(Kitco News) – Gold prices will gain an additional 6% by the middle of 2026 as fresh demand from key groups of buyers will drive the yellow metal to new record highs, according to Goldman Sachs Research led by analyst Lina Thomas.

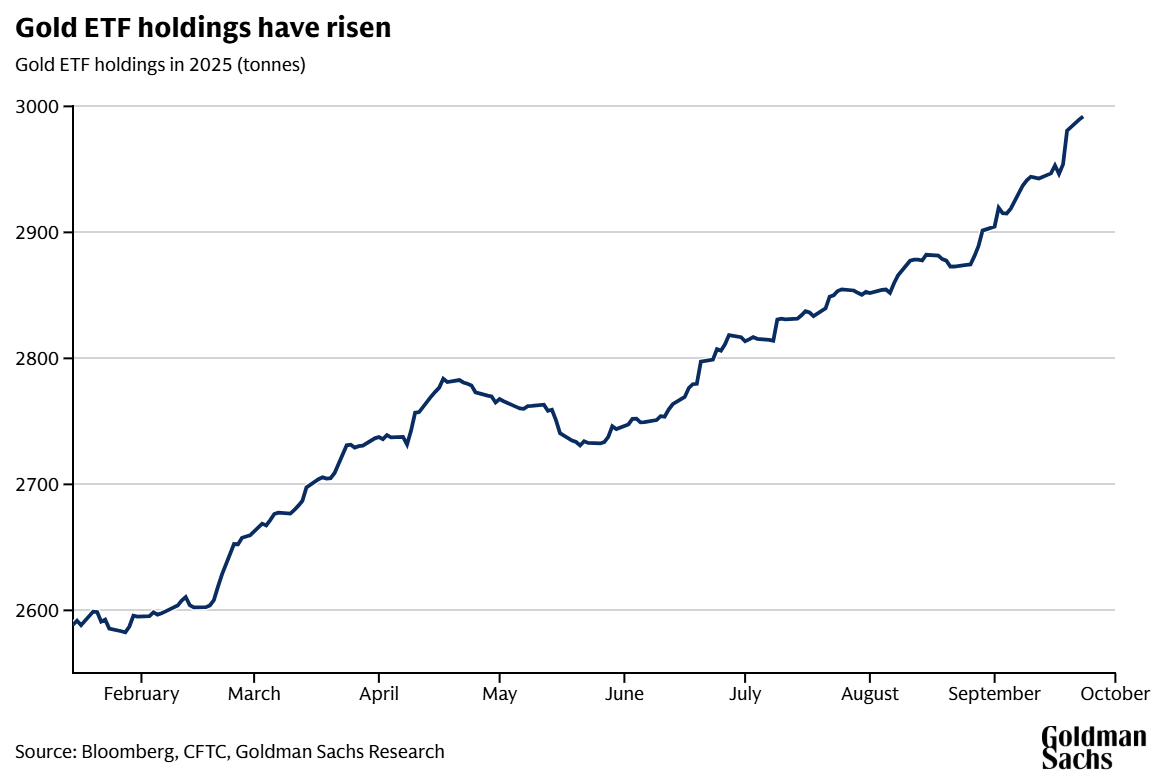

The research team predicts the gold price will rise to $4,000 per ounce by the middle of next year – up from $3,772 on September 24 – Thomas wrote in the report. The new forecast is driven by “strong structural demand from central banks and easing from the US Federal Reserve (which supports ETF demand for gold).”

The analysts said buyers of gold fall into two broad groups. “Conviction buyers tend to purchase the yellow metal consistently, regardless of the price, and based on their view on the economy or to hedge risk,” they said. “These include central banks, exchange-traded funds, and speculators. Their thesis-driven flows set the price direction.”

“As a rule of thumb, every 100 tonnes of net purchases by these conviction holders corresponds to a 1.7% rise in the gold price,” they noted.

On the other hand, opportunistic buyers – including households in emerging markets – enter the market only when they believe the price is right. “They may provide a floor under prices on the way down and resistance on the way up,” the analysts said.

According to Goldman Sachs Research’s nowcast of central bank activity, central banks purchased less gold in July than the monthly average for 2025. “Central banks have purchased 64 tonnes of gold per month this year, which is below Goldman Sachs Research’s forecast of 80 tonnes per month,” the report stated.

“This is consistent with the seasonal pattern,” Thomas said. “Central bank purchases tend to slow in the summer and re-accelerate from September. But the seasonal pattern supports our unchanged central bank outlook.”

Since Russia’s foreign-currency reserves were frozen following its invasion of Ukraine in 2022, central banks, and particularly those in emerging markets, have increased the pace of gold purchases by a factor of five. “We view this as a structural shift in reserve management behavior, and we do not expect a near-term reversal,” Thomas wrote. “Our base case assumes that the current trend in official sector accumulation continues for another three years. Our rationale is that emerging market central banks remain significantly underweight gold compared to their developed market counterparts and are gradually increasing allocations as part of a broader diversification strategy.”

Thomas said that the latest survey data from the World Gold Council supports their view, with 95% of central banks surveyed expecting global gold holdings to increase in the next 12 months, while none anticipated a decrease. Meanwhile, 43% of the surveyed central banks plan to increase their own gold holdings – the highest level since the survey began in 2018 – while none plan to sell any holdings.

“At the same time, speculative positioning in derivatives markets by large investors like hedge funds appears significantly bullish on gold,” the report noted. “The amount of net long gold bets on the futures and options exchange COMEX is in its 73rd percentile since 2014 as speculators build up their long positions betting on gold prices to rise.”

Goldman Sachs Research believes gold prices are more likely to exceed their analysts’ $4,000 forecast than to undershoot it.

However, the increase in long gold positions, a bet that prices will rise, “raises the risk of tactical pullbacks” as speculators’ net bets on gold tend to revert to the mean over time, Thomas said.

On September 26, Goldman Sachs Research advised investors to diversify through commodities like gold to protect against unexpected financial market tail risks.

“Equity-bond portfolios aren’t well protected against stagnant economic growth and elevated inflation in two situations in particular: when global policy uncertainty is elevated (e.g., markets debating the central bank’s ability to contain inflation) and when the economy is hit by a supply shock (such as a sudden interruption in energy supplies),” the report noted. “For example, gold prices jumped in the 1970s as pronounced spending by the US government and reduced central bank credibility stoked inflation.”

“Gold surged as investors sought value outside the system,” Thomas wrote in the report.

Commodities were also among the few assets that rose in inflation-adjusted terms when Russian gas to Europe was cut off in 2022. Goldman Sachs Research noted that during any 12-month period during which both stocks and bonds delivered negative real returns, either commodities or gold delivered positive performance.

Commodities can also protect portfolios against trade volatility, with Thomas pointing out that commodity supplies are becoming more concentrated, and countries are using their control over resources as geopolitical leverage.

“The growing use of commodities as leverage may reinforce the diversification benefits of commodities in portfolios,” Thomas said.