(Kitco News) - Despite significant selling pressure, the gold market has managed to hold critical long-term support above $4,000 an ounce. However, even if this support level fails, one market analyst said that current prices represent a good buying opportunity to build a long-term position.

In an interview with Kitco News, Thorsten Polliet, Honorary Professor of Economics at the University of Bayreuth and publisher of the BOOM & BUST REPORT, said that even if gold prices continue to drop, the long-term bull trend remains unbroken.

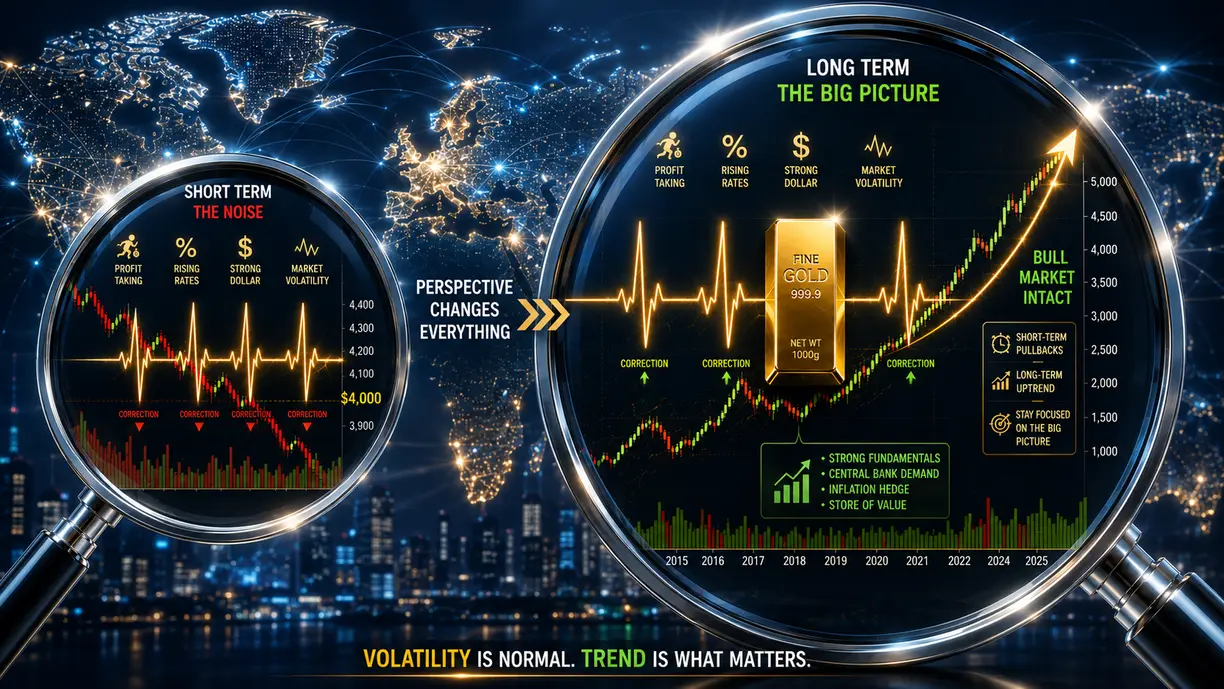

Although the recent volatility and price action have been disappointing for many gold investors, Polleit said that gold's drop from its highs should be viewed as a natural correction following an exceptionally strong rally rather than the beginning of a new bear market.

"If you use an exponential trend and another polynomial trend, then you would say $5,500 was pretty much way off any trend line," he said. "A kind of reaction from this point of view shouldn't be too surprising."

Polliet explained that even though gold could test lower levels in the near term, the fundamental outlook for the broader economy continues to provide strong support for the precious metal.

"It may drop below $4,000, but I think at $3,900 or so, roundabout there, it will stop," he said. "This is actually the underlying trend that reflects our current regime, with all its problems, with negative real interest rates, with money printing, with government debt spinning out of control."

That conviction is shaping his own investment decisions. Polleit revealed that he is considering adding to his gold holdings. Although he is still deciding between physical bullion and exchange-traded products, he said current prices would not deter him from buying.

"I wouldn't mind buying at $4,000," he said. "I wouldn't be surprised if it goes a little bit lower than that, but if you have a long-term orientation and make your decisions with a horizon of five years or longer, this is an attractive price."

For Polleit, trying to time the exact bottom may prove less important than establishing exposure to an asset that continues to benefit from powerful structural tailwinds.

"Of course, you could bet maybe it goes a little bit lower than that, but who knows?" he said. "In five years' time, I've little doubt that the gold price won't be much, much higher."

His bullish outlook rests largely on what he sees as an increasingly fragile global monetary system. Massive government debt burdens, persistent fiscal deficits, and central banks' limited ability to maintain restrictive monetary policy all support higher gold prices over the long term.

Polleit said investors continue to underestimate the implications of "fiscal dominance"—a situation where central banks become constrained by governments' financing needs. With debt levels elevated across developed economies, he believes policymakers have little room to engineer a sustained period of high real interest rates.

"Real returns will remain negative on bonds and possibly also on various stocks," he said. "That is another argument why I think gold will continue its upward trend."

Although rising bond yields have weighed on gold in recent weeks by increasing the opportunity cost of holding non-yielding assets, Polleit views that pressure as temporary. He expects markets will eventually recognize that central banks cannot maintain significantly higher rates without threatening economic growth and debt sustainability.

Beyond sovereign debt concerns, Polleit said that much of the current inflationary pressure stems from higher energy costs rather than excessive money creation. In that environment, he argued, traditional monetary policy tools are poorly suited to addressing the problem.

"This is not a normal monetary inflation process unfolding. It has been caused by a cost-push effect," he said. "You cannot fight higher energy costs by hiking rates."

According to Polleit, aggressive rate hikes in response to supply-driven inflation risk will slow economic growth and push indebted economies toward recession without meaningfully reducing underlying energy costs. That dynamic ultimately reinforces the case for gold as a long-term store of value.

Despite periodic corrections and shifting investor attention toward high-growth technology themes, Polleit believes gold remains underowned and underappreciated by many investors.

"The case for gold is even stronger now than it was a couple of years ago," he said. "Actually, I'm more convinced than ever that holding gold makes perfect sense."