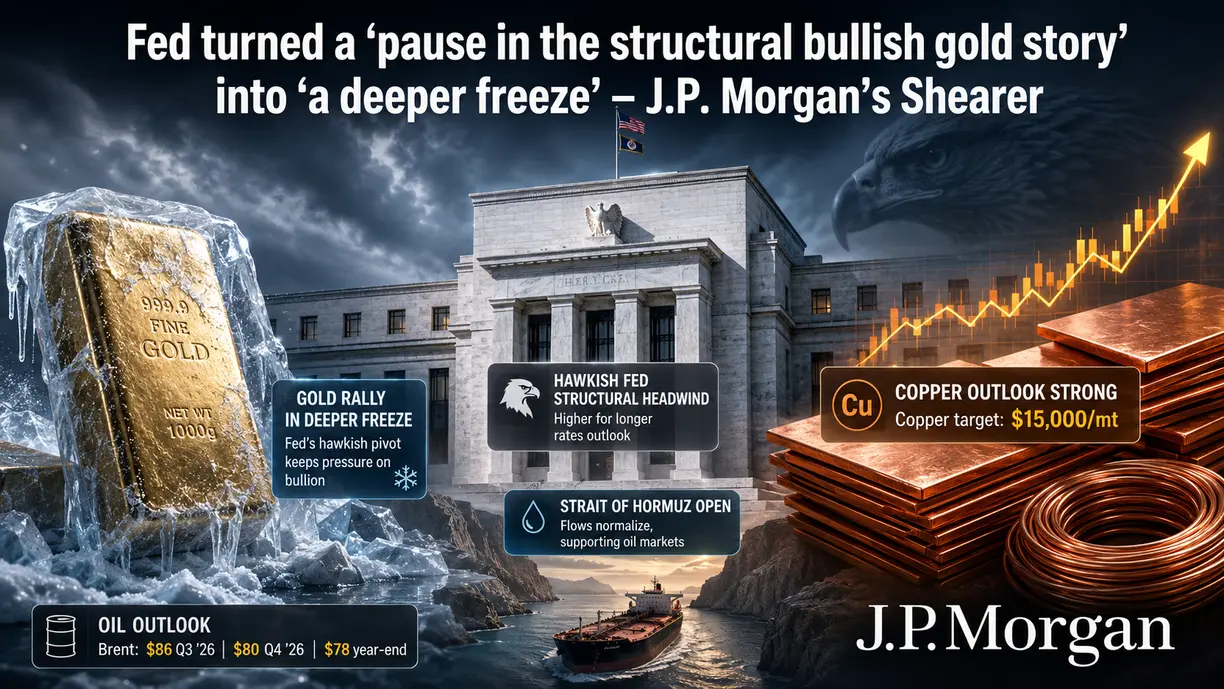

(Kitco News) – The Federal Reserve’s recent hawkish pivot has had the effect of materially prolonging the pause in gold’s structural price rally, and in the near term, the base metals may offer the most attractive investment opportunities, according to Gregory Shearer, head of Base and Precious Metals Strategy at J.P. Morgan.

In a recent interview, Shearer was first asked how he expects oil markets to react to a full reopening of the Strait of Hormuz.

“We think a reopening is in the cards,” he said. “Our current supply estimates are assuming something where there is a gradual resumption of oil flows through Hormuz. What that really looks like is something where by July, we're getting back to around 68% of pre-conflict levels, and then the rest of the year through 2026, creeping up towards about 100%. So it does jump quite a lot over the summer, and then it's a long tail of supply resumptions.”

He warned, however, that J.P. Morgan expects plenty of bumps and delays on the road back to regular supply.

“What really drives our price forecast is OECD commercial inventories,” he said. “The most recent publicly reported data from the likes of IEA are actually showing that the overall market rebalancing that we thought, essentially the close to 1.6 billion barrels of cumulative shortfall between late February and August, is still tracking. The interesting dynamic is that the releases from strategic players, governments, have been tracking what we expected, but the OECD commercial inventory decline has been materially less than we expected. And that indicates that there's likely a larger degree of demand destruction that has come into this market.”

“What this really means is that over the balance of the year, this lower-than-expected draw on OECD commercial inventories implies materially less upward pressure than what we were thinking maybe a month or two ago,” he continued. And now what we see for Brent prices themselves is something averaging around $86 per barrel in the third quarter of '26 and $80 per barrel in the fourth quarter of '26, ultimately exiting this year at a level around $78 per barrel. This over the second half of '26 is still higher than where we see the current forward curve trading, even though we think that this downward pressure carries on into '27 where our price forecast average is something around $64 per barrel, which is below the curve for next year.”

