that a December rate cut is not a foregone conclusion “lifted the dollar and nudged real yields higher, further cooling enthusiasm” for gold, while the market reaction to U.S.-China tariff progress was muted.

“Investors recognise that the deeper strategic tensions remain unresolved, particularly around technology, supply chains, and industrial policy,” he said. “The announcement may have reduced tail risks but did little to change the longer-term case for owning defensive assets.”

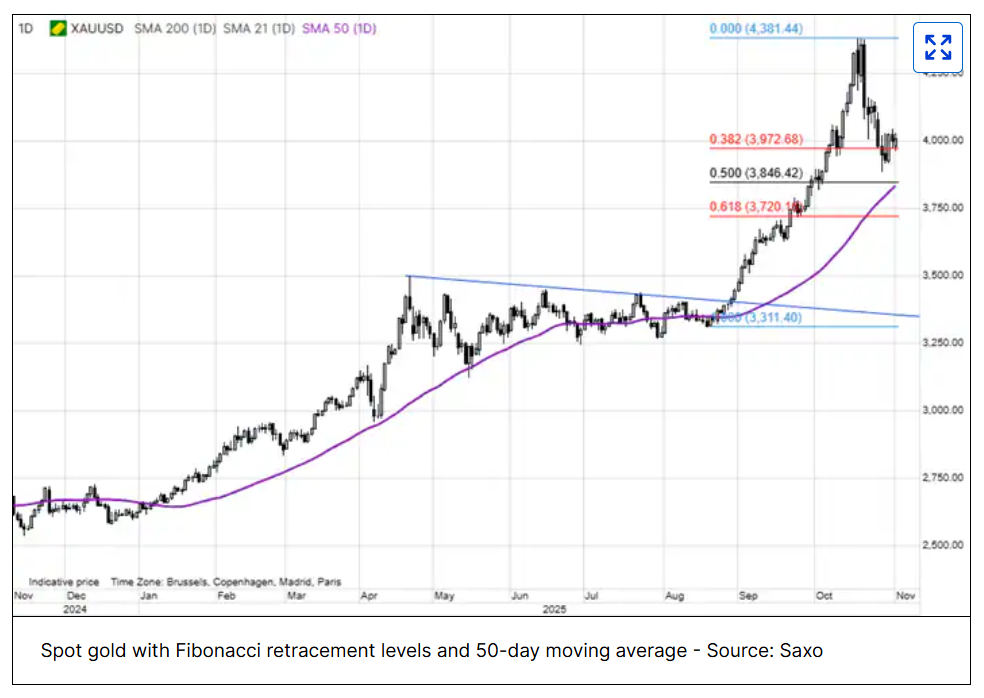

In terms of the technical picture, he said gold’s recent price correction “has been a healthy development suggesting the market is releasing pressure rather than reversing trend.”

“Support has been building near USD 3,835–3,878, an area that aligns with the 50% Fibonacci retracement of latest run up since August as well as the 50-day moving average,” Hansen said, and warned that “a deeper slide cannot be ruled out if equity market risk appetite stay buoyant and the dollar continues to firm.”

He also noted that ETF holdings rose sharply during the rally, and futures data “suggest only moderate long reduction” rather than liquidation.

“Meanwhile, central banks remain a key source of stability, with the World Gold Council reporting Q3 official purchases of 220 tonnes, lifting year-to-date buying to 634 tonnes—close to last year’s record,” he said. “This persistent official demand continues to limit downside volatility.”

Hansen said despite the yellow metal’s recent weakness, fiscal debt concerns, the threat of currency debasement, central bank demand, and the Fed’s policy trajectory mean the bullish case for gold remains intact.

Turning to gold’s short-term outlook, he said that while this year’s high may be in, the recent pullback “appears more like consolidation than capitulation.”

“The last major consolidation following the May record high near USD 3,500 lasted roughly four months before the August breakout triggered a nine-week, 27% advance,” he said. “A similar duration this time could imply another period of sideways trade before renewed strength into early 2026. Until then, elevated volatility and alternating sentiment swings may test short-term conviction on both sides of the market.”

“Once this corrective phase runs its course, the same forces that fuelled this year’s rally—debt, inflation, and diversification demand—are likely to reassert themselves, making the next meaningful leg higher a 2026 story.”