“Long story short, what we're seeing from a balance and recovery perspective actually still does imply that prices over the second half of the year are going to trade well above what is currently embedded into the oil forward curve.”

Beyond energy, Shearer said J.P. Morgan is very focused on metals for the balance of 2026.

“The first thing is gold,” he said. “The hawkish Fed from Kevin Warsh and the communications at the last FOMC has really turned this pause in the structural bullish gold story into a bit of a deeper freeze,” he said. “And within that, what we're really seeing is there's a very large lack of engagement as long as the specter of rate hikes are hanging over this market.”

“Shearer said they’ve now shifted their focus to copper. “What we see in copper is actually quite a structurally supported fundamental backdrop, seeing essentially a global industrial upturn,” he said. “We're expecting stronger momentum in China in the second half of '26 – which is a key market – all of that coming where mine supply in this copper market still remains very anemic.”

“But the biggest single factor that we're expecting over the second half of this year is essentially a tariff review for refined copper in the U.S.,” he continued. “What's happening in the copper market right now is that the U.S and China are in a tug of war for copper and what that's really leaving is ex-US market balances exceptionally tight. Our ultimate view here is that the U.S. will structure refined copper tariffs in a way that keeps imports attractive to the United States, keeping this sort of tug of war and struggle for copper ongoing, and ultimately opening the door for copper prices to push up towards around $15,000 per metric ton.”

On April 9, Tai Hui, chief market strategist, Asia Pacific at JP Morgan Asset Management said gold’s dramatic selloff during the Iran war has weakened its status as a defensive hedge, and investors should instead treat gold as an investment asset.

Hui said during a media briefing that “gold did not work as a hedge against geopolitics.”

“We’ve been arguing for quite some time that gold is not a very good hedge against anything,” Hui said. “If you look at its correlation with equities or risk assets, it’s not very consistent.”

In first 20 days from the time the attacks on Iran began, gold fell from a high of $5,415 to a low of $4,100 per ounce – a loss of 24% peak to trough – and the yellow metal has struggled to build momentum as the conflict has dragged on.

Hui said that many investors still view gold as a hedge against geopolitical events, despite the fact that its track record of performance during these types of events over the past 30 years is weak.

“We’re not even talking about 70% of [geopolitical] events get an upside,” he said. “It’s like 50/50. It’s a coin toss.”

Hui said gold has a number of things working against it, even outside of geopolitical shocks like the Iran war.

“Its volatility is as high as emerging market equities,” he pointed out. “It does not generate income. Obviously, in the last two years, if you owned gold, you didn’t care about income, but the cost of carry is something to think about.”

“If you’re owning it to enhance your return because of the fundamentals of central bank buying and the so-called debasement trade, that makes sense, but if you’re owning it in the belief that it can help you to offset market corrections, it’s not a particularly reliable tool.”

Despite these drawbacks, Hui said there are still good reasons to own gold, including long-term demand from central banks looking to diversify away from the U.S. dollar as well as investors hedging against the rapid growth of government debt and the money supply.

“As the supply of gold growth is limited, so there’s an investment case for gold, but we have to be super clear that gold is an investment asset, not a hedge asset,” he said.

“Gold, to us, is still an interesting asset to be included in asset allocation, but we just need to understand that in terms of the role it plays, it’s more of a return enhancement rather than a risk management tool.”

J.P. Morgan has consistently backed the view that the gold rally will continue and pullbacks are temporary. On Feb. 17, the firm’s senior brain trust said there’s a reasonable case to be made against gold’s continued appreciation – but that case is wrong.

“Gold has had a ferocious rally over the last five years, skyrocketing over 170%, wrote Kriti Gupta, Executive Director of J.P. Morgan Private Bank, and Justin Biemann, Global Investment Strategist. “There’s a laundry list of reasons why, but the biggest driver may be a new era of geopolitical volatility and fragmentation, incentivizing investors to buy the precious metal.”

“Now add on worries about currency debasement, growth, inflation and irresponsible fiscal finances that haven’t been fully reflected in sovereign assets,” they continued. “It’s no wonder the precious metal has been a popular asset for investors during times of stress.